Inferno Italiano

One Firbird in the Flames

- Non-performing loans at Italy’s 10 largest banks swamp equity capitalization 9 to 1

- Italian bailout fund Atlante needs its own bailout… for a third time

- Multiple European regulators now shuffling the deck chairs but bonds still afloat

- Deep value equity buyers risk deep disappointment, with one critical exception

“The Italian government is in a dialogue with the European Commission on how to apply the stabilization framework to these specific circumstances…” says Klaus Regling, CEO of the EU Stabilization Fund. “I am sure they will find a way.” Yes of course they will. European Central Bank President Mario Draghi famously assured us “whatever it takes” in 2012, having since saved the far less systemically relevant Greek and even Cypriot banks. Countries don’t let entire banking sectors go out of business, but if you’re looking to buy, I’d advise Allegro Non Troppo… not too fast.

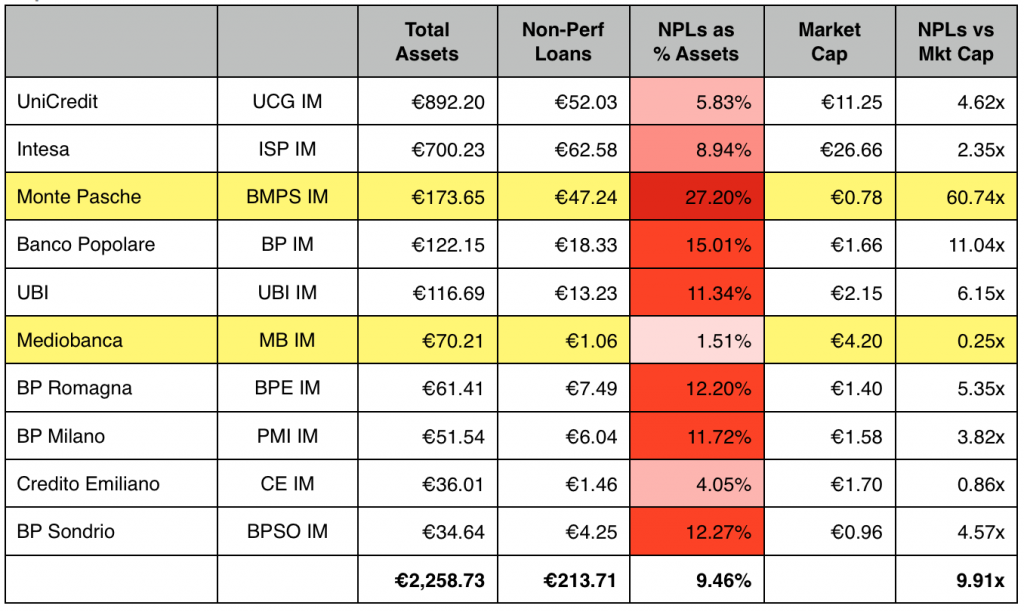

Italy’s banking sector has been teetering on the brink of insolvency for many months, though not until #Brexit highlighted the unwillingness of healthier countries to keep footing the bill did the Italian banking stocks truly implode. The poster child for ill-health and under-capitalization is Italy’s third largest bank by assets, Banco Monte dei Paschi di Sienna (BMPS IM). Over a quarter of its assets are classified as nonperforming, and the stock now trades for pennies. NPLs have completely overwhelmed Italian bank balance sheets, and on average, NPLs exceed market cap by 9.91 times. (Note I’ve also highlighted fifth largest, Mediobanca. Its 1.51% ratio of non-performing loans to assets is consistent with the U.S. average of 1.59%. We’ll get to tour “Firebird” in a moment.) First, the pain.

Italy’s Bleeding Banks

Top 10 Ranked by Assets (billions)

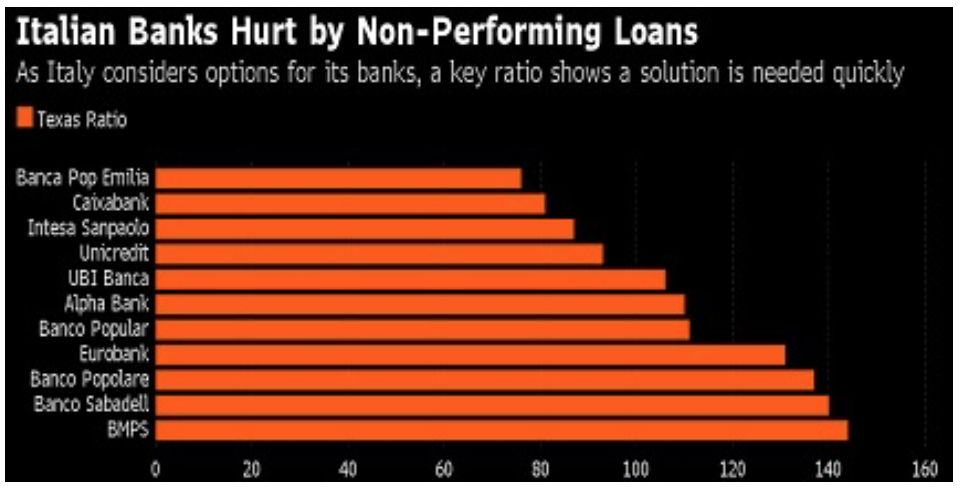

Italy’s banks desperately need recapitalization. In addition to NPLs as a percentage of total assets, regulators also consider something called the Texas Ratio, which is defined as NPLs divided by tangible common equity plus loan loss reserves. It measures the extent to which a bank’s capital cushion has been overwhelmed. Any number above 100 is considered highly problematic, and this Bloomberg chart clearly illustrates Italian banks have exceeded their cushion in stunning fashion. Poster child BMPS is on the bottom, appropriately.

Italy’s banks desperately need recapitalization. In addition to NPLs as a percentage of total assets, regulators also consider something called the Texas Ratio, which is defined as NPLs divided by tangible common equity plus loan loss reserves. It measures the extent to which a bank’s capital cushion has been overwhelmed. Any number above 100 is considered highly problematic, and this Bloomberg chart clearly illustrates Italian banks have exceeded their cushion in stunning fashion. Poster child BMPS is on the bottom, appropriately.

While Q1 filings for the 10 largest banks indicate NPLs of 213 Euros, Italian regulators peg total sector NPLs at 400 Euros. The bad news here (beyond the obvious acceleration over several months and likely underestimation by “audited” figures from March) is that the country’s privately administered bailout fund doesn’t have enough capital to cover the bailout. It’s called the “Atlante” fund, which is Italian for Atlas… a curious choice given the Atlas Mountains and implicit “mountain of debt” metaphor. It’s capital of roughly 4.5 billion Euros equates to 1/100 of the theoretical total of NPLs on Italian bank balance sheets. As a result, the European Commission has authorized the Italian government to provide guarantees on 150 billion Euros of NPLs, though that’s still less than half the total of 400 billion. Oh, and Italy’s Debt to GDP is already 133%. Madonna!

Scuzi… Now What?

Curiously, Italian bank equities tell one story, but the bonds tell another. Consider poster child BMPS IM. While the stock has fallen to about ¢0.30 Euros, reflecting tangible common equity worth less than NPLs (ie insolvent), the bank’s 47 billion Euros of debt trade significantly higher (Bloomberg/BoAML quotes)

• 22 secured bond issues due July 2016 through November 2025 currently yield 0.52% to 1.31%

• 132 unsecured bond issues due July 2016 through May 2021 currently yield 4-7%

Only do subordinated bonds (8 issues 13.89% avg) and junior subordinated bonds (6 issues 34.26% avg) reflect the stress of the situation. Note, many of these bonds trade infrequently, marks are indicative only.

In other words, some of the bond holders will get less than others, but no one is going to get totally shafted. Remember, even Greek and Cypriot banks got bailed out. The European Central Bank, the European Commission, the International Monetary Fund, the EU Stabilization Fund, Germany’s Bundesbank and every other governmental agency is in on the game. They don’t call him Super Mario for nothing.

In other words, some of the bond holders will get less than others, but no one is going to get totally shafted. Remember, even Greek and Cypriot banks got bailed out. The European Central Bank, the European Commission, the International Monetary Fund, the EU Stabilization Fund, Germany’s Bundesbank and every other governmental agency is in on the game. They don’t call him Super Mario for nothing.

As for Wall Street’s take, Morgan Stanley writes “If done successfully, this could be a major catalyst for the banking sector in Europe, not just Italy. Citigroup and Mediobanca have run their own stress test scenarios, and while not quite as sanguine, the point is their analysts are trying to quantify

downside because their customers and portfolio managers sense another ECB bear hug. People want in.

Good Business, Bad Zip Code

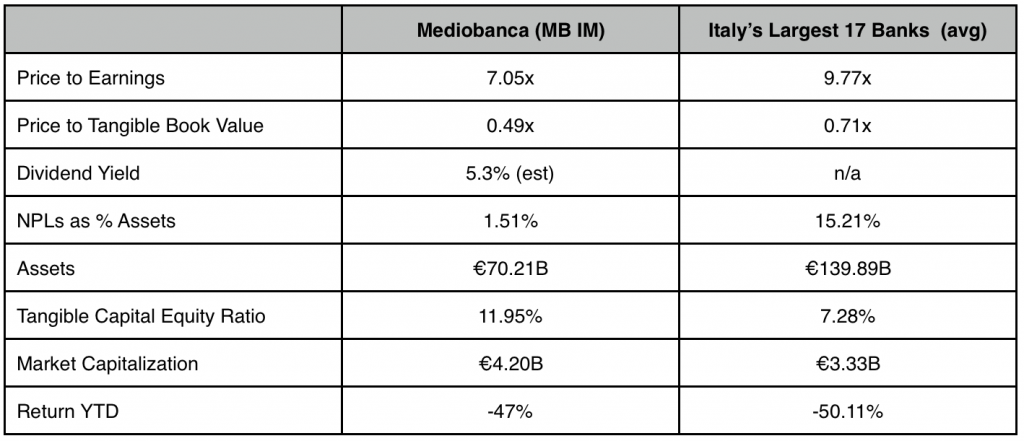

I am generally NOT inclined to jump in and trust Ceasrus Draghius et. al., but one Italian bank in particular may offer value: Mediobanca (MB IM). As already noted, its reported NPLs as a percentage of assets are 1.51%, less than the U.S. average assuming its figures are accurate. The bank has reported 11 consecutive positive earnings quarters, 8 of which showed growth YoY. As a result, it’s profitable and trades at a modest P/E of 7.05x 2016 estimated earnings. Price to tangible book value is just 0.49x, and its Tangible Common Equity Ratio is a healthy 11.95%. In addition, 9 of 13 analysts rate it a BUY with a target of 8.15 (73% upside). It also pays a 5.3% dividend. Here’s how these figures compare to peers:

History indicates Mediobanca has generally been a buy below $5. I am inclined to agree, though I would also add allegro non troppo… not too fast. Go gently.

Mi Amore?

Mediobanca (MB IM)