Check-Out Time

6 Hotel Operators to Short

- 7 years of rising Revenue per Available Room (RevPAR) implies hotel growth is late cycle

- Average U.S. room rate increases of 2.4% in May are the lowest since 2010

- Hotel rooms currently under construction and/or in planning will increase total U.S. supply 10%

- Minimum wage and AirBnB introduce significant structural challenges to hotel profitability

Several hotel-focused real estate executives have shared surprisingly candid concerns with me in separate conversations over the past several months. They tell me the luxury urban hotel market is oversupplied, prices paid by developers have been far too high and borrowers with weak balance sheets are about to get a very loud wake-up call. Had I not been privy to their insight, I might not have noticed. The industry‘s benchmark measure of Revenue per Available Room (RevPAR, or Rate x Occupancy) has risen each of the past seven years, the longest ever recorded cycle based on Bloomberg Industries data. Plus, hotels I visit for business are often near capacity, and just last week I got bumped on an overbooked flight to Chicago. As far as I can tell, the big city hotel biz looks pretty good.

Thank goodness for the experts, and their willingness to set me straight. Whereas I see construction cranes moving across a downtown sky as a sign of deep-pocketed institutions making significant longterm capital investment, the pros see development run amok. That 7-year high is their 7-year itch. Stepping back for a moment… #AsGoodAsItGets?

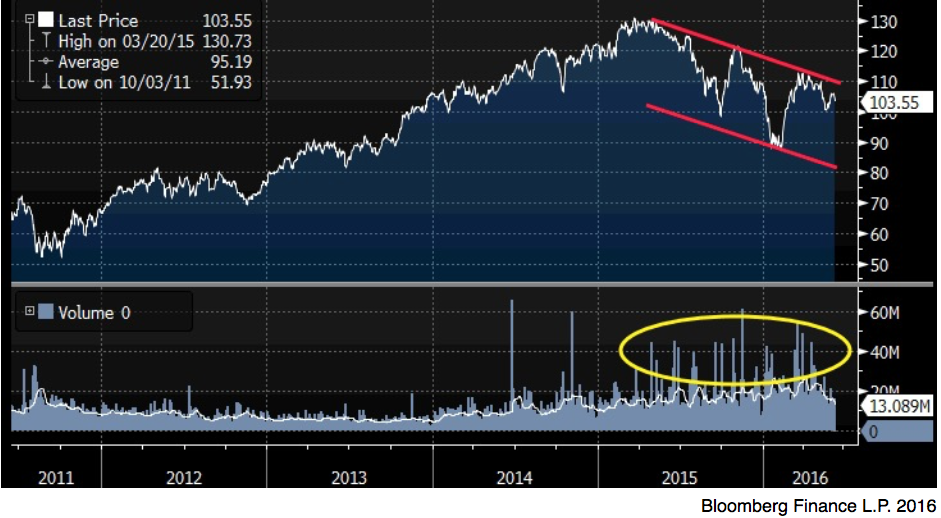

Maybe so, and investors have clearly begun to express concern. Hotel REITs –which generally own the underlying real estate and pay mid-single digit dividends– have declined over 25% from their all-time high. That’s a powerful message in a rate-stared environment. In addition, the stocks have sold off on higher volume. Again, a strong message.

Checking Out

Bloomberg Hotel Index

Oversupply

To appreciate investor’s concerns, just drive around Manhattan… or Houston, or Denver, or Portland. Construction-related traffic jams in New York City this summer have become impenetrable. Along Tenth Avenue in the 30s I recently counted 13 cranes hoisting steel as part of a Phase I redevelopment around the old Hudson Yard Railroad facility. Planners promise a new “city within the city” and when I shared my impressions with the CEO of a noted real estate development company, he told me many of those structures were financed at 2-4% cap rates (property net operating income divided by purchase price).

This means you’d need to own that building for 25 to 50 years and run it at full occupancy with no unexpected capital expenditures just to re-coop your initial investment… inflation not included. Cap rates this low are historic and likely unsustainable, which is why my friend turned down several opportunities to participate. He believes the combination of high prices paid and optimistic assumptions about growth will ultimately force several of these projects into default.

Consider this nugget from the New York Building Congress 2016 Annual Report, entitled “Sky’s the Limit.” Attention bulls: The following material is graphic in nature. Reader discretion is advised.

An amazing $40 billion worth of construction projects were initiated across the five boroughs in 2015, and the New York Building Congress forecasts construction spending will increase even further to $41 billion in 2016 and $40.8 billion in 2017. More new office space is being built than at any other point in the past quarter of a century. Spending on residential construction is at an all- time high and is likely to produce more than 90,000 new units between 2015 and 2017. New hotel rooms have been added at a blistering pace.

What’s happening in New York is hardly unique, and two key numbers prove the point:

1. U.S. non-residential construction spending of $688B is within 6% of the all-time high in 2008 (Census Bureau).

2. 509,626 new hotel rooms currently in planning and/or under construction will increase the total number of available rooms in the U.S. by 10% to 5.58M, according to figures tracked by hospitality research firm STR, Inc. The current construction/planing figure represents an increase of 19% compared to last year. READ THAT AGAIN PLEASE… the 10% part.

New supply pushes prices lower by definition, and Q1 rate increases nationally of 2.4% indicate the slowest advance since 2010 (Smith Travel and Bloomberg data). Even if the economy resumes 3-4% growth and corporate earnings break out of the cur rent 3 year slumber, hotels have to contend with competition from AirBnB, which now lists over 2M properties. While the company does not break out U.S. listings, its current global inventory equates to one-fifth of all U.S. hotel rooms. That is what we call a 500-pound gorilla, and its chest pounding serves as a warning to hoteliers they are expanding at exactly the wrong time.

New supply pushes prices lower by definition, and Q1 rate increases nationally of 2.4% indicate the slowest advance since 2010 (Smith Travel and Bloomberg data). Even if the economy resumes 3-4% growth and corporate earnings break out of the cur rent 3 year slumber, hotels have to contend with competition from AirBnB, which now lists over 2M properties. While the company does not break out U.S. listings, its current global inventory equates to one-fifth of all U.S. hotel rooms. That is what we call a 500-pound gorilla, and its chest pounding serves as a warning to hoteliers they are expanding at exactly the wrong time.

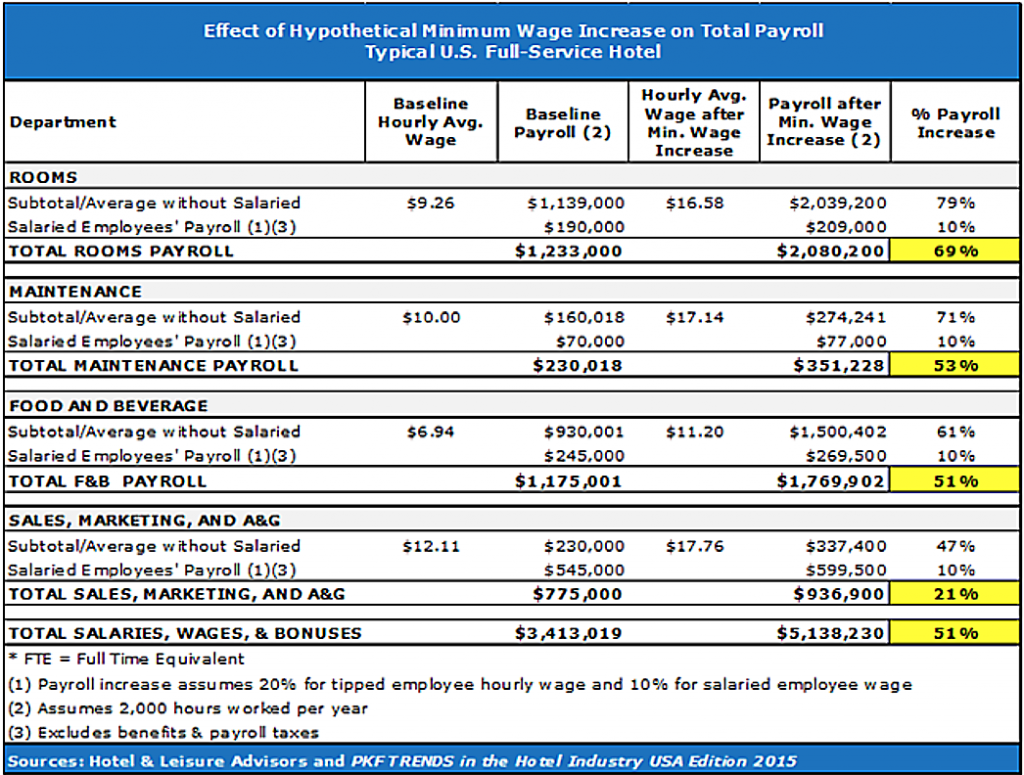

Recent minimum wage increases also present a major headwind for hotel owners and operators. www.hotelonline.com published a case study on how raising minimum wage to $15 would increase labor costs by 51% for a standard 248 room full service hotel. Since labor represents a hotel’s single largest cost component, the analysis suggests hotels will struggle to maintain profitability —

Recent minimum wage increases also present a major headwind for hotel owners and operators. www.hotelonline.com published a case study on how raising minimum wage to $15 would increase labor costs by 51% for a standard 248 room full service hotel. Since labor represents a hotel’s single largest cost component, the analysis suggests hotels will struggle to maintain profitability —

and with the economy growing <3% and supply rising 10%, raising rates isn’t viable.

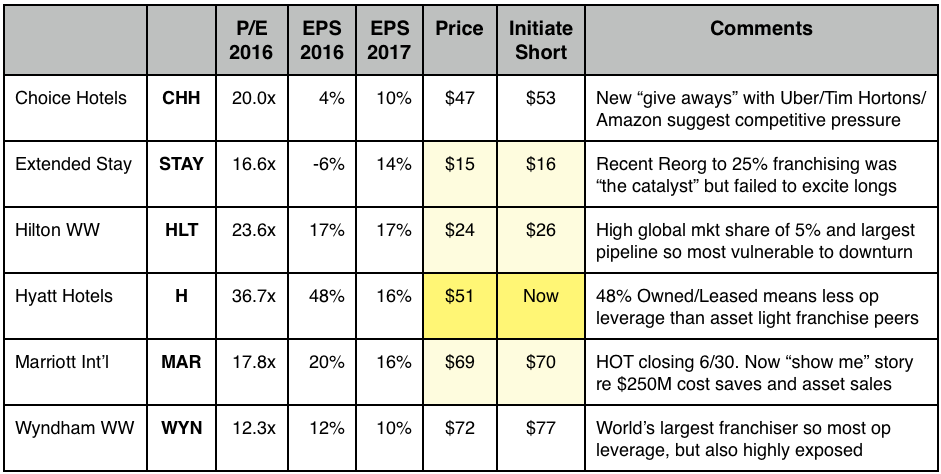

The Trade: Short the Operators

Hotels companies come in two varieties: Operators and Owners. As an example, Marriott International (MAR) manages reservations and guest services whereas counterpart Host Hotels & Resorts Inc. (HST) owns the property, plant and equipment. HST is about steady income and long-term real estate appreciation. MAR offers investors greater cyclical upside through operating leverage… in a rising market. Since shorting stocks which pay 4-7% dividends is NOT my idea of fun, I focus on the operating companies. Both groups have trended lower since last year’s peak and now trade in a very specific channel of lower highs and lower lows, giving us reasonable clarity on when to initiate short positions.