Sample Issue

Thank you for your interest. Please note that this sample of a past issue is shown for indicative purposes only. Content is not current.

Week of March 8, 2021

Bullseye Brief explores American Ingenuity… people and companies transforming our world. When I find a stock with a Great Story, supported by Compelling Data and a Newsy Catalyst, I write it up as a Bullseye pick and put it in the portfolio. I love what I do.

Executive Summary

Actionable Trades

Buy – ARE,BXP, DAR

Sell – ACLS, ET, URI

Picks Making News

ACLS, CRM, MSFT, PGNY, RXO, UBER, WYNN, XPO

Also in this Issue

Catalysts Next Week

Portfolio Performance

Trader Talk: No Surprise

Bullseye View on Stocks, Bonds, Oil, Gold, Dollar

Bullseye View

S&P 500 Index 4,081 +6.30% YTD

Momentum – January marked the best start to a year in decades, and now the 50-day moving average has crossed above the 200-day ma, signaling a positive change in trend. Earnings are better than feared and rate hikes are nearly done. I recall 2018, when everyone believed recession was inevitable. Then sentiment u-turned. Stocks rose 35%.

10-yr Treasury 3.66% (vs. 1.95% 1-yr ago)

Push-Pull – Bond traders appear evenly divided over whether we’ll see one more or two more rate hikes, pegging the “terminal rate” at 5.10% based on Fed Funds futures. Either way, the Fed is nearly done if inflation continues to decline. So why is the yield curve inverted? Residual stress, lingering price pressures and debt ceiling angst.

Dollar Index (DXY) 103.32 +8.02% (1-yr chg)

Back in the Pool – DXY has finally found its footing, having fallen 14% from October’s 20-year high in response to Fed guidance about an eventual pause in rate hikes. Remember, USD is the world’s reserve currency, and you can only take it down so far before global investors step in and buy… regardless of Fed policy.

Gold $1,864/oz. +1.49% (1-yr chg)

Range Trade #1 – When the dollar falls, gold rises and vice versa… they are substitutes by definition. DXY appears to have stopped falling, so I expect gold to stop rising. Gold is a range trade. It’s a BUY in the $1,600s and a SELL in the $1,900s… it reached $1,950 last week. We’ll never get rich on gold, but it’s a reliable trading vehicle.

Oil $78.78/bbl -12.28% (1-yr chg)

Range Trade #2 – Oil remains under $80 as above-normal temperatures reduce heating oil demand and stalemate in Ukraine whittles away the war premium. Additionally, global producers are making up for lost Russian crude, even Venezuela is being allowed to sell again. Like gold, oil is a range trade. BUY in the low $70s, SELL in the high $90s.

Actionable Trades

BUY

Alexandria Real Estate Equities, Inc. (ARE) – I will add under $170.

Boston Properties, Inc. (BXP) – I will add under $70.

Darling Ingredients, Inc. (DAR) – I am building this new position under $65.

SELL

Axcelis Technologies, Inc. (ACLS) – Rises through my $85 target, so I sell half.

Energy Transfer LP (ET) – Approaching my $14 target, at which point I’ll sell half.

United Rentals, Inc. (URI) – Rises through my $440 target so I sell half.

Access all reports on the Past Issues tab, or search by ticker using the magnifying glass icon upper right.

Picks Making News

Axcelis Technologies, Inc. (ACLS) – Rises to an all-time high as earnings soar past estimates: $1.71 vs. $1.38. Revenues also beat and management raises guidance by 5%, adding revenue will exceed $1B for the first time.

Microsoft Corp. (MSFT) – Releases a new version of its Bing search engine which uses AI-enabled ChatGPT.

Progyny, Inc. (PGNY) – Falls as much as 10% on a report from short-seller Spruce Point suggesting that tech layoffs could halt revenue growth and cause a 60-80% selloff. KeyBanc Capital Markets Analyst Scott Schoenhaus rebuts the argument: “PGNY’s provider network provides a distinct competitive advantage which would take years to build out,” adding layoffs are “nothing new” and “PGNY can keep winning new clients outside of tech, where estimates are already baking in no growth in covered lives for 2023.”

RXO, Inc. (RXO) – Earnings handily beat estimates ($0.28 actual vs. $0.23 est.) despite a slight revenue shortfall, highlighting the operational leverage of this XPO freight logistics spinoff. Gross margins rose 250 basis points to 19.6%. Notably, downloads of its RXO Drive/Connect app rose 45%, and freight brokerage volume rose 4% even as the overall US freight market contracted.

Salesforce Inc. (CRM) – Hedge fund investor Dan Loeb becomes the fifth activist investor to take a large position in the company. This is very positive. The market loves strong handed investors pushing management for growth.

Uber Technologies, Inc. (UBER) – Pops 10% as Q4 earnings of $0.29 blow away the estimate for a loss of $0.11. Revenues are up. Rides are up. Freight is up. Guidance is up. Total booking increased 19% to a record $30.7B… just for the quarter. CEO Dara Khosrowshahi: “We ended 2022 with our strongest quarter ever, with robust demand and record margins.”

Wynn Resorts International (WYNN) – Rises 5% to a one-year high despite missing earnings estimates on the assumption that Chinese lockdowns are over and Macau casinos will recover quickly.

XPO Logistics, Inc. (XPO) – All over the map: Rises 5% initially as earnings beat estimates ($0.98 vs. $0.84) and increase 53% YoY… then falls 12% the next day after conservative guidance by management on freight rates.

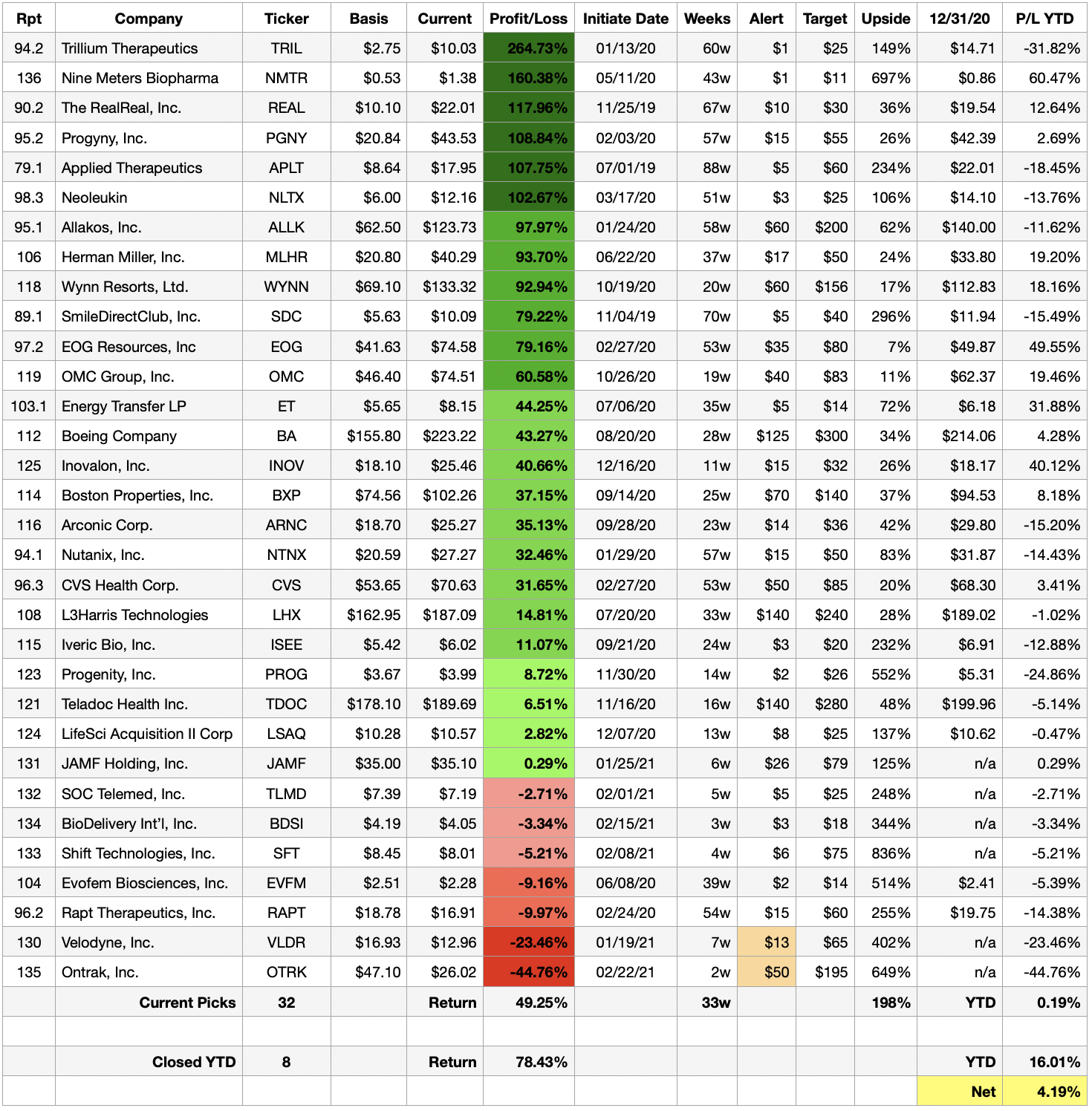

Bullseye Performance

Open Positions – SAMPLE ONLY – NOT CURRENT

Dividends paid and option premium written reduce basis when applicable.

Access all reports on the Past Issues tab, or search by ticker using the magnifying glass icon upper right.

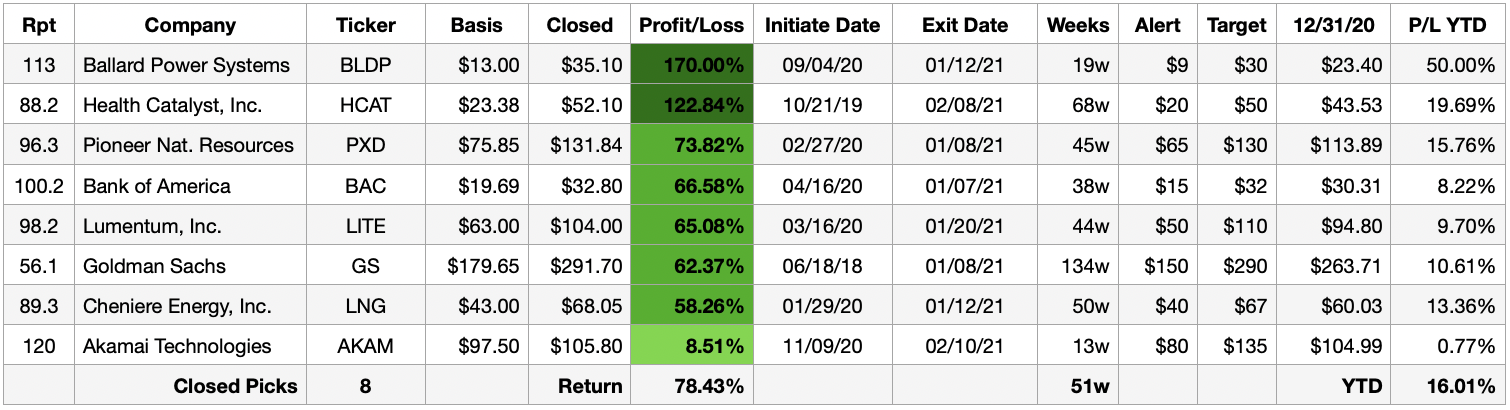

Closed Positions YTD

Catalysts Next Week

Monday

- Normalization – Wholesale Trade Inventories expected to rise 1.2%, consistent with the 3-month moving average.

- This Day in 1855 – First train crosses USA’s first railway suspension bridge in Niagara Falls… American Ingenuity.

- This Day in 2021 – International Women’s Day, sponsored by the UN and promoting “Women in Leadership.”

- Conferences – Citigroup Digital Money / Citigroup Global Property

- Earnings – SFT

Tuesday

- Feeling Better #1 – NFIB Small Business Optimism expected to rebound from the previous month’s 7-month low.

- Conferences – Baird Mobility / BofA Consumer Retail / H.C. Wainwright Life Sciences / Truist Technology

- Earnings – None

Wednesday

- Inflation #1 – CPI MoM expected 0.4% vs 0.3% the previous month.

- Inflation #2 – CPI MoM expected 0.2% vs 0.0% the previous month (ex Food and Energy).

- Inflation #3 – CPI YoY expected 1.7% vs 1.4% the previous month.

- Inflation #4 – CPI YoY expected 1.3% vs 1.4% the previous month (ex Food and Energy).

- Lone Star No More – Texas allows all businesses to reopen at 100% of capacity.

- Conferences – Barclays Healthcare / RBC Global Financing Institutions / Wolfe Fintech.

- Earnings – IBDSI, ORCL, TRIL

Thursday

- Help Wanted – The JOLTS Index expected to show 6.60M job openings vs 6.64M the previous month.

- Conferences – Susquehanna 10th Annual Tech

- Earnings – None

Friday

- Inflation #5 – PPI MoM expected 0.4% vs 1.3% the previous month.

- Inflation #6 – PPI MoM expected 0.2% vs 1.2% the previous month (ex Food and Energy).

- Inflation #7 – PPI YoY expected 2.6% vs 1.7% the previous month.

- Inflation #8 – PPI YoY expected 2.5% vs 2.0% the previous month (ex Food and Energy).

- Felling Better #2 – University of Michigan Consumer Sentiment expected 77.7 vs 76.8 the previous month.

- Conferences – None

- Earnings – NLTX

Trader Talk

Two Timeframes… Two Opposites – Selloffs feel horrible, but they don’t often last long… even the bad ones. The S&P 500 Index has corrected at least 4% on 19 occasions spanning 1-4 weeks since 2016, yet it has remained consistently in an uptrend. The average decline has been about 9%. While last week’s 5% consolidation suggests we’re only half way there, I’d argue that it’s coming on the heels of a 4.5% decline in January and a concurrent 12% decline for the NASDAQ. There’s a bottom in here somewhere.

Stocks are under pressure on concern interest rates will rise. Growth stocks have been hit especially hard, since a higher discount rate implies lower target prices for stocks. I appreciate the logic, but the 10-year yield would have to rise to 3% before discounted cash flow models would cut price targets 10%. That’s along way from here.

Many of my names have fallen double-digits. I have added to some of them. We will get through this period of adjustment to higher rates, and I believe rates will remain relatively low for a long time. I also believe the economy will normalize sooner than many believe. This is positive, but selloffs are stressful.

Podcast

Inspiring Innovation – Scott Kirsner is a best-selling author who founded Innovation Leader to advise CEOs on how to cultivate new ideas within their organizations. As someone who has built an investment platform around American Ingenuity, I want to know his secrets. You’ll get the link at noon.

New Pick: Reinvent Technology Partners (RTP)

Most advanced, electric-powered heli-taxi creates attractive call option on the future of mobility.

Uber in the Sky

SPAC for eVTOL

-

Arial short-haul taxis represent a $500B addressable market in the US and $1.5T globally per Booz Allen

-

Electric helicopters are 100 times quieter and four times cheaper to operate than traditional helicopters

-

5 startups dominate electric Vertical Take Off & Landing (eVTOL) but only one is public and certified to fly

Finally Happening – Everyone is talking about electric vehicles, but the conversation never seems to go beyond cars, trucks and buses… until now. After ten years of privately funded development happening far from prying eyes, electric-powered flight capable of lifting several thousand pounds is now a reality. The FAA has just issued its first-ever certification for an e-copter, and it’s already being used by the Air Force to transport personnel more efficiently across sprawling airbases. The company making it possible wants to introduce an Uber-like service at Uber-like prices over the next several years, but its corporate SPAC parent already trades today. I want to be clear: This is big picture, high risk and long term… but the numbers do make sense. It’s a great example of American Ingenuity, and I’m a buyer.

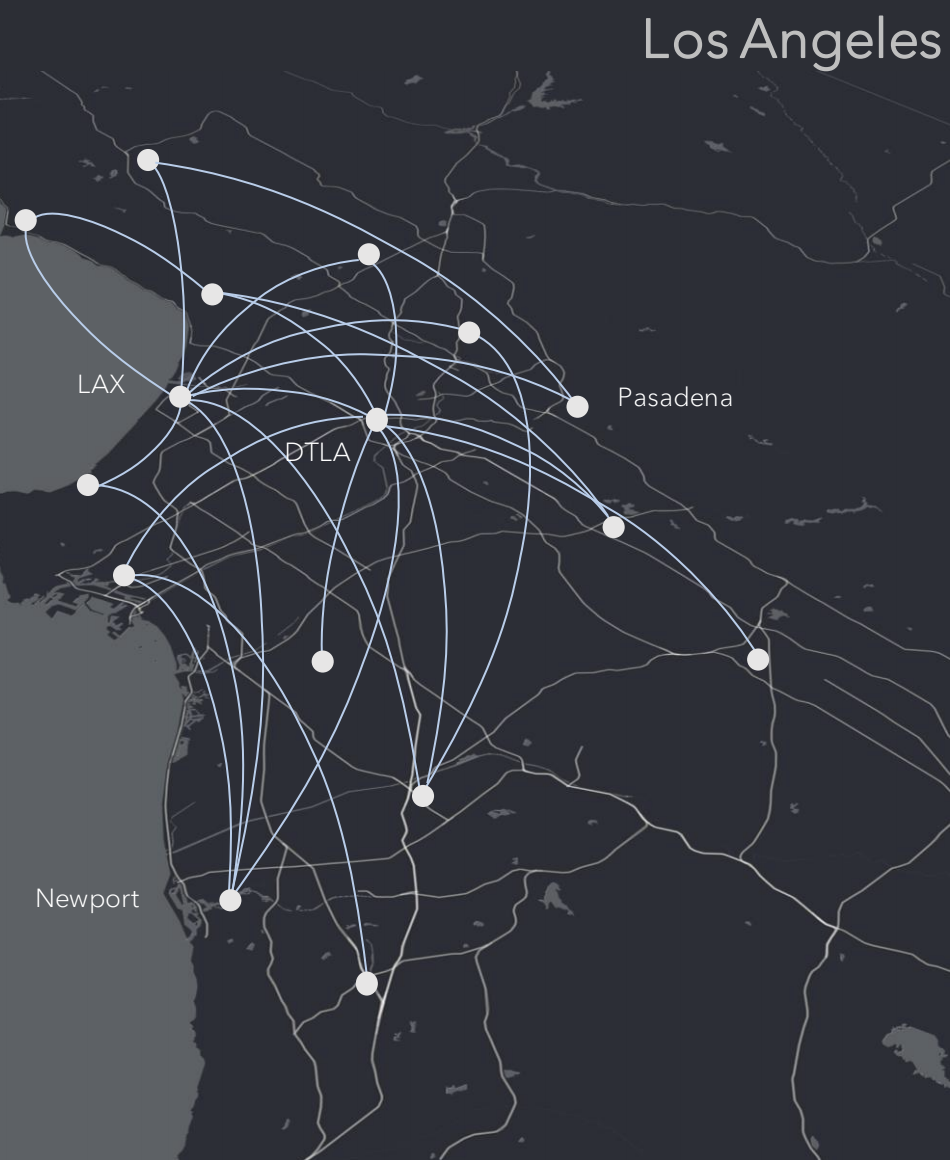

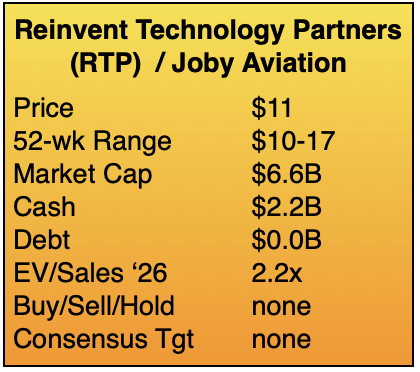

Reinvent Technology Partners (RTP) is the SPAC created by LinkedIn Co-founder Reed Hoffman and Zynga Founder Mark Pincus, which on February 24 announced a $6.6B transaction to acquire Joby Aviation, the world’s first Electric Vertical Takeoff and Landing (eVTOL) manufacturer to receive FAA certification and US Air Force airworthiness. The company aims to launch commercial service by 2024, operating short-haul flights priced similarly to UberX… with the energy efficiency of a Tesla… while cutting travel time by 75% for the typical 25 mile trip. Joby will build and operate its own fleet, initially ferrying travelers between airports and large urban centers like Los Angeles and New York. Joby’s ultimate goal is to revolutionize mobility across the globe, providing a green solution which saves a billion people an hour a day.

Joby Works Like Uber

Similar Price… But Faster

I’ll start with the basics… how the thing flies. Joby’s eVTOL is like a giant drone you’d fly in your backyard, with six electric powered motors driving six independent rotors. The difference is that its rotors tilt up to enable heavy vertical lifting, then down for horizontal cruising speeds of 200 mph. Incredibly, the six motors are about as loud as rustling leaves even at full throttle, and the entire apparatus can be controlled with a single joystick. There are significantly fewer moving parts to maintain compared to a traditional helicopter, and multiple rotors ensure stability as well as safety, since each operates independently and 4-5 functioning rotors can still land the aircraft safely should 1-2 fail mid-flight. Lithium batteries provide a 150-mile range, and can be recharged quickly. Each aircraft is designed with a ten year lifespan in mind, operating 12 hours a day with 7 hours of flight time.

Joby’s business model calls for a fully-integrated vertical enterprise. Joby engineers will design and manufacture the vehicles, while Joby pilots will operate them, and Joby personnel will manage people moving through Joby-owned transportation hubs. It’s a complete proposition, requiring enormous coordination. Imagine if Boeing not only built airplanes, but also operated an airline and ran its own airports.

Joby’s business model calls for a fully-integrated vertical enterprise. Joby engineers will design and manufacture the vehicles, while Joby pilots will operate them, and Joby personnel will manage people moving through Joby-owned transportation hubs. It’s a complete proposition, requiring enormous coordination. Imagine if Boeing not only built airplanes, but also operated an airline and ran its own airports.

The approach is monumental in scope, and explains why dozens of mechanical engineers from Toyota have joined dozens of electrical engineers from Intel to build the necessary infrastructure. Recall Joby bought Uber Elevate last year (Uber’s homegrown helicopter service), and several dozen software engineers are bringing their operational experience as well. Each of these partners is an also an investor, JetBlue included… which sees Joby as a way to get more passengers to the airport and into its planes. Curiously, Uber intends to integrate Joby into its app and collect passengers from around town, dropping them at Joby eVTOL depots for their flight. It’s a team effort, and the partners all want a piece of the action. I like institutional buy-in… more vested interests pushing for success.

Transformation… Not Transportation

Leaders, Investors and Partners

Now let’s talk numbers. The RTP acquisition of Joby provides an infusion of capital which will give Joby total cash on-hand of $2.1B, enough to fund development an an initial fleet of 40 vehicles ferrying Bay Area passengers to SFO and/or Los Angeles travelers to LAX. The company WILL need to raise capital at that point, and it WILL be dilutive. The hope is that excitement will be sufficient to drive shares materially higher in advance of a capital raise. Given what’s at stake, I could also see current partners leading another round, which would probably be well-received.

Now let’s talk numbers. The RTP acquisition of Joby provides an infusion of capital which will give Joby total cash on-hand of $2.1B, enough to fund development an an initial fleet of 40 vehicles ferrying Bay Area passengers to SFO and/or Los Angeles travelers to LAX. The company WILL need to raise capital at that point, and it WILL be dilutive. The hope is that excitement will be sufficient to drive shares materially higher in advance of a capital raise. Given what’s at stake, I could also see current partners leading another round, which would probably be well-received.

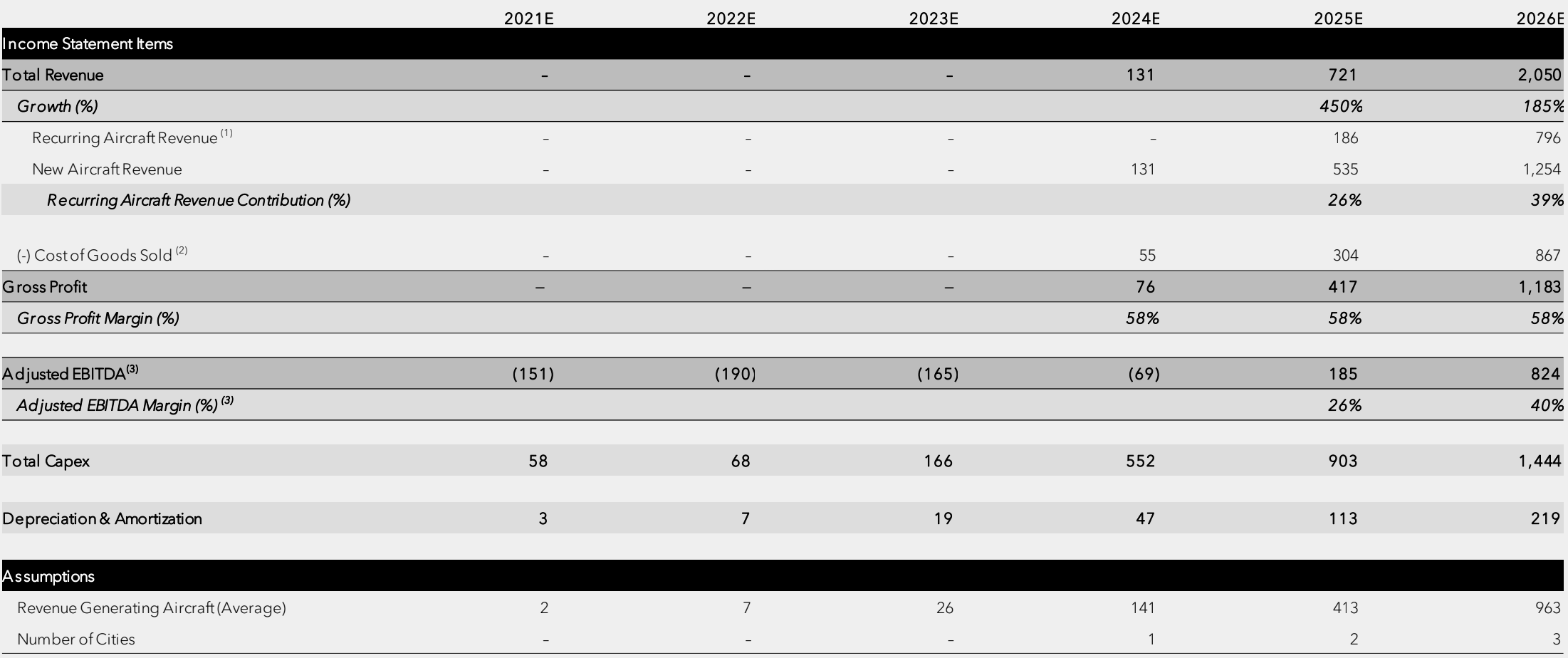

Each aircraft will cost $1.3M to build once the manufacturing plant is operating at scale, which Joby estimates will be 2025… plant permitting and initial ground breaking in CA are already underway. Critically, Joby believes that individual eVTOLs will be able to generate $2.2M in topline revenue annually, implying a 1.3 year payback. This assumes an average trip cost of about $40 ($3/seat mile and 2.4 of 4 seats filled), which is potentially cheaper than an UberX from Newport Beach to LAX and 3-4 times faster. Joby projects 963 eVTOLs will generate $2B in revenue by 2026, the first year it should be judged as viable. Granted, these are all Joby’s numbers, but we have to start somewhere.

Joby’s Commercial Ramp

…According to Joby

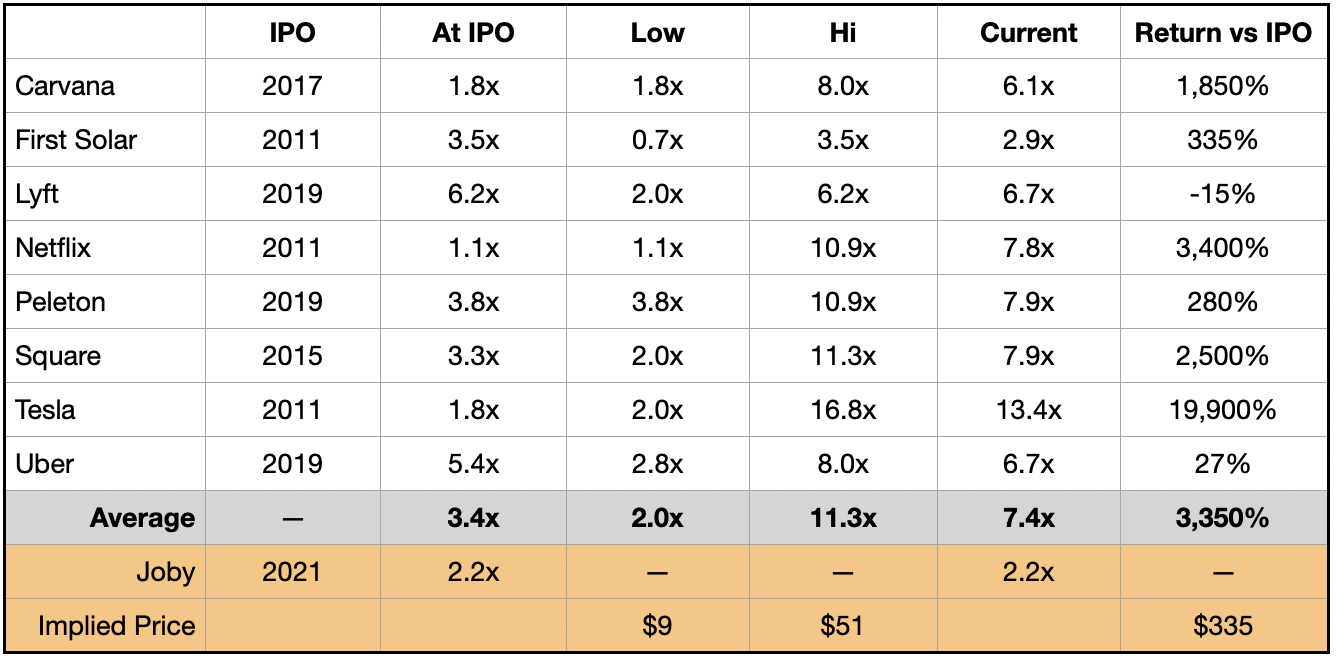

On the surface, Joby looks cheap… though there a MILLION variables at play here. If Joby’s pro-forma estimates are accurate, the company will generate revenues of $2.05B in 2026. Given a current capitalization of $6.6B and cash on-hand of $2.1B, Joby trades at a 2.2 times Enterprise Value to Sales (($6.6B – $2.1B) / $2.05B). Again, that’s pretty cheap relative to where other highly disruptive companies traded when they too were at Joby’s stage.

What’s Fair Value?

Disruptor EV/Sales

Assigning a price target to a theoretical company like Joby may seem like a reach, but it’s an important exercise. I am using the company’s own guidance, which pegs valuation currently at a 2.2 times 2026 sales estimates of $2.05B. I then compare this valuation to the EV/Sales multiples of other notable disruptive companies. Joby’s 2.2 multiple looks cheap relative the average multiple of 3.4x at the IPO, but inline with where companies traded on their lows. This is good from a value perspective… Joby is near the bottom of its expected range. On the high end, disruptive peers have traded at an average of 11.3x, which would imply a $51 target for Joby. I’d be thrilled with a 500% return.

RTP founders Reed Hoffman and Mark Pincus are fully committed. Their respective lock-ups in this transaction (the amount of time which must pass before they can sell their shares) is five years… many magnitudes longer than the standard 6 month holding period. Additionally, they have stock options which don’t even vest unless the stock appreciates to $40-50. In other words, they are playing for a moonshot… like Tesla. Clearly, their interests are aligned with ours.

The Trade

Buy Reinvent Technology Partners (RTP) $9-11 with a $50 target and an $7 alert.

I will build my position thoughtfully. High-potential / High-risk NASDAQ names are getting sold right now because investors are worried that rising rates will deflate the value of their investments. While short-sided… rates are still exceptionally low and the economy is rebounding… I want to be sensitive to what’s happening. Additionally, the Joby platform will take time to come together. As a result, I’ll pick my spots and build my position gradually.

I will build my position thoughtfully. High-potential / High-risk NASDAQ names are getting sold right now because investors are worried that rising rates will deflate the value of their investments. While short-sided… rates are still exceptionally low and the economy is rebounding… I want to be sensitive to what’s happening. Additionally, the Joby platform will take time to come together. As a result, I’ll pick my spots and build my position gradually.

My target of $50 implies a multiple of sales more inline with other highly disruptive companies as noted above… 11.3x compared to 2.2x currently. Joby could certainly see upside well beyond $50, especially considering that Joby’s disruptive peers have risen an average of 3,350% above their own respective IPO prices. At this early stage, I’m comfortable with a $50 target,

RTP’s acquisition of Joby will result in a one-for-one stock exchange, where each RTP share will convert into one Joby share, and the transaction is expected to close April-May. No analysts cover Joby currently, but I suspect this will change after the closing. ![]()

Still on the Ground… Ready to Fly?

Reinvent Technology Partners (RTP)

Subscribe at BullseyeBrief.com

-

Enjoy a Free 45-Day Subscription to Bullseye Brief

- Click Here