Here Today…Here Tomorrow

Buy Sprint Bonds Now

- Operating income turns positive for first time in 9 years on enterprise-wide restructuring

- Price cuts and leasing drive subscriber growth to 3-yr high while churn to 20-yr low

- Sufficient near-term liquidity and deep-pocketed parent Softbank underscore solvency

- Sprint’s Jewel in the Crown is 2.5 Ghz spectrum valued at nearly three times enterprise value

Sprint wants you to know they’re here to stay, and they’ve even hired Verizon’s geeky pitch man to prove the point. His now famous tagline “Can you hear me now” will begin morphing into “Almost as good at half the price.” Okay, I’m kidding. But that’s effectively the pitch to consumers, and it’s based on Nielsen data ranking Sprint within 1% of Verizon for reliability across 104 major U.S. markets. As for cranky investors who’ve seen shares fall below $4 and yields rise above 12%, copywriters should start drafting comments about cash flow and assets. If you dig through the numbers, you will likely conclude this company is no where near Ch. 11, as the gloom crew predicts. I’m no pitch man, but if I were writing their ads I’d say simply “Buy the Bonds Now.”

I too approached Sprint skeptically at the onset, but pivoted from Doubter to Buyer once I recognized three compelling pillars which uphold Sprint as a dynamic and viable long-term enterprise:

1. More than enough capital to meet commitments through 2017

2. A committed and well-capitalized majority owner

3. Three times its own enterprise value in high quality 5G spectrum

Let’s first address the near-term, Sprint’s capital flows over the next 2 years. Using both public filings and some excellent research from J.P. Morgan Telecom analyst Philip Cusick, CFA, here’s the picture.

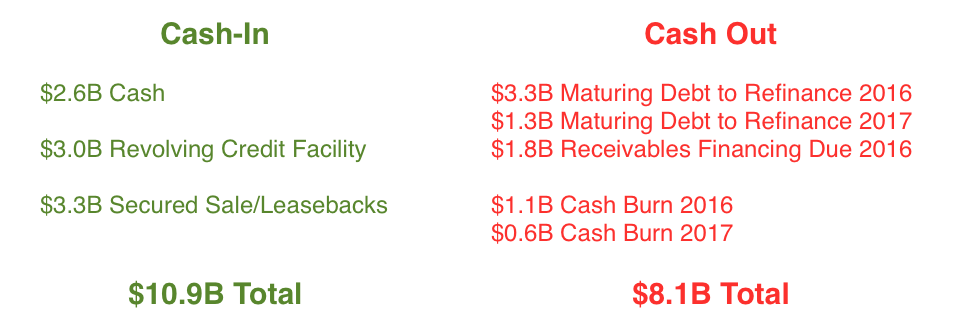

Show Me the Money

Sprint Liquidity 2016-17

The message here is clear: Sprint is NOT GOING OUT OF BUSINESS. With $2.8B in demonstrable liquidity through 2017, Sprint has plenty of breathing room to operate, invest and even expand. To quote JPM’s Mr. Cusik “Sprint has sufficient liquidity to work at it for at least the next 18-24 months and we are warily optimistic.” If his use of the word warily concerns you, recognize Sprint’s $31B in outstanding debt makes it the single largest U.S. high yield issuer, with half of its bonds trading at distressed levels (greater than 10%). So nay sayers have been leaning on all levels of the capital structure, though the benchmark 7 1/8 coupon bonds due in 2024 have rallied 15-20% since February lows on better than expected Q1 results.

Near-Term Fundamentals

First quarter results demonstrated Sprint’s restructuring plan is working, as management raised EBITDA guidance for 2016 to $9.5-$10B from $8.1B. Sprint has been actively driving customers to leasing plans from outright purchases which it previously had to subsidize. It has also created a leasing subsidiary which buys phones for handset makers, leases them to customers and then securitizes the cash flow as an asset backed-transaction. Japan’s Mizuho Securities led these two most recent MLS transactions and we will likely see more.

Additionally, Sprint has targeted $2B in cost savings through 2017 as it streamlines operations across each unit. The CFO has even set up a separate cost control War Room where every single layer is analyzed enterprise-wide. So far, the $250M quarterly run rate is right on target. Admittedly, the one thing we don’t like is lowered capex spending from $5B to $3B because it slows the move to 5G, where Sprint’s superior 2.5GHz spectrum is its jewel in the crown (more on this on a moment).

Additionally, Sprint has targeted $2B in cost savings through 2017 as it streamlines operations across each unit. The CFO has even set up a separate cost control War Room where every single layer is analyzed enterprise-wide. So far, the $250M quarterly run rate is right on target. Admittedly, the one thing we don’t like is lowered capex spending from $5B to $3B because it slows the move to 5G, where Sprint’s superior 2.5GHz spectrum is its jewel in the crown (more on this on a moment).

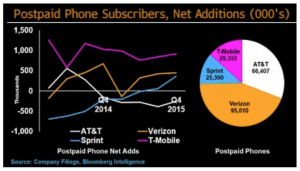

As for Sprint’s core business of signing up people for wireless service, net subscriptions YoY have risen for 6

consecutive quarters. Critically, Sprint is adding subscribers, as opposed to simply no longer losing them at lower rates. Yes, Sprint is actually gaining subscribers… 22k in Q1 (blue line). Note the head to head decline versus

AT&T (white line). Equally important, the savage price war which has cut the cost of plans in half since 2013 may have hit bottom. Ultra aggressive discounter T-Mobile has quietly begun raising data plan prices by $5-15 per month. In a business where four providers provide nearly 100% of the service (AT&T, Verizon, T-Mobile, Sprint) even small price increases are significant.

Long-Term Fundamentals

The massive increase in the flow of data has forced carriers to pursue multiple new approaches to wireless transmission. This includes aggregation, where carriers compress data and consolidate channels into a single pathway. It also means beaming signals directly versus random scanning, and creating micro cells in tight urban environments. Phd types from M.I.T. refer to these new protocols as densification, and suffice to say no U.S. operator has more spectrum depth to “densify” its network and deliver more capacity than Sprint. This is due to its market leading ownership of 2.5 GHz spectrum essential to driving data across next generation 5G networks.

Bloomberg Intelligence analyst John Butler estimates the value of Sprint’s 5G spectrum at $137B, which is nearly three times Sprint’s entire enterprise value of $46B. So if Sprint suddenly filed Ch. 11 tomorrow and liquidated assets, a judge would be in the highly unusual position of sorting out who gets $109B in cash, assuming the spectrum went on the market and attracted competitive bids. John’s estimate is based on comparable valuations for recent secondary market transactions. He says even if he uses a more conservative approach, comparing Sprint’s spectrum to AWS-3 bands, he still pegs the value at $85.6B. Since Sprint owns more 2.5Ghz spectrum than its competitors, and this spectrum is essential to

future 5G buildout, I would argue Sprint owns more “future” than its competitors. I want to own a piece of Sprint, and I think high yielding bonds are the best way to get paid for my involvement.

One more critical point before I get to my two trades…

Never underestimate the impact of a mentor. Mentors open doors, run blocker, mend fences and in some cases mentors help make ends meet. Sprint has a mentor in SoftBank CEO/Founder Masatoshi Son. SoftBank owns 83% of Sprint and currently has $22B of cash on its balance sheet. It also owns 28% of Alibaba (even after its recent 4% sale which raised $8.9B in cash). The point here that Sprint has a very deep-pocketed and well connected parent. While rating agencies debate the staying power of Sprint, I say simply look to the parent. Saving face is a deeply-rooted cultural identification in Japan, and the thought of a highly visible Japanese parent letting an investment of Sprint’s magnitude go under is simply

unthinkable. If things really got bad, Sprint could certainly turn to SoftBank.

So… rising EBITDA, growing subscriber base, successful restructuring, valuable assets, wellcapitalized parent and sufficient cash flow to meet debt service and capital investment —> That’s Sprint.

The Trade

1. Buy Sprint 8 3/8 bonds of 2017 yielding 5.24%. These bonds provide more than adequate compensation at 5.24% for a business which clearly has sufficient capital to operate and grow between now and next summer (August 2017 maturity).

2. Buy Sprint 7 1/4% bonds of 2024 yielding 11.43%. This long-term position provides both compelling yield AND the opportunity for significant capital appreciation. It offers the most attractive “convexity” of the longer term bonds, a fancy way of saying “bang for the buck.” Convexity measures the relationship between price and yield. In this case, a 300 basis point decline in yield (meaning the market perceivesless risk and bids up the bonds thereby reducing yield) would generate a 20% increase in price. That’s bang for your buck. So you’re being compensated near term for what I believe is quantifiable risk, and offered the possibility of significant capital growth as perception of Sprint improves.

As for the equity, it’s less compelling. There is no dividend and earnings per share are flat. Sprint is less about operating growth and equity appreciation, more about viability and cash flow. I like Sprint’s bonds, particularly at these yields.