Separation Anxiety

Miners Too Far Ahead of Gold

- Mining stocks have rallied five times more than gold year-to-date

- Incremental gold demand in 2016 has been driven largely by flows into exchange traded funds

- Poor profitability among mining companies undermines current valuation

- Options market offers attractive ways to establish short exposure

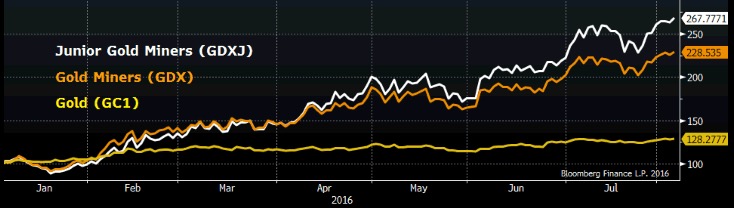

Anyone who bought gold mining stocks at the beginning of the year is a hero. The big companies like Newmont (NEM) and Barrick (ABX) are up 127% on average. The smaller takeout candidates, often called the junior miners are up even more –about 165%. No other sector even approaches triple digit returns this year. Granted, the sector peaked in 2011, so investors have had to wait five years for redemption. In addition, many of the miners still sit well below all-time highs, but this year’s windfall feels pretty good. The operative question at this point: How far will they go, or how long will this last?

Newmont Mining CEO Gary Goldberg took a stab at providing an answer during the company’s 2Q earnings call on July 20. As you might expect, he’s bullish.

“Low or even negative real interest rates are making gold an increasingly attractive investment. Concerns about slower global economic growth and weaker domestic employment have forced the Fed to be more cautious about raising interest rates. The markets now anticipate no or at most one rate hike in 2016. Inflation is also trending upward. We’re seeing more money flowing into gold on the back of these trends… global ETF gold holdings have increased by more than 17 million ounces or nearly 40%.”

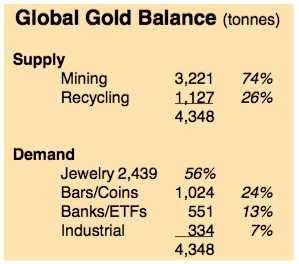

Mr. Goldberg is correct about the surge in demand from financial buyers, most notably by administrators of exchange traded funds needing to purchase gold in order to issue more units against investor inflows. You can see financial buying accounted for about 13% of demand in 2015, much of which came from central bankers, whereas this year it’s all about the ETF, 336 tonnes worth of buying in Q1. (The supply/demand balance tends to vary by about 10% from year to year, based on demand tracked by Bloomberg from the World Gold Council.) Incremental demand so far in 2016 has been enough to drive the price of gold 28% higher. It’s impressive, but there’s also a disconnect… the mining stocks are up 5 times more. I recognize they have operating leverage… but 5x?

Mr. Goldberg is correct about the surge in demand from financial buyers, most notably by administrators of exchange traded funds needing to purchase gold in order to issue more units against investor inflows. You can see financial buying accounted for about 13% of demand in 2015, much of which came from central bankers, whereas this year it’s all about the ETF, 336 tonnes worth of buying in Q1. (The supply/demand balance tends to vary by about 10% from year to year, based on demand tracked by Bloomberg from the World Gold Council.) Incremental demand so far in 2016 has been enough to drive the price of gold 28% higher. It’s impressive, but there’s also a disconnect… the mining stocks are up 5 times more. I recognize they have operating leverage… but 5x?

Conscious Uncoupling

In fairness, companies like Newmont Mining have been particularly adept and lowering costs and paying down debt during the four year gold implosion which haunted them from 2011 to 2015. They’ve shuttered marginal mines and generally brought all-in sustaining costs (AISC) down to $700-800/oz from well over $1,000/oz. In the case of Barrick Gold, net debt has fallen from $10.4B in 2014 to about $7.5B currently. Overall, mining companies have done a good job retooling their businesses to prepare for leaner times, realizing like so many others $2,000 gold wasn’t the slam-dunk markets had assumed.

It’s a very different scene from 2010, when I interviewed then-Newmont CEO Richard O’Brien at the BMO Metals & Mining Conference for Bloomberg Television. He had just wound down the last of Newmont’s hedges (impeccably timed) and proudly announced he did so because investors told him they wanted exposure to gold, not financial wizardry. They certainly got it… albeit in a different way.

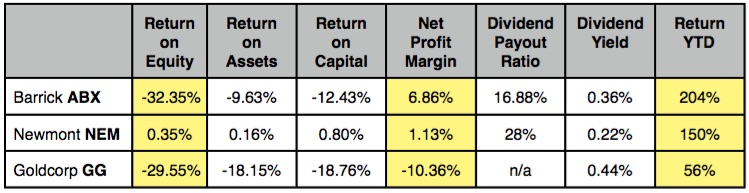

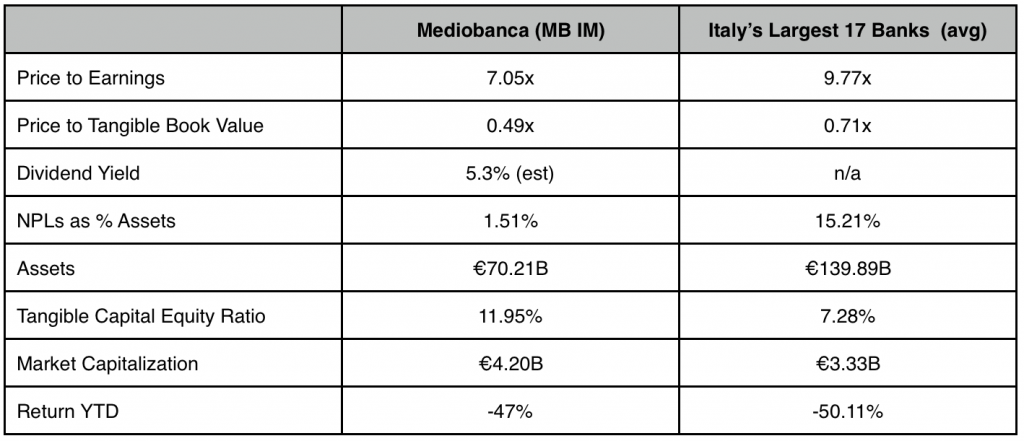

Here’s the thing about gold investors: When they buy, they think gold is going to make them rich. It’s not about double-digit earnings growth or cheap NAV, it’s about runaway inflation or the end of fiat currency and only gold will protect them. $2,000 gold? More like $10,000 gold. Take a look at the metrics for the three largest mining companies in the ever popular VanEck Gold Miners ETF (GDX), whose daily average volume of 73M shares makes it one of the most active equity securities in the world.

You Want to Own These?

Q1 Profit Metrics

The profitability metrics on these companies are AWFUL, and by the way there’s no dividend to speak of because there are virtually no earnings. Obviously investors see something else… I love Goooooooooold.

Okay, I admit an average price to book ratio of 2.09 for the miners in the GDX and 1.96 for the smaller companies in the GDXJ is not unreasonable. It’s neither rich relative to the S&P 500 Index nor to the historical range for the sector. In addition, I fully recognize the appeal of gold against the backdrop of rising sovereign debt due to global money printing by central banks. I will also grant that all this money printing may one day stoke inflation, against which gold should provide a hedge. Fine.

But let me say this: I do not want to own marginally profitable mining companies already up 150-200% YTD on the “hope” gold rallies further. In fact, I want to short them, and the analyst community would appear to agree. Many of the stocks within the GDX and GDXJ are trading at/near consensus targets. They’ve had their run and it’s time to sell. Here’s how we do this:

1. Buy puts on the GDXJ funded by selling calls. I like Sep 50 puts vs Sep 53 calls at even money (both $2.80) with the index at $51.00. This combo give us a little cushion and costs nothing initially.

2. Buy long-dated GDX Nov 29 puts for $1.90 and forget about them. The index is at $31.25 so the breakeven is -12.58% and if the miners break, this option will accelerate quickly (33 delta currently).

3. Short a little Couer Mining for fun at $15.75… it’s up 535% YTD.

Subscribe at https://bullseyebrief.com

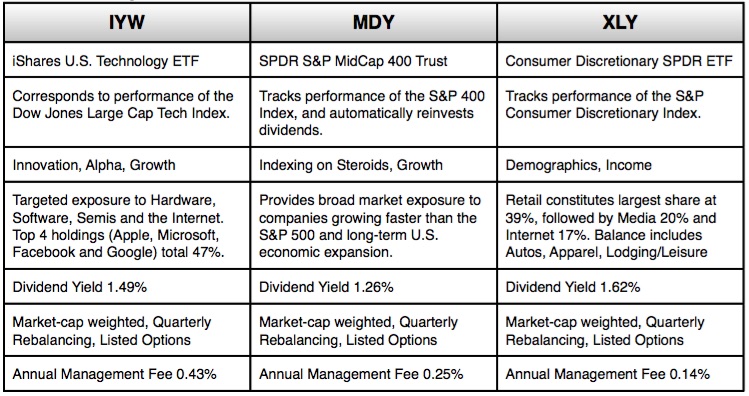

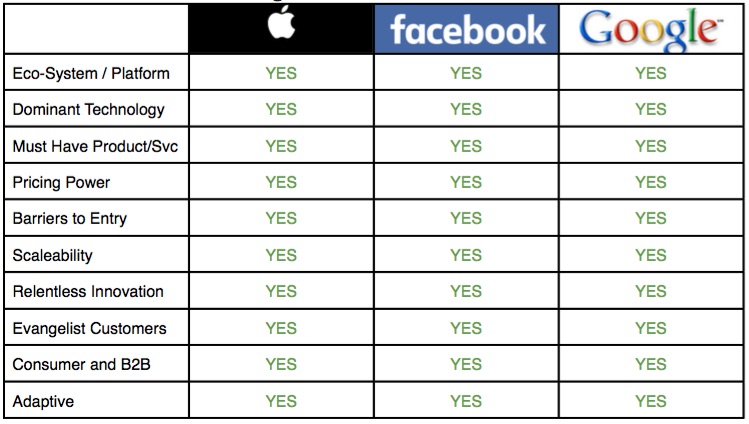

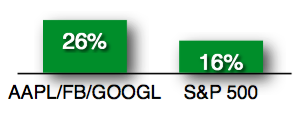

Bloomberg lists a total of 35 technology ETFs. I selected IYW because it offers the highest exposure to Apple/Facebook/Google (35% of assets). These three companies reinvest an average of 26% of sales back into R&D plus CapEx, compared to 16% for the S&P 500 Index. These companies are committing $84B annually in pursuit of new solutions. They clearly BELIEVE in their ability to innovate, which I find very attractive.

Bloomberg lists a total of 35 technology ETFs. I selected IYW because it offers the highest exposure to Apple/Facebook/Google (35% of assets). These three companies reinvest an average of 26% of sales back into R&D plus CapEx, compared to 16% for the S&P 500 Index. These companies are committing $84B annually in pursuit of new solutions. They clearly BELIEVE in their ability to innovate, which I find very attractive.

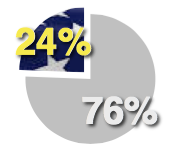

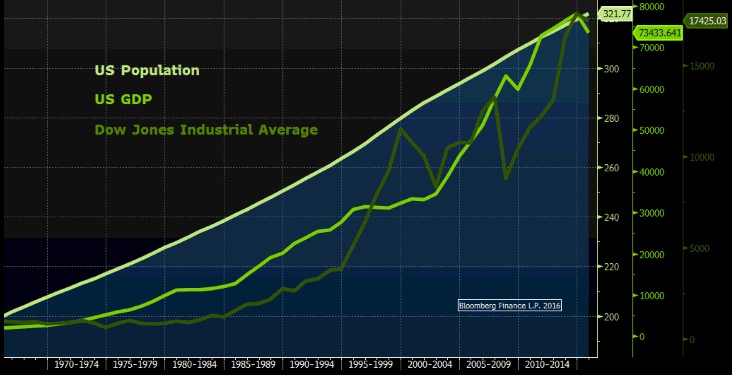

entrepreneurs (Mr. Trump, are you listening?) free of regulation and onerous taxes (ahem, Ms. Clinton?), the U.S. produces 24.4% of world GDP with just 4.5% of the world’s population. This is an incredible testament to U.S. productivity, which speaks loud and clear of the American Dream. While oil-rich countries with smaller populations like Kuwait and Norway can claim higher per capita figures, the average American household earns $53,657 per year. More importantly for our purpose as investors, Americans spend approximately two-thirds of this income consuming products and services (the balance goes to taxes and savings). –> There’s a reason why former Fed Chair Greenspan called Wal-Mart each month to track consumer expenditures…

entrepreneurs (Mr. Trump, are you listening?) free of regulation and onerous taxes (ahem, Ms. Clinton?), the U.S. produces 24.4% of world GDP with just 4.5% of the world’s population. This is an incredible testament to U.S. productivity, which speaks loud and clear of the American Dream. While oil-rich countries with smaller populations like Kuwait and Norway can claim higher per capita figures, the average American household earns $53,657 per year. More importantly for our purpose as investors, Americans spend approximately two-thirds of this income consuming products and services (the balance goes to taxes and savings). –> There’s a reason why former Fed Chair Greenspan called Wal-Mart each month to track consumer expenditures…

NAV write-downs of 20-25% and immediate negotiations to begin liquidating assets in order to satisfy redemptions. Analysts piled-on and share prices plunged. In less than a week, several stocks got cut in half. Then something funny happened: Institutional buyers showed up. As retail holders clamored for cash, pros opened their checkbooks.

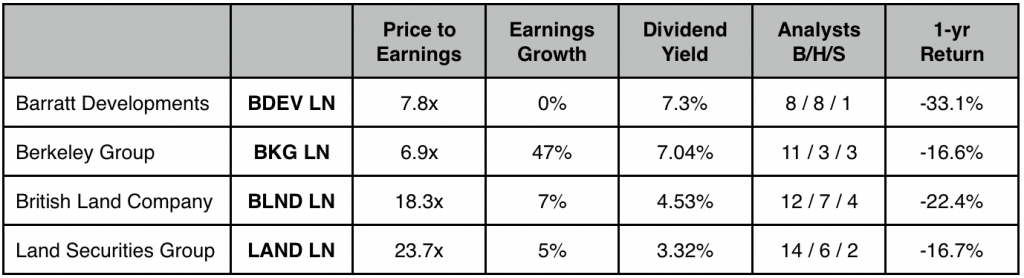

NAV write-downs of 20-25% and immediate negotiations to begin liquidating assets in order to satisfy redemptions. Analysts piled-on and share prices plunged. In less than a week, several stocks got cut in half. Then something funny happened: Institutional buyers showed up. As retail holders clamored for cash, pros opened their checkbooks. to Debenhams for £400M, which equates to a cap rate of just 2.75%. That’s more expensive than the record 3-5% cap rates being paid in Manhattan. It’s also a significant premium to the 7% rate paid for the same property in 2008.

to Debenhams for £400M, which equates to a cap rate of just 2.75%. That’s more expensive than the record 3-5% cap rates being paid in Manhattan. It’s also a significant premium to the 7% rate paid for the same property in 2008.

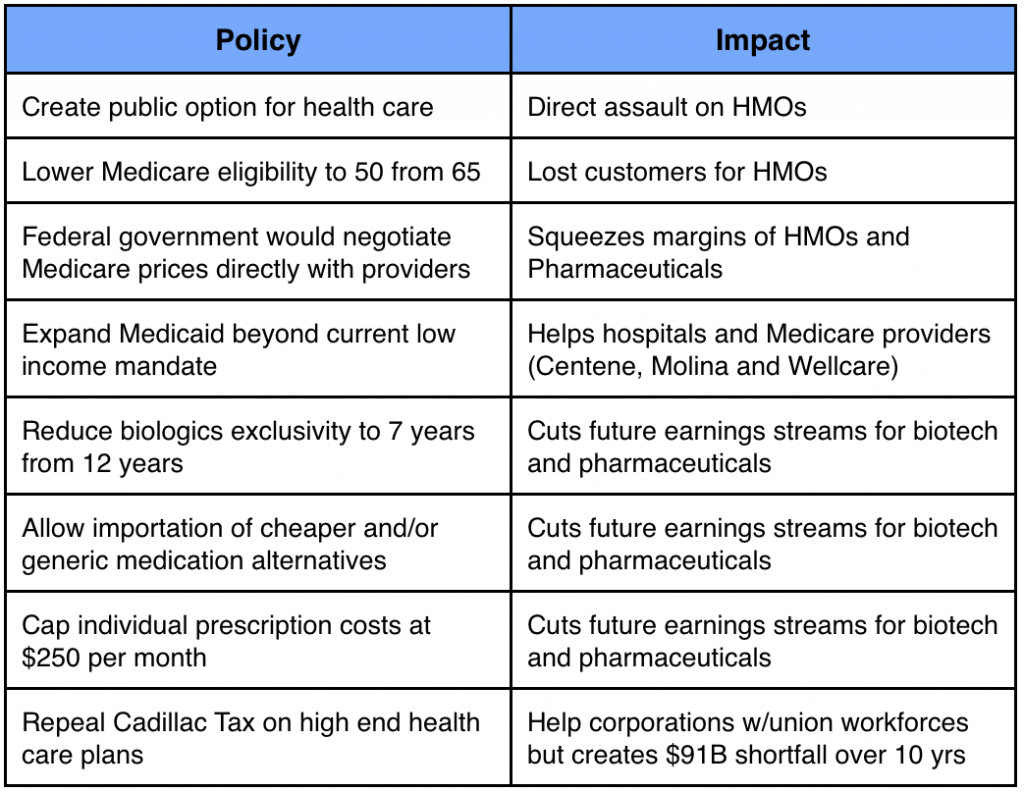

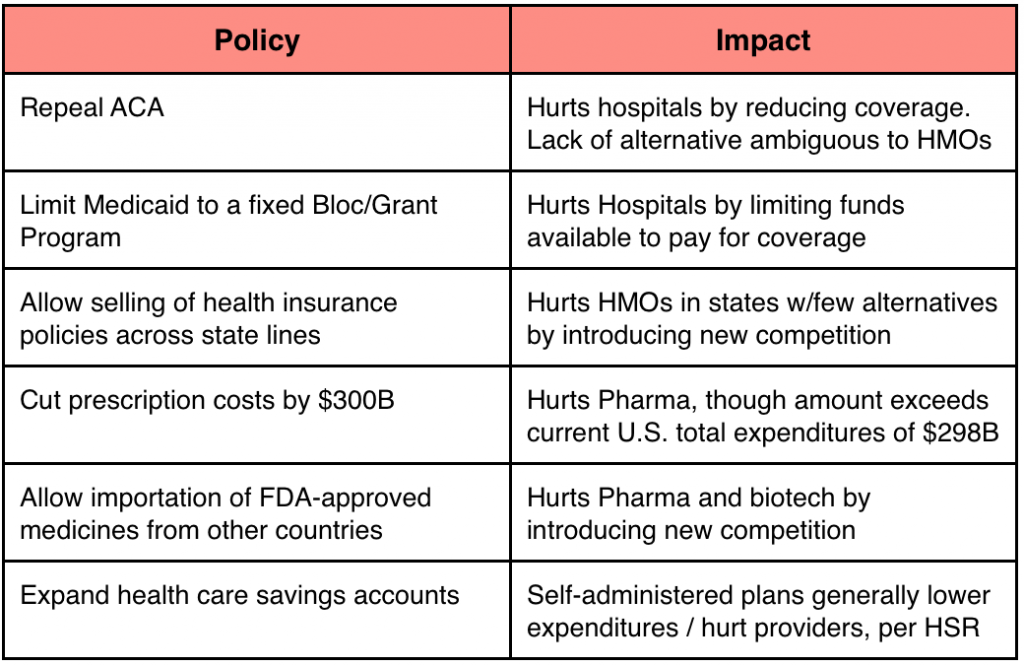

For starters, history implies a far more positive prognosis for health care investors post election. Credit Suisse analyzed stock performance of health care companies during election years since 1984 and found they tend to languish ahead of elections, then rebound once the veil of uncertainty is lifted. Writes analyst Scott Fidel, “P/E multiples for MCOs and EV/EBITDA multiples for hospitals tend to trade at discounts to 5-year averages leading into election day… and political uncertainty is intensified this year.” This intensity is due both to the closeness of the race and healthcare’s 17.8% share of U.S. GDP. It has become the ultimate political lightning rod.

For starters, history implies a far more positive prognosis for health care investors post election. Credit Suisse analyzed stock performance of health care companies during election years since 1984 and found they tend to languish ahead of elections, then rebound once the veil of uncertainty is lifted. Writes analyst Scott Fidel, “P/E multiples for MCOs and EV/EBITDA multiples for hospitals tend to trade at discounts to 5-year averages leading into election day… and political uncertainty is intensified this year.” This intensity is due both to the closeness of the race and healthcare’s 17.8% share of U.S. GDP. It has become the ultimate political lightning rod. “The present system is unsustainable. The only question is whether we will master the change or it will master us. I am offering a specificic agenda which will get us to universal health care coverage. That’s what I will do as President.”

“The present system is unsustainable. The only question is whether we will master the change or it will master us. I am offering a specificic agenda which will get us to universal health care coverage. That’s what I will do as President.”

“Since March of 2010, the American people have had to suffer under the incredible economic burden of the Affordable Care Act–Obamacare. We’re going to repeal and replace this horror, and it is a horror.”

“Since March of 2010, the American people have had to suffer under the incredible economic burden of the Affordable Care Act–Obamacare. We’re going to repeal and replace this horror, and it is a horror.”

The so-called “Matrix stocks” have been on fire since my late February write-up, rising 29% or about three and a half times more the S&P 500 Index. These are the companies focused on helping businesses process and interpret reams of data generated by e-commerce, social media and the Internet of Things (IoT). Apigee (APIC) is a particular standout, having doubled from $6 to $12. The company derives its name from Application Programming Interfaces or API, hence Apigee. CEO Chet Kapoor explained to me in surprisingly plain English how APIs funnel facts/figures from company databases into simple spreadsheets so developers can create new apps. Data mining is evolving rapidly, moving quickly from Business Intelligence to Artificial Intelligence… i.e. from data interpretation to data prediction. This key theme will spawn more ideas in upcoming issues of Bullseye.

The so-called “Matrix stocks” have been on fire since my late February write-up, rising 29% or about three and a half times more the S&P 500 Index. These are the companies focused on helping businesses process and interpret reams of data generated by e-commerce, social media and the Internet of Things (IoT). Apigee (APIC) is a particular standout, having doubled from $6 to $12. The company derives its name from Application Programming Interfaces or API, hence Apigee. CEO Chet Kapoor explained to me in surprisingly plain English how APIs funnel facts/figures from company databases into simple spreadsheets so developers can create new apps. Data mining is evolving rapidly, moving quickly from Business Intelligence to Artificial Intelligence… i.e. from data interpretation to data prediction. This key theme will spawn more ideas in upcoming issues of Bullseye. StealthGas (GASS) is my second best performer to date up 12.84% since late March. It is also MY SINGLE WORST MANAGED POSITION. The stock rallied from $3.35 to over $5 in two months and I did nothing to protect the gains. I could have written all of you to say “put a little something in your pocket here” or at least put a floating stop on the position. Instead I have watched if slip back into the 3s. Admittedly, the fundamental story is still intact: StealthGas trades at a fraction of Net Asset Value (NAV), controls 20% of the global market for smaller Liquified Petroleum Gas tankers (LPGs), and is making money even at historic low day rates. As a result, it is still a buy. But instead of having fresh capital from $5 sales to redeploy into $3 purchases, I’m already committed. Bottom line: I grade the thesis A-plus, my risk management C-minus.

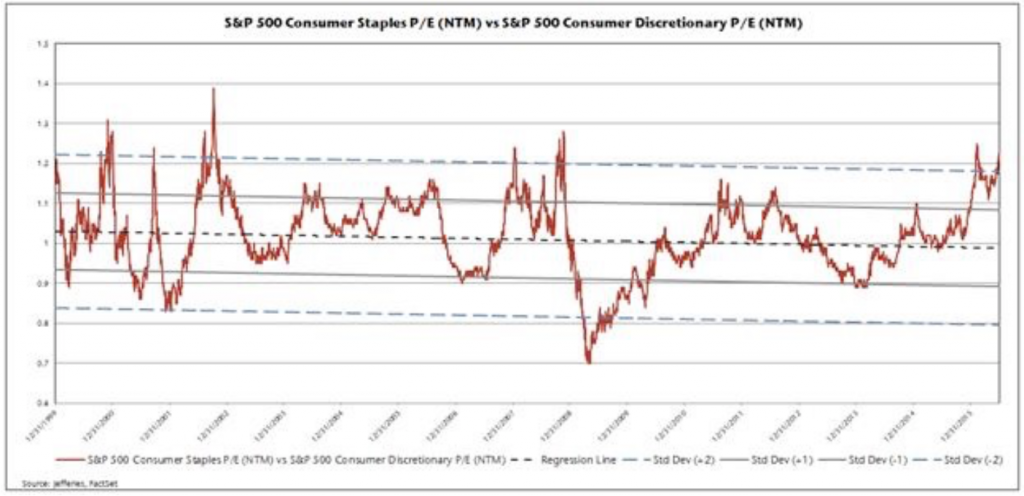

StealthGas (GASS) is my second best performer to date up 12.84% since late March. It is also MY SINGLE WORST MANAGED POSITION. The stock rallied from $3.35 to over $5 in two months and I did nothing to protect the gains. I could have written all of you to say “put a little something in your pocket here” or at least put a floating stop on the position. Instead I have watched if slip back into the 3s. Admittedly, the fundamental story is still intact: StealthGas trades at a fraction of Net Asset Value (NAV), controls 20% of the global market for smaller Liquified Petroleum Gas tankers (LPGs), and is making money even at historic low day rates. As a result, it is still a buy. But instead of having fresh capital from $5 sales to redeploy into $3 purchases, I’m already committed. Bottom line: I grade the thesis A-plus, my risk management C-minus. Consumer Staples continue to defy gravity. Many trade at earnings multiples of 30 times (nearly double the S&P 500 Index), in spite of low single digit earnings growth and dividend yields well under 2%. Predictability and yield were the entire thesis for long investors seeking safety and income. Now valuation has effectively rendered their appeal null and void… just don’t tell Mondelez. On June 30 it launched a bid for Hersey (HSY), which is one of the shorts on my list. Several have since popped 5-6%. Hershey has said, no thanks, as it did to both Nestle and Wm. Wrigley Jr. Co. back in 2002. Takeover bids aside, staples are relatively low volatility stocks historically, which partly explains why they’ve attracted safe haven investors since 2008.I would add to short positions, or at least by long-dated puts which represent a low cost way to position for an eventual return to earth.

Consumer Staples continue to defy gravity. Many trade at earnings multiples of 30 times (nearly double the S&P 500 Index), in spite of low single digit earnings growth and dividend yields well under 2%. Predictability and yield were the entire thesis for long investors seeking safety and income. Now valuation has effectively rendered their appeal null and void… just don’t tell Mondelez. On June 30 it launched a bid for Hersey (HSY), which is one of the shorts on my list. Several have since popped 5-6%. Hershey has said, no thanks, as it did to both Nestle and Wm. Wrigley Jr. Co. back in 2002. Takeover bids aside, staples are relatively low volatility stocks historically, which partly explains why they’ve attracted safe haven investors since 2008.I would add to short positions, or at least by long-dated puts which represent a low cost way to position for an eventual return to earth.

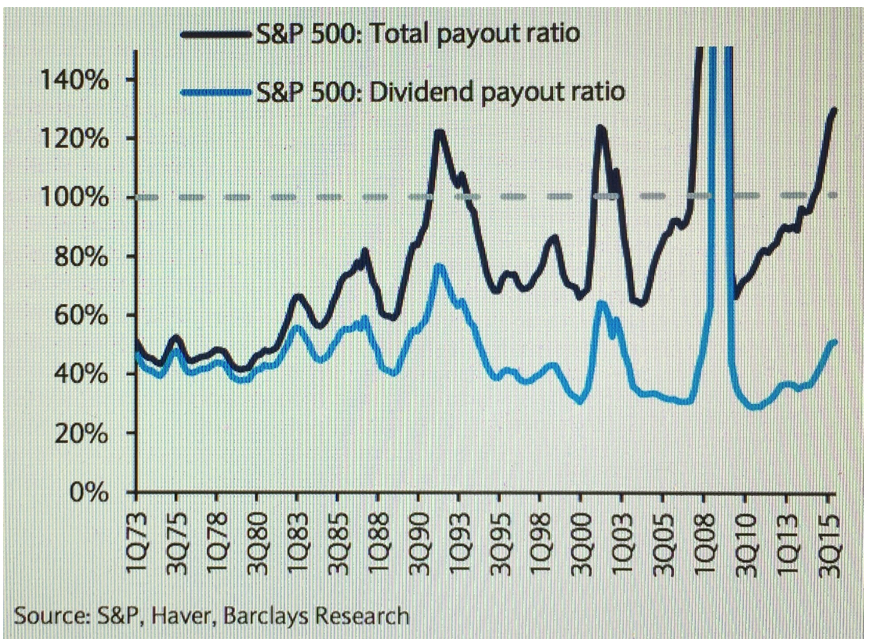

Barclays Head of U.S. Equity Strategy Jonathan Glionna offers some particularly sobering data for the fiscally minded among us. In his mid-year note to clients, he concludes U.S. corporations are paying money to shareholders which they simply do not have. Specifically, he examined payout rations by sector, defined as the total amount companies pay in dividends and spend on buybacks expressed as a percentage of net income. Think of it as the amount a corporation effectively gives back to share holders. One is a cash payment, the other raises earnings per share by lowering share count. Both are generally deemed rewarding…generally. The problem in this case is a combined (total) payout ratio of 128%, meaning corporations are paying out more than they earn.

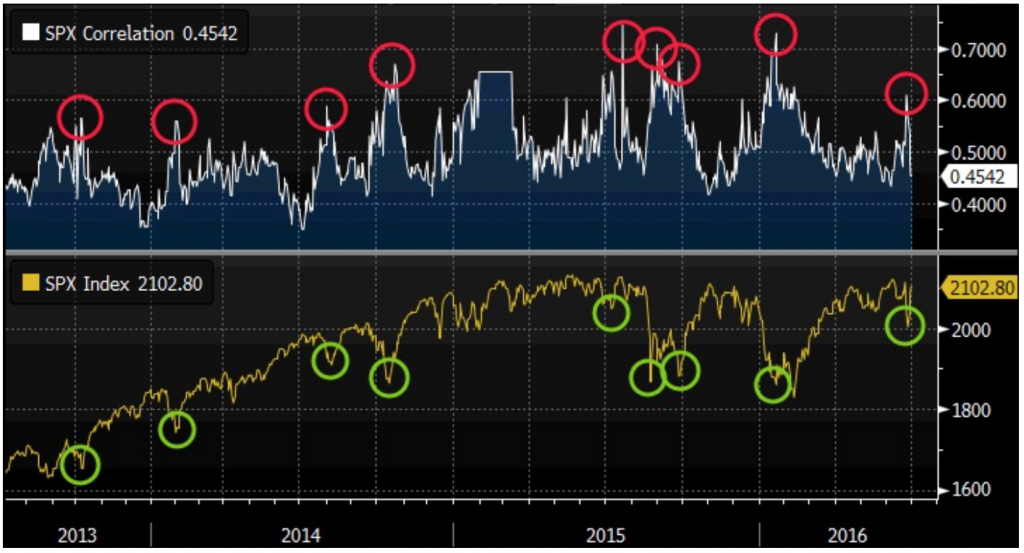

Barclays Head of U.S. Equity Strategy Jonathan Glionna offers some particularly sobering data for the fiscally minded among us. In his mid-year note to clients, he concludes U.S. corporations are paying money to shareholders which they simply do not have. Specifically, he examined payout rations by sector, defined as the total amount companies pay in dividends and spend on buybacks expressed as a percentage of net income. Think of it as the amount a corporation effectively gives back to share holders. One is a cash payment, the other raises earnings per share by lowering share count. Both are generally deemed rewarding…generally. The problem in this case is a combined (total) payout ratio of 128%, meaning corporations are paying out more than they earn. Gold has been on a tear this year, and it’s not due to industrial demand or the fabled Indian Wedding season, which can create short-term seasonal spikes of 15%. Futures have risen from under $1,100/oz last December to $1,350 recently. I admit I have missed this move completely, but I have certainly not missed the staggering outperformance of gold relative to copper. Whereas demand for gold as a store of value has soared, its industrial cousin copper has languished, and the ratio between the two now stands at 6.11 (meaning one ounce of gold costs 6.11 times more than 100 pounds of copper). This nearly equates to the peak during 2009. The disparity within metals reveals a larger disparity within markets: Can the Dow Industrials maintain a near record high with industrial metal demand at a near record low? One position implies hope, the other implies fear and I do not believe two such critical assets classes can sustain polar opposite viewpoints indefinitely. The rubber bands are getting stretched, farther and farther.

Gold has been on a tear this year, and it’s not due to industrial demand or the fabled Indian Wedding season, which can create short-term seasonal spikes of 15%. Futures have risen from under $1,100/oz last December to $1,350 recently. I admit I have missed this move completely, but I have certainly not missed the staggering outperformance of gold relative to copper. Whereas demand for gold as a store of value has soared, its industrial cousin copper has languished, and the ratio between the two now stands at 6.11 (meaning one ounce of gold costs 6.11 times more than 100 pounds of copper). This nearly equates to the peak during 2009. The disparity within metals reveals a larger disparity within markets: Can the Dow Industrials maintain a near record high with industrial metal demand at a near record low? One position implies hope, the other implies fear and I do not believe two such critical assets classes can sustain polar opposite viewpoints indefinitely. The rubber bands are getting stretched, farther and farther.

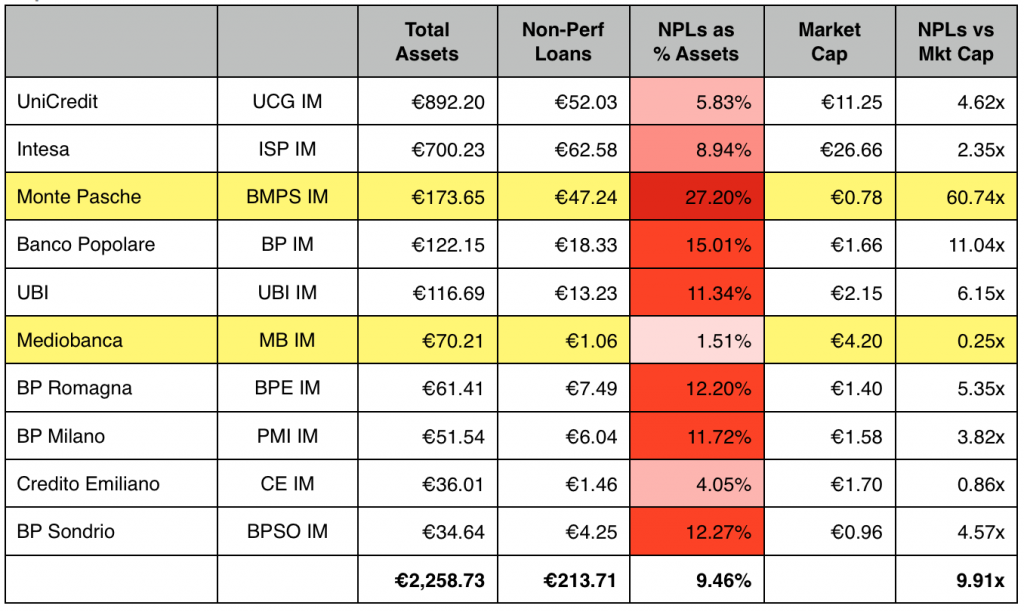

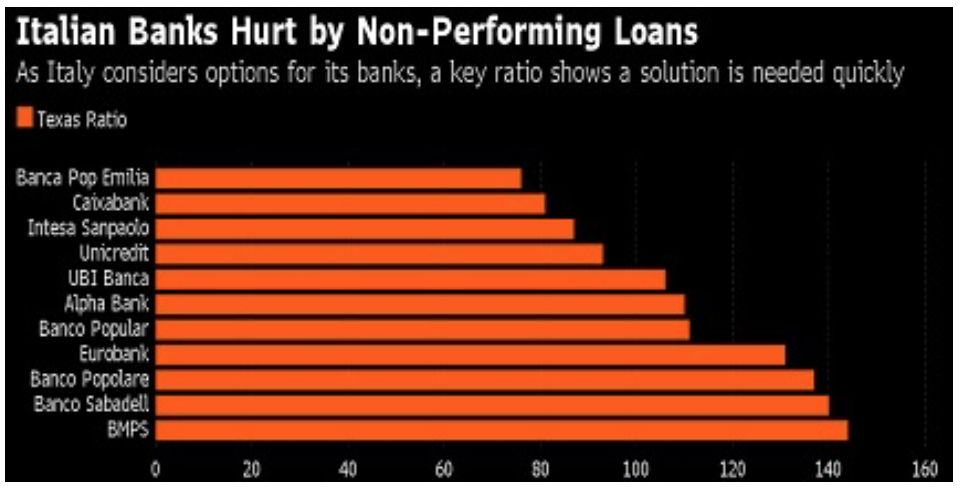

Italy’s banks desperately need recapitalization. In addition to NPLs as a percentage of total assets, regulators also consider something called the Texas Ratio, which is defined as NPLs divided by tangible common equity plus loan loss reserves. It measures the extent to which a bank’s capital cushion has been overwhelmed. Any number above 100 is considered highly problematic, and this Bloomberg chart clearly illustrates Italian banks have exceeded their cushion in stunning fashion. Poster child BMPS is on the bottom, appropriately.

Italy’s banks desperately need recapitalization. In addition to NPLs as a percentage of total assets, regulators also consider something called the Texas Ratio, which is defined as NPLs divided by tangible common equity plus loan loss reserves. It measures the extent to which a bank’s capital cushion has been overwhelmed. Any number above 100 is considered highly problematic, and this Bloomberg chart clearly illustrates Italian banks have exceeded their cushion in stunning fashion. Poster child BMPS is on the bottom, appropriately. In other words, some of the bond holders will get less than others, but no one is going to get totally shafted. Remember, even Greek and Cypriot banks got bailed out. The European Central Bank, the European Commission, the International Monetary Fund, the EU Stabilization Fund, Germany’s Bundesbank and every other governmental agency is in on the game. They don’t call him Super Mario for nothing.

In other words, some of the bond holders will get less than others, but no one is going to get totally shafted. Remember, even Greek and Cypriot banks got bailed out. The European Central Bank, the European Commission, the International Monetary Fund, the EU Stabilization Fund, Germany’s Bundesbank and every other governmental agency is in on the game. They don’t call him Super Mario for nothing.

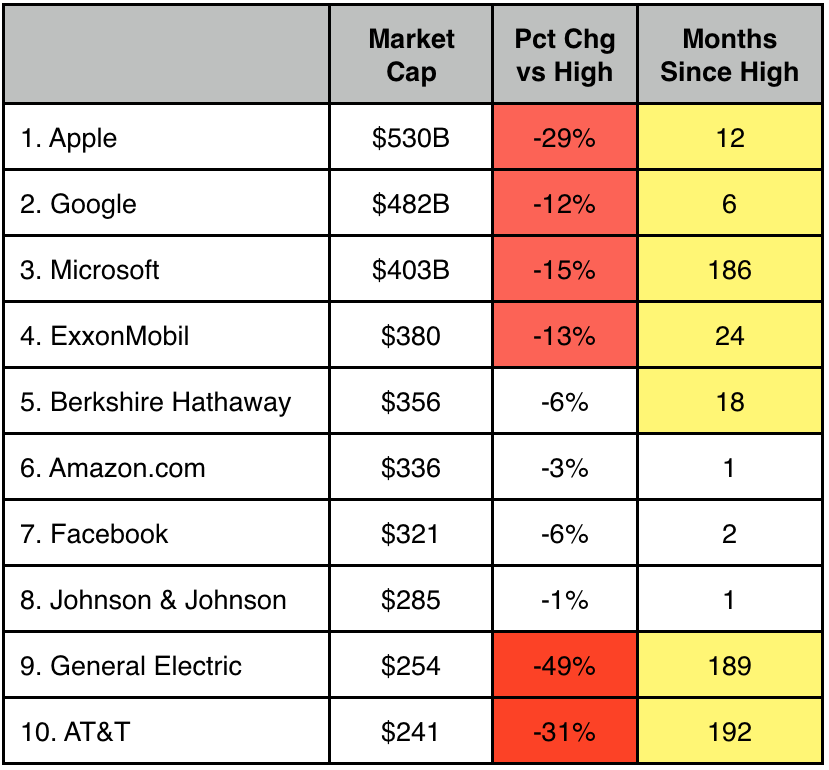

Amazon and Facebook have managed to buck the trend, but leadership among the “leaders” has been hard to come by. I show the ten biggest S&P 500 stocks by market cap to illustrate the point. Again, this group is down an average of 16.5% from individual all-time highs, and those highs were recorded an average of 64 months ago. Patience is a virtue. Or torture. Look at Microsoft. It peaked 186 months ago, but still sits 15% below the peak. It may be the third largest company in the U.S. but it hasn’t exactly produced

Amazon and Facebook have managed to buck the trend, but leadership among the “leaders” has been hard to come by. I show the ten biggest S&P 500 stocks by market cap to illustrate the point. Again, this group is down an average of 16.5% from individual all-time highs, and those highs were recorded an average of 64 months ago. Patience is a virtue. Or torture. Look at Microsoft. It peaked 186 months ago, but still sits 15% below the peak. It may be the third largest company in the U.S. but it hasn’t exactly produced