Separation Anxiety

Miners Too Far Ahead of Gold

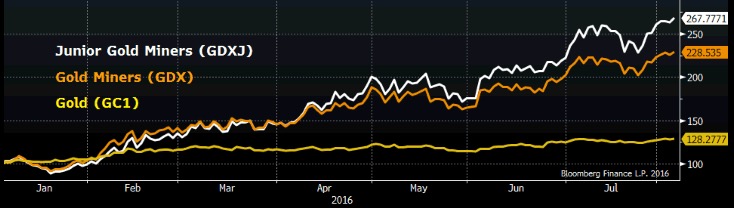

- Mining stocks have rallied five times more than gold year-to-date

- Incremental gold demand in 2016 has been driven largely by flows into exchange traded funds

- Poor profitability among mining companies undermines current valuation

- Options market offers attractive ways to establish short exposure

Anyone who bought gold mining stocks at the beginning of the year is a hero. The big companies like Newmont (NEM) and Barrick (ABX) are up 127% on average. The smaller takeout candidates, often called the junior miners are up even more –about 165%. No other sector even approaches triple digit returns this year. Granted, the sector peaked in 2011, so investors have had to wait five years for redemption. In addition, many of the miners still sit well below all-time highs, but this year’s windfall feels pretty good. The operative question at this point: How far will they go, or how long will this last?

Newmont Mining CEO Gary Goldberg took a stab at providing an answer during the company’s 2Q earnings call on July 20. As you might expect, he’s bullish.

“Low or even negative real interest rates are making gold an increasingly attractive investment. Concerns about slower global economic growth and weaker domestic employment have forced the Fed to be more cautious about raising interest rates. The markets now anticipate no or at most one rate hike in 2016. Inflation is also trending upward. We’re seeing more money flowing into gold on the back of these trends… global ETF gold holdings have increased by more than 17 million ounces or nearly 40%.”

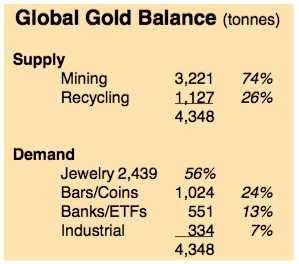

Mr. Goldberg is correct about the surge in demand from financial buyers, most notably by administrators of exchange traded funds needing to purchase gold in order to issue more units against investor inflows. You can see financial buying accounted for about 13% of demand in 2015, much of which came from central bankers, whereas this year it’s all about the ETF, 336 tonnes worth of buying in Q1. (The supply/demand balance tends to vary by about 10% from year to year, based on demand tracked by Bloomberg from the World Gold Council.) Incremental demand so far in 2016 has been enough to drive the price of gold 28% higher. It’s impressive, but there’s also a disconnect… the mining stocks are up 5 times more. I recognize they have operating leverage… but 5x?

Mr. Goldberg is correct about the surge in demand from financial buyers, most notably by administrators of exchange traded funds needing to purchase gold in order to issue more units against investor inflows. You can see financial buying accounted for about 13% of demand in 2015, much of which came from central bankers, whereas this year it’s all about the ETF, 336 tonnes worth of buying in Q1. (The supply/demand balance tends to vary by about 10% from year to year, based on demand tracked by Bloomberg from the World Gold Council.) Incremental demand so far in 2016 has been enough to drive the price of gold 28% higher. It’s impressive, but there’s also a disconnect… the mining stocks are up 5 times more. I recognize they have operating leverage… but 5x?

Conscious Uncoupling

In fairness, companies like Newmont Mining have been particularly adept and lowering costs and paying down debt during the four year gold implosion which haunted them from 2011 to 2015. They’ve shuttered marginal mines and generally brought all-in sustaining costs (AISC) down to $700-800/oz from well over $1,000/oz. In the case of Barrick Gold, net debt has fallen from $10.4B in 2014 to about $7.5B currently. Overall, mining companies have done a good job retooling their businesses to prepare for leaner times, realizing like so many others $2,000 gold wasn’t the slam-dunk markets had assumed.

It’s a very different scene from 2010, when I interviewed then-Newmont CEO Richard O’Brien at the BMO Metals & Mining Conference for Bloomberg Television. He had just wound down the last of Newmont’s hedges (impeccably timed) and proudly announced he did so because investors told him they wanted exposure to gold, not financial wizardry. They certainly got it… albeit in a different way.

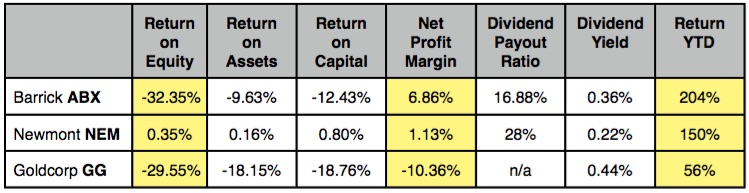

Here’s the thing about gold investors: When they buy, they think gold is going to make them rich. It’s not about double-digit earnings growth or cheap NAV, it’s about runaway inflation or the end of fiat currency and only gold will protect them. $2,000 gold? More like $10,000 gold. Take a look at the metrics for the three largest mining companies in the ever popular VanEck Gold Miners ETF (GDX), whose daily average volume of 73M shares makes it one of the most active equity securities in the world.

You Want to Own These?

Q1 Profit Metrics

The profitability metrics on these companies are AWFUL, and by the way there’s no dividend to speak of because there are virtually no earnings. Obviously investors see something else… I love Goooooooooold.

Okay, I admit an average price to book ratio of 2.09 for the miners in the GDX and 1.96 for the smaller companies in the GDXJ is not unreasonable. It’s neither rich relative to the S&P 500 Index nor to the historical range for the sector. In addition, I fully recognize the appeal of gold against the backdrop of rising sovereign debt due to global money printing by central banks. I will also grant that all this money printing may one day stoke inflation, against which gold should provide a hedge. Fine.

But let me say this: I do not want to own marginally profitable mining companies already up 150-200% YTD on the “hope” gold rallies further. In fact, I want to short them, and the analyst community would appear to agree. Many of the stocks within the GDX and GDXJ are trading at/near consensus targets. They’ve had their run and it’s time to sell. Here’s how we do this:

1. Buy puts on the GDXJ funded by selling calls. I like Sep 50 puts vs Sep 53 calls at even money (both $2.80) with the index at $51.00. This combo give us a little cushion and costs nothing initially.

2. Buy long-dated GDX Nov 29 puts for $1.90 and forget about them. The index is at $31.25 so the breakeven is -12.58% and if the miners break, this option will accelerate quickly (33 delta currently).

3. Short a little Couer Mining for fun at $15.75… it’s up 535% YTD.

Subscribe at https://bullseyebrief.com