Last Tree Standing

One Lender Still Faces the Axe

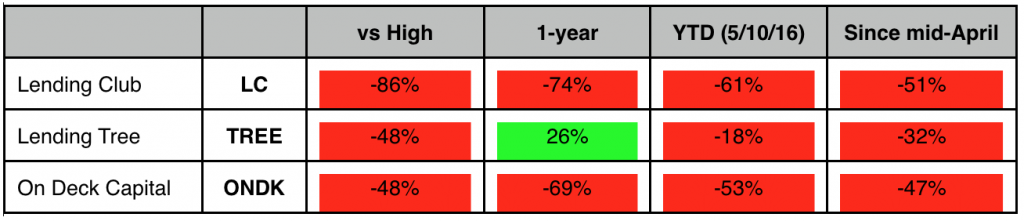

- Online lenders cut in half since April will NOT recover

- Four governmental regulatory bodies now examining marketplace loan practices

- Bloated cost structures undermine the legitimacy of top line growth

- Lending Tree (TREE) will fall to the forest floor like its competitors

Marketplace lenders were supposed to transform borrowing the way Priceline (PCLN) transformed travel, uniting buyers and sellers on a common platform so they could agree on a price and consummate a deal.

There is only one problem: The concept is failing in spectacular fashion. During the first two weeks of May, On Deck Financial, Inc. (ONDK) lost double the estimate for Q1, LendingClub Corp. (LC) fired its CEO for selling $22M of loans which failed to meet investors’ criteria, and underwriters at Goldman Sachs and Jefferies suspended pending loan securitizations. Only Lending Tree (TREE) still stands… barely. All ten analysts rate shares a Buy, but no tree can withstand gale force winds indefinitely.

Relentless Selling

Which of these is not like the other?

If a tree falls in the forest, and no one’s there, does it still make a sound? Answer: Yes, just ask the regulators. Four governmental agencies are now examining the business of online lending, and their prying eyes are sending tremors through the industry. The Federal Trade Commission recently joined Treasury, the FDIC and Elizabeth Warren’s Consumer Financial Protection Bureau in trying to better understand whether consumers might be unwittingly opening themselves up to predatory lending practices.

This bad for anyone still long Lending Tree, as Government tends to have a heavy and indiscriminating hand. Former American Banking Association President Frank Keating told me regulatory changes created by Dodd-Frank legislation “raised operating costs for traditional Main Street lenders by an average of 17%, even though they have nothing to do with capital markets.” Sadly for the marketplace lenders, their business models have everything to do with capital markets, as secondary loan securitization is essential to recycling capital and generating earnings growth.

Now, before we get too bogged down by the negatives (though we’re getting there quickly) let’s start with the noble promise of making more credit more available to more people. Just as companies like Uber and Fresh Direct have harnessed connectivity to enhance fulfillment and customize choice, FinTech innovators have created a number of new platforms to connect consumers and capital more directly. As a result, total online loan origination rose to $37B in 2015, up from virtually zero in less than five years, according to Autonomous Research.

Dozens of private lending companies with names like Rapid Advance and Multifunding LLC now compete online to offer loans with significantly less friction than traditional underwriters. Many of their processes are automated by algorithms analyzing digitized documents on servers far away from expensive branch offices, meaning they can process loans faster and at lower cost than traditional banks. Often, borrowers get approved the same day they apply, and funds are wired within the week. These so-called marketplace lenders have prospered by stepping into the void left by banks still repairing balance sheets after more than $1.1T of write downs since 2008.

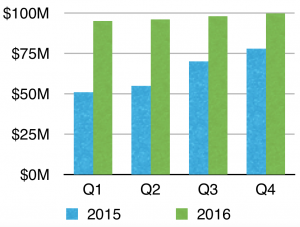

On Deck estimates $80-120B in demand for small business loans went unfulfilled in 4Q16, compared to actual loan volume of $193B. So On Deck has been busy writing business, but as the recent earnings miss demonstrates, buying business at the margin can be very expensive. Loan loss reserves rose and securitization fell, which is a double whammy. Loan quality is falling so fewer people are willing to buy the company’s loans in the after market. To quote J.P. Morgan analyst Richard Shane (who rates ONDK a hold):

“The high level of credit risks inherent is ONDK’s high yield portfolio remain difficult to assess given the company’s reliance on its proprietary algorithm for determining credit risks. As credit risk management is critical to sustaining ONDK’s robust growth, we remain watchful with regard to the effectiveness of its credit assessment algorithms.”

On Deck uses use its own capital to make loans, so its position and opacity make it particularly problematic, which is also why it’s a single digit stock. Lending Tree, by contrast acts as a neutral or third party marketplace, introducing borrowers and lenders. Even so, Lending Tree still faces multiple challenges.

1. Flat Quarterly Revenues

1. Flat Quarterly Revenues

Lending Tree’s top line has gone from Growth Miracle in 2015 to Miracle Gro wanted in 2016. Whereas last year’s revenue rose from $51M in Q1 to $78M in Q4, management recently guided analysts to $95M per quarter this years… for all four quarters. When an exasperated analyst f rom BWS Financial exclaimed, “$95M per quarter for all four quarter means zero sequential growth” the CEO responded “I need to look at the numbers.” So here they are in green, ironically: Zero sequential growth.

2. Extremely High Costs

Anyone who follows Amazon knows that on-line profit margins can be notoriously thin, so thin that supermarkets at 2-3% actually look robust! Welcome to the world of online lending. In theory, operating a marketplace without the burden of branch offices along Main Street should be cheap. It’s not. Customer acquisition is EXTREMELY expensive. Lending Tree spends 59% of revenue on advertising. Lending Tree’s total SG&A expense (Sales, General & Administrative) equates to 80% of total revenue, the second highest of all 1500 stocks in the S&P 1500 Index. Think of it this way, Lending Tree spends 80 cents to make 20 cents, meaning there’s very little room for error. Do YOU want to be in that business?

3. Expensive Middleman

Lending Tree proudly highlights it lending partners in the company presentation. Wells Fargo figures prominently in several categories, as it should… accounting for about one in five mortgages in the U.S. But does Wells Fago really need Lending Tree? It’s already Goliath. And why should lenders like Chase and Citi pay 50-400 basis points per loan for customer introduction? Curiously, On Deck is a Lending Tree customer. So is SoFi, which pitches itself to Millenials in need money as “awesome” and describes markets as “weird.” I remember when institutional stock brokers charged 12 cents/share, and now it’s less than a penny. Real estate brokers once collected 10%. Disintermediation works when process is simplified and cost is lowered, not when a new layer is inserted. Sorry Lending Tree, you are not mission critical.

4. People as Product

I suspect we will learn over time that the four regulatory agencies examining Lending Tree will express concern over fundamental conflicts of interest inherent in the structure of its business. The key issue is its definition of Customer. Per the original S-1 registration document filed with the SEC in 2008:

Access to Supply: Tree.com provides lending and real estate network partners with important customer acquisition channels. Tree.com believes the ability of its partners to reach a large qualifies audience through its brands and businesses is a significant benefit. Tree.com com offers customers the choice of multiple suppliers in one setting.

This paragraph clearly identifies banks are partners of Lending Tree, using the online platform for “customer acquisition.” Several questions arise:

• But does this imply the borrowers are product, or are borrowers customers?

• Are banking partners also customers?

• Can a market place fairly represent both sides without providing total transparency, especially when proprietary algorithms process the data?

• Should we interpret “multiple suppliers” as the banks supplying capital or the borrowers supply

I offer no answers, but I am confident that dozens of lawyers laboring at four agencies can create enough uncertainty and overhang to pressure this sector for a long time. Regulators strung out the debate over for-profit college loan abuse for several years. Similarly, banks are still settling suits from 2008, and even BP is not clear of its 2010 oil spill. This debate will drag on for years.

Bottom Line: Lending Tree is a long-term, structural short position. It’s growth has slowed, its costs are high, it may ultimately prove less relevant to existing partners and regulators have dug in.

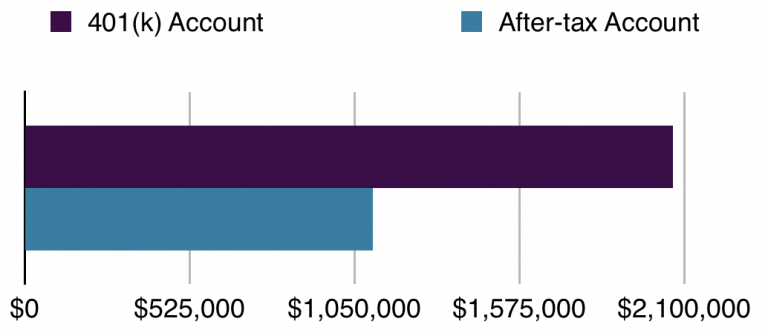

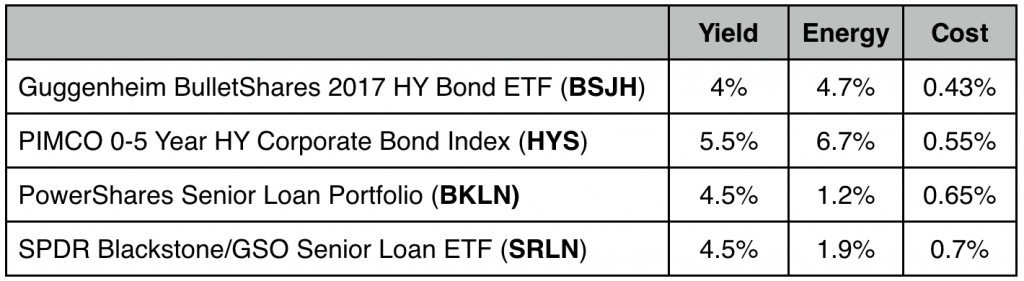

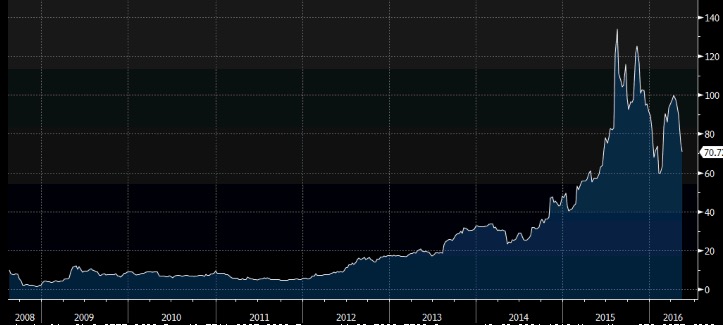

Lending Tree will also prove a challenging position to trade for two key reasons: The company has expressed considerable interest in buying shares in the below $70, as it did during the February sell-off; and short interest exceeds 40% of float, meaning it could be subject to a massive short cover rally. That said, the long-term chart clearly indicates a deteriorating trend and plenty of room to the downside.

Lower Highs & Long Way to Zero

Lending Tree (TREE)

Copyright 2016 Bloomberg Finance L.P.