Summer Fever

Five Cowbells of Caution

- Equity strategists struggle to stay bullish as mid-year forecasts reveal 2.5% upside

- Defensive strategies producing superior returns across multiple asset classes

- Shareholder payouts exceed corporate profits ahead of fifth likely quarterly earnings decline

- Bond markets telegraph low rates for longer

“I got a fever, and the only prescription is more cowbell.” Will Ferrell is hands down my favorite SNL star of all-time. Ron Burgundy, Ricky Bobby, Buddy the Elf… on and on. But Cowbell guy still gets my vote as the best Will Farrell character ever. Sorry Alex Trebek. Yes it was completely stupid, it was also totally brilliant. http://www.nbc.com/node/209806/video/1119596?auto=true#vc214886=1 Turns out, the bell-ringing metaphor was also strangely apropos. “Cowbell” aired on April 8 of 2000, just days after the NASDAQ logged its infamous tech top. I’m not saying SNL is really that good, but I am saying this market’s got a little fever, and I’m hearing pros ring cowbell.

I spent part of my July 4th weekend catching up on a few dozen research reports from some of the top strategists on Wall Street. This is an essential component of my due diligence, and since markets were closed I was able to concentrate without the usual interruptions. Things were going great, but after a couple hours I started getting antsy. So many smart people were expressing unease about markets and money flow, plus they were backing it up with data.

This is exactly how I myself have been feeling lately. Call it aches and pains, and while a fever may not put us in the hospital, but it can still make for some severe unpleasantries… just look at the 15% declines for Italy and Spain after Brexit. Cough Cough. So what’s the remedy?

Acknowledge that scratch in the throat and take some precautions.

• Give yourself some R&R by lightening exposure

• Flush the system of laggards

• Wrap yourself in a blanket of puts, or cash

I’ll get to portfolio specifics in a moment. First, five notable hits from the Cowbell Chorus:

1. Defense Goes Offense

S&P 500 Index Sector Returns (6/30)

There are only two reasons to buy telecom and Utilities: Dividends and Safety. For these two groups to have appreciated over 20% in just six months tells me there is an incredible concern about the health of the broader market –understandably so. U.S. corporations will likely enter a fifth consecutive quarter of falling earnings when they begin reporting 2Q results next week. In addition, the S&P trades at 17.5x an estimated $120 eps for 2016, which assumes second half earnings do an abrupt about-face and rise 8-10%. I recognize #hopespringseternal but I have a hard time figuring out where the growth will come from, especially since the largest U.S. companies derive about two-thirds of revenue overseas. Let me share two further observations. First, the S&P Telecom Index may be up this year, but the long-term story is so uninspired it’s still 43% below the 2000 peak. Second, Utilities now trade at a higher multiple than Technology. Quite literally, this market is upside down.

2. Turtle Beats the Hare

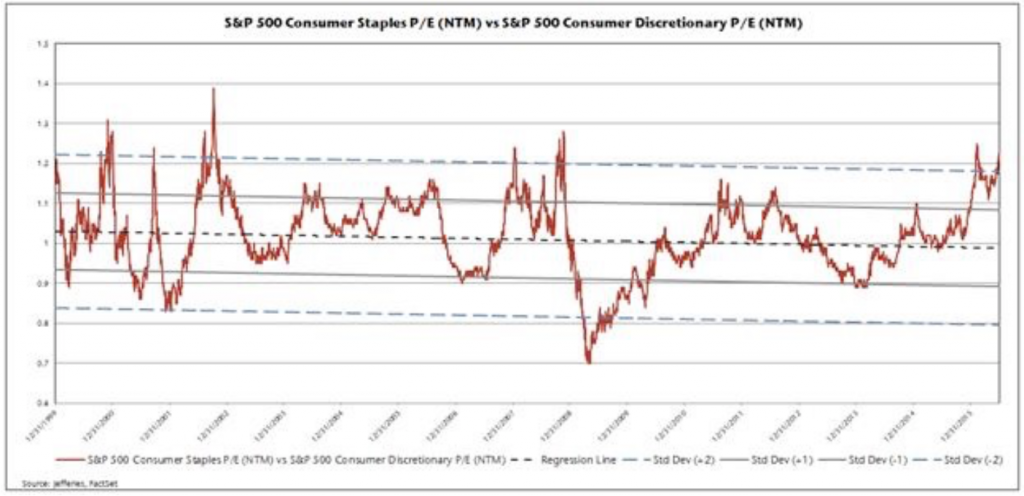

Staples vs Discretionary

I know this chart is hard to read, but I’m thankful to Jefferies for the perspective it provides and I urge you to take note. It compares defensive consumer staples to expansionary consumer discretionary stocks, specifically as a ratio of their forward Price to Earnings multiples (P/E NTM). When the ratio rises, staples are our performing. Currently, the ratio has risen about 2 standard deviations, which has happened less than 5% of the time since 1990. Here’s what Jefferies quantitative team wrote to clients:

Typically, six months after the spread widens to 1 standard deviation in favor of staples, staples have underperformed discretionary by 6% but in the six months since crossing 1 standard deviation, staples have actually outperformed by 6%, which is unprecedented and suggests to us some convergence in the multiples.

Their data indicates staples typically contract by 500 basis points relative to discretionary three months after one standard deviation moves… currently we’re above 2 standard deviations. In plain English, this means SELL. I provided a list of stapes to SHORT in the Bullseye report dated June 10, so I am definitely on board with this one. https://bullseyebrief.com/band-aids-beverages-bleach-issue-6-1/

3. Spare a Dime?

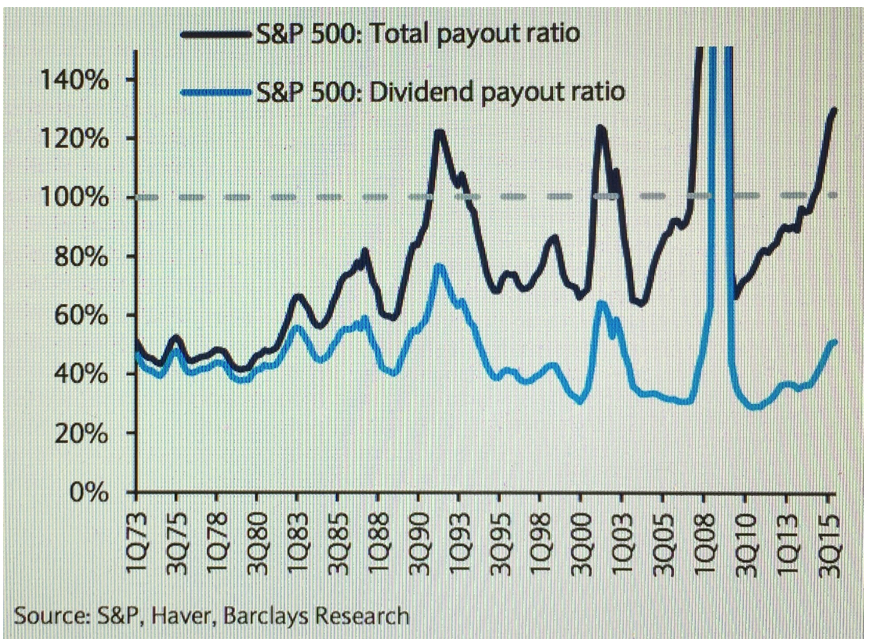

U.S. Corporations Borrowing to Pay Shareholders

Barclays Head of U.S. Equity Strategy Jonathan Glionna offers some particularly sobering data for the fiscally minded among us. In his mid-year note to clients, he concludes U.S. corporations are paying money to shareholders which they simply do not have. Specifically, he examined payout rations by sector, defined as the total amount companies pay in dividends and spend on buybacks expressed as a percentage of net income. Think of it as the amount a corporation effectively gives back to share holders. One is a cash payment, the other raises earnings per share by lowering share count. Both are generally deemed rewarding…generally. The problem in this case is a combined (total) payout ratio of 128%, meaning corporations are paying out more than they earn.

Barclays Head of U.S. Equity Strategy Jonathan Glionna offers some particularly sobering data for the fiscally minded among us. In his mid-year note to clients, he concludes U.S. corporations are paying money to shareholders which they simply do not have. Specifically, he examined payout rations by sector, defined as the total amount companies pay in dividends and spend on buybacks expressed as a percentage of net income. Think of it as the amount a corporation effectively gives back to share holders. One is a cash payment, the other raises earnings per share by lowering share count. Both are generally deemed rewarding…generally. The problem in this case is a combined (total) payout ratio of 128%, meaning corporations are paying out more than they earn.

Sometimes there’s a legitimate time lag, in that payouts during one period are funded by higher profits which accrue later due to accounts receivable balances or earnings offsets. For the most part however, payout ratios above 100% imply a drawdown of cash and/or funding through debt. What’s also troubling here, total payouts exceed 100% for all but three S&P 500 sectors (Technology, Financials and Energy). So the other seven groups are spending serious coin, coin they don’t have! As Mr. Glionna so keenly observes, buybacks reached an alltime high of $161B in the first quarter. In addition, companies with high total payouts historically have not appreciably outperformed the broader market, but merely kept pace. Borrowed money, borrowed time?

4. Heavy Metal

Ratio of Gold to Copper

Gold has been on a tear this year, and it’s not due to industrial demand or the fabled Indian Wedding season, which can create short-term seasonal spikes of 15%. Futures have risen from under $1,100/oz last December to $1,350 recently. I admit I have missed this move completely, but I have certainly not missed the staggering outperformance of gold relative to copper. Whereas demand for gold as a store of value has soared, its industrial cousin copper has languished, and the ratio between the two now stands at 6.11 (meaning one ounce of gold costs 6.11 times more than 100 pounds of copper). This nearly equates to the peak during 2009. The disparity within metals reveals a larger disparity within markets: Can the Dow Industrials maintain a near record high with industrial metal demand at a near record low? One position implies hope, the other implies fear and I do not believe two such critical assets classes can sustain polar opposite viewpoints indefinitely. The rubber bands are getting stretched, farther and farther.

Gold has been on a tear this year, and it’s not due to industrial demand or the fabled Indian Wedding season, which can create short-term seasonal spikes of 15%. Futures have risen from under $1,100/oz last December to $1,350 recently. I admit I have missed this move completely, but I have certainly not missed the staggering outperformance of gold relative to copper. Whereas demand for gold as a store of value has soared, its industrial cousin copper has languished, and the ratio between the two now stands at 6.11 (meaning one ounce of gold costs 6.11 times more than 100 pounds of copper). This nearly equates to the peak during 2009. The disparity within metals reveals a larger disparity within markets: Can the Dow Industrials maintain a near record high with industrial metal demand at a near record low? One position implies hope, the other implies fear and I do not believe two such critical assets classes can sustain polar opposite viewpoints indefinitely. The rubber bands are getting stretched, farther and farther.

5. Compression Depression

Bond Market Going Comatose

My final chart says it all: Bond traders have compressed yields so much they think Chair Yellen will raise rates only 2-3 times in the next five years. That is NOT indicative of a growing economy. Here’s the math: the Fed Funds rate is currently 30 basis points and 2-year yields are 0.41%, meaning there’s only about a 44% probability of a 25 basis point hike in the next two years ((41-30)/25). Yes, you read that correctly…the next two years.

Looking further out, traders have compressed the spread between 5yr notes and 2yr treasuries from 140 basis points two years ago to 59 basis points today, which implies they see just 2.4 rate increases of 25 basis points through 2021 (59/25). On the assumption the Fed would be forced to raise rates if inflation accelerated –even if it really, really wanted to stand by Europe– such a glum outlook suggest little growth in the offing.

Now I’m Depressed. Thanks Adam

It’s not that bad. We can still make money on the long side, we just have to be HIGHLY selective in what we buy. Recognize the markets are sending some very uncomfortable signals. By the same token, global central banks continue to work in unison back-stopping disaster (#Brexit, Italian bank capital infusions, Puerto Rican debt, Japanification, etc).

Here’s the game plan:

• Clearly identify the theme and catalyst behind every long (Growth, Value, Income)

• Avoid “indexed positions” like SPYs and QQQs

• Write call premium against long positions when implied volatility expands (generally 30 days or less)

• Buy puts on broader indices on big up days (60 days out with strikes down 2-3%)

• Increase exposure to shorts incrementally

• Pare exposure generally

Current longs include themes like Data Mining, Dividends and One-off Value Ideas.

Current shorts include Staples, and Hotels opportunistically.