Report Card

Winners, Losers & Lessons at Mid-Year

- THANK YOU for joining me as subscribers in my first quarter of business

- 15 of 21 recommendations (71%) have generated positive returns since inception

- Lower correlation within the S&P 500 Index creating opportunity to generate alpha

- Renewed coordination by central banks to reflate assets still the key obstacle for shorts

Bullseye Brief has successfully completed its first quarter in business. I am profoundly grateful for your encouragement, patronage and frequent attaboy messages of support. 15 of 21 ideas presented in these first months have produced positive results, meaning I have effectively “hit the target” 71% of the time. I’ve scored one Bullseye with the data mining companies profiled in my first issue, they are up 29%. I have also missed a couple of marks, notably the gravity-defying staples I am short. Overall, I’m learning there’s a rhythm to balancing research, writing and marketing. As one of our fellow Bullseye subscribers shared with me recently, the key to success is “patience and perseverance.” Great advice, and I thank each of you for your trust. -AJ

Bullseye Performance Attribution

Returns as of June 30, 2016

The so-called “Matrix stocks” have been on fire since my late February write-up, rising 29% or about three and a half times more the S&P 500 Index. These are the companies focused on helping businesses process and interpret reams of data generated by e-commerce, social media and the Internet of Things (IoT). Apigee (APIC) is a particular standout, having doubled from $6 to $12. The company derives its name from Application Programming Interfaces or API, hence Apigee. CEO Chet Kapoor explained to me in surprisingly plain English how APIs funnel facts/figures from company databases into simple spreadsheets so developers can create new apps. Data mining is evolving rapidly, moving quickly from Business Intelligence to Artificial Intelligence… i.e. from data interpretation to data prediction. This key theme will spawn more ideas in upcoming issues of Bullseye.

The so-called “Matrix stocks” have been on fire since my late February write-up, rising 29% or about three and a half times more the S&P 500 Index. These are the companies focused on helping businesses process and interpret reams of data generated by e-commerce, social media and the Internet of Things (IoT). Apigee (APIC) is a particular standout, having doubled from $6 to $12. The company derives its name from Application Programming Interfaces or API, hence Apigee. CEO Chet Kapoor explained to me in surprisingly plain English how APIs funnel facts/figures from company databases into simple spreadsheets so developers can create new apps. Data mining is evolving rapidly, moving quickly from Business Intelligence to Artificial Intelligence… i.e. from data interpretation to data prediction. This key theme will spawn more ideas in upcoming issues of Bullseye.

StealthGas (GASS) is my second best performer to date up 12.84% since late March. It is also MY SINGLE WORST MANAGED POSITION. The stock rallied from $3.35 to over $5 in two months and I did nothing to protect the gains. I could have written all of you to say “put a little something in your pocket here” or at least put a floating stop on the position. Instead I have watched if slip back into the 3s. Admittedly, the fundamental story is still intact: StealthGas trades at a fraction of Net Asset Value (NAV), controls 20% of the global market for smaller Liquified Petroleum Gas tankers (LPGs), and is making money even at historic low day rates. As a result, it is still a buy. But instead of having fresh capital from $5 sales to redeploy into $3 purchases, I’m already committed. Bottom line: I grade the thesis A-plus, my risk management C-minus.

StealthGas (GASS) is my second best performer to date up 12.84% since late March. It is also MY SINGLE WORST MANAGED POSITION. The stock rallied from $3.35 to over $5 in two months and I did nothing to protect the gains. I could have written all of you to say “put a little something in your pocket here” or at least put a floating stop on the position. Instead I have watched if slip back into the 3s. Admittedly, the fundamental story is still intact: StealthGas trades at a fraction of Net Asset Value (NAV), controls 20% of the global market for smaller Liquified Petroleum Gas tankers (LPGs), and is making money even at historic low day rates. As a result, it is still a buy. But instead of having fresh capital from $5 sales to redeploy into $3 purchases, I’m already committed. Bottom line: I grade the thesis A-plus, my risk management C-minus.

Consumer Staples continue to defy gravity. Many trade at earnings multiples of 30 times (nearly double the S&P 500 Index), in spite of low single digit earnings growth and dividend yields well under 2%. Predictability and yield were the entire thesis for long investors seeking safety and income. Now valuation has effectively rendered their appeal null and void… just don’t tell Mondelez. On June 30 it launched a bid for Hersey (HSY), which is one of the shorts on my list. Several have since popped 5-6%. Hershey has said, no thanks, as it did to both Nestle and Wm. Wrigley Jr. Co. back in 2002. Takeover bids aside, staples are relatively low volatility stocks historically, which partly explains why they’ve attracted safe haven investors since 2008.I would add to short positions, or at least by long-dated puts which represent a low cost way to position for an eventual return to earth.

Consumer Staples continue to defy gravity. Many trade at earnings multiples of 30 times (nearly double the S&P 500 Index), in spite of low single digit earnings growth and dividend yields well under 2%. Predictability and yield were the entire thesis for long investors seeking safety and income. Now valuation has effectively rendered their appeal null and void… just don’t tell Mondelez. On June 30 it launched a bid for Hersey (HSY), which is one of the shorts on my list. Several have since popped 5-6%. Hershey has said, no thanks, as it did to both Nestle and Wm. Wrigley Jr. Co. back in 2002. Takeover bids aside, staples are relatively low volatility stocks historically, which partly explains why they’ve attracted safe haven investors since 2008.I would add to short positions, or at least by long-dated puts which represent a low cost way to position for an eventual return to earth.

Good News

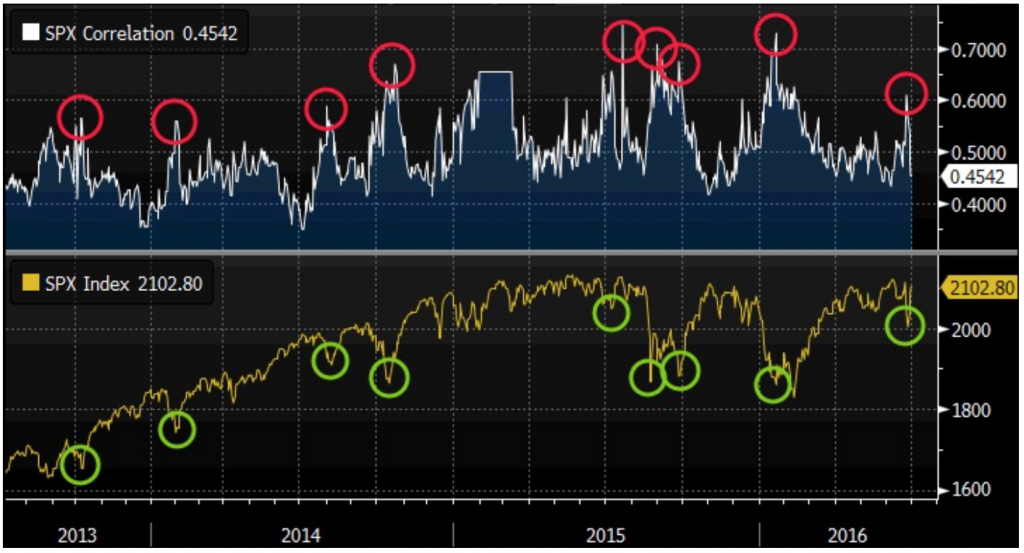

My recent piece “Chasing Alpha” identifies several metrics like Capex and Earnings Momentum as key drivers for second half returns. Specific themes and individual stocks matter more now as correlation within the S&P 500 Index has dropped to 0.45 (meaning the 500 components move the same general direction less than half the time.) This bodes well for active managers, and raises the stakes for all of us to “get it right.” It also bodes well for long-weighted portfolios. After spikes in correlation, as we experienced first hand during the Brexit scare when global assets sold-off in unison, markets tend to rally.

Correlation Spikes –> Buying Opportunities

I conclude my self-evaluation with an excerpt from a piece I originally wrote for the J.P. Morgan Chase website entitled, “Six Months an Entrepreneur, Six Lessons Learned.” Please email me if you’d like the complete article.

Happy summer, and again I say thank you.

* * *

I have been blessed in my first six months as a small business owner. Family has offered support, friends have opened doors, and clients have paid on time! In fact, it’s going much better than I could have expected, with one critical exception. Managing myself is the hardest thing I’ve ever done. EVER.

I’m not talking about work ethic. Long hours come naturally to me, as do enthusiasm, creativity and pitching new business. I’m talking about the soft stuff they fail to teach at B-school: Emotion. Dealing with my own mood swings has proven far more challenging than anything else on my to-do list. One week I find several new leads, even land a client. The next week, zilch. This must be how actors feel!

The fact is, life is about ups and downs. Whether we’re starting a business, auditioning for a role or raising a family, progress rarely follows a straight line. I have found in these first months the less I self-evaluate, the better. Like an investor who spends the day staring at flashing prices on a screen, one minute I’m a hero and the next I’m confused. So for everyone who thinks you’re only as good as your latest achievement, I say “No way.” Consider instead going for a run, spending time with friends or family and taking a break. Lesson #1: Soften Your Grip.