High Yield Now

Four Bond Funds Too Cheap to Ignore

- Implied default rates suggest 20% of energy/metals/mining companies will file Ch. 11

- Excessive pessimism has widened HY spreads to 800bps, exceeding recessionary norms

- Strong U.S. payrolls growth consistent with expansion not recession

- HY offers compelling deep value opportunity

Dr. Ethan Harris of Bank America Merrill Lynch is my kind of economist… pedigreed, top-ranked and totally normal. He once confessed to me in a commercial break at BloombergTV he found my co-anchor’s “multi-syllable words way too confusing.” Last month he told CNBC viewers worried about China to “take a deep breath and relax… they only buy 1 percent of our GDP… stuff over there doesn’t exactly say Made in America.”

Dr. Harris manages the global economic research team at BofAML, and since Institutional Investor has ranked him #1 multiple times, we pay particular attention when he changes his view. Recently, Ethan has raised his estimate for the probability of recession in the U.S. over the next 12 months to 20 percent, so did Ellen Zentner of Morgan Stanley.

While less alarming than the 40 percent probability cited the following day by Deutsche Bank economist Joe Lavaorgna, R-word anxiety has compressed the spread between 2-yr and 10-yr government bonds to the lowest in eight years. Long-term growth expectations have fallen so significantly, traders only demand an extra 113 basis points of return for 2026 compared to 2018. That’s the kind of malaise we witnessed in 2008! Sorry Ethan, but no wonder economics is dubbed the dismal science.

Bond Bummer

2-10 Spread U.S. Treasuries

Admittedly, we’ve seen The International Monetary Fund and World Bank lower growth forecasts repeatedly over the past twelve months, though their pronouncements are hardly recessionary. Each institution still sees global growth climbing 2.9 to 3.1 percent, with the U.S. likely averaging just above 2 percent. In fact, not one of the 71 strategists tracked by Bloomberg forecasts negative GDP in the next two quarters, traditionally the definition of a recession.

So by going against the grain, Messrs Harris and Lavorgna are either dead wrong, providing cover for themselves in case we do enter recession, or possibly they are just early.

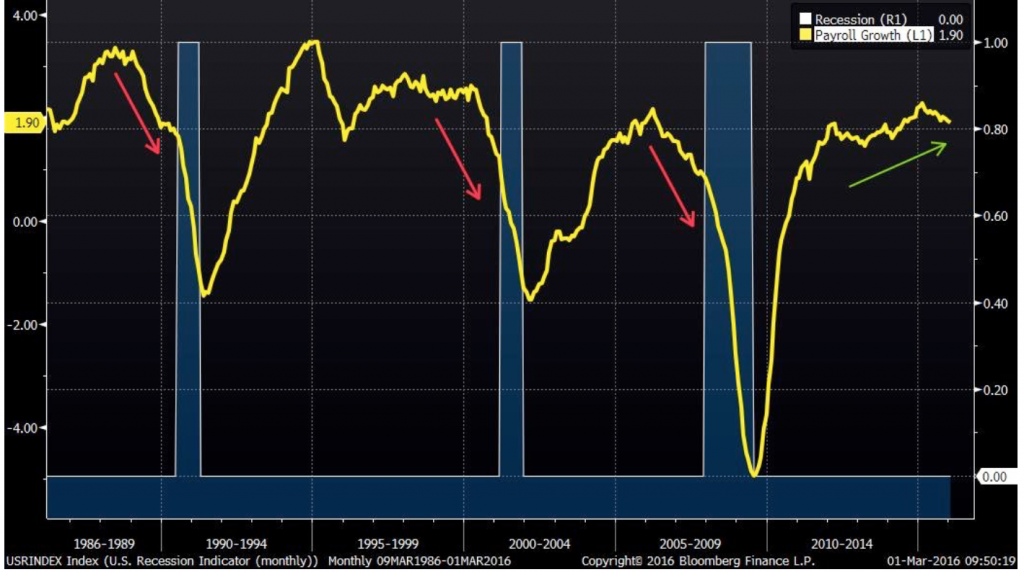

For clarity we turn to the labor market, which typically peaks 18-24 months ahead of recessionary downturns. We’ve charted the year-over-year change for monthly non-farm payrolls to illustrate the point. Recessions are identified by shaded areas. Severe labor downturns preceded all three recessions, which is not the case currently. January non-farm payrolls rose 1.90 percent, consistent with the 6-month average of 1.97 percent. If recession were in the offing later this year, we’d likely already have seen a steep decline in job growth.

No Downturn…No Recession

Non-Farm Payrolls Still Rising 2%

The National Federation of Independent Businesses provides additional comfort about continued labor market strength. It’s monthly survey of 1,400 geographically diverse firms across multiple industries indicates 29 percent of respondents have positions they are unable to fill, a six-month high. Additionally, 11 percent plan to hire additional workers within the next year, consistent with the 6-month moving average of 12%. If business owners are optimistic about hiring, in spite of having to pay 2.5 percent more in hourly wages per the January Jobs Report, we think investors should be more optimistic about the economy. Instead they are running scared.

This fear is most evident in the high yield market, where falling energy prices have gutted the energy sector and widened spreads across the board as if wholesale recession were a foregone conclusion.

Since the best outcome bond investors can expect is repayment in full and coupons along the way, they are notorious for fleeing a fire before there’s smoke. Strategas Research Head of U.S. Fixed Income Tom Tzitzouris explains:

“Defaults are rising and spreads should rise too, but the pace in Jan was a bit too fast for the rate of economic and credit decay. Above 700 basis points, high yield spreads signal a recession. Above 750 they are starting looking cheap. Current spreads at 777 imply a 6.25% default rate… high for a non-recession calendar year and almost 2% above longterm averages.”

Translation: The high yield debt market is oversold and should be bought.

And here’s the key…

Weakness in energy is skewing the entire high yield market. Energy accounts for just 16 percent of high yield issuance but could potentially account for 53 percent of total defaults this year, provided JPMorgan is accurate and one in five energy companies files Chapter 11. Add the related metals/mining sector and the number rises to 71% (J.P. Morgan Debt Monitor).

Never before have one-fifth of America’s energy, metals, and mining companies defaulted in the same year. JPM recently initiated this forecast to present a worst case scenario. In fact, it’s the only way to arrive at an overall HY default rate of 6 percent, since all other sectors will likely see the same sub-2 percent rate of the past several years.

To Tom’s point, spreads above 750 bps imply defaults above 6 percent, and 6 percent is only achievable if energy, metals and mining implode at rates never before witnessed. At these prices, buyers are being well compensated for the risk. We like high yield here.

So THANK YOU nervous bond investors for throwing away your perfectly good bonds. Your fear presents a value opportunity, and while we could certainly buy individual issues, we will opt instead for the diversification of exchange traded funds (ETFs) which invest in a basket of bonds from HY issuers.

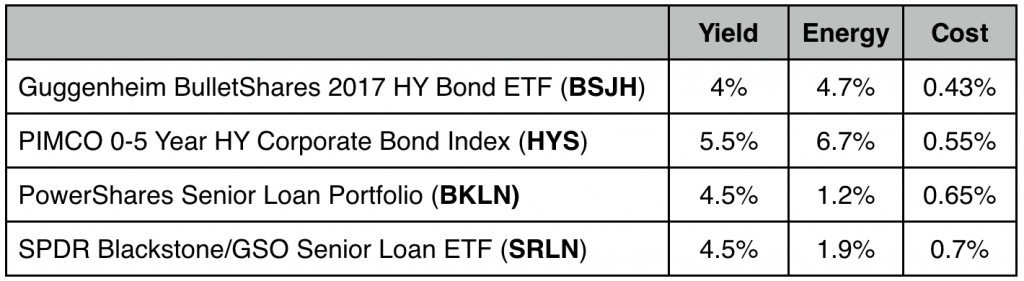

Bloomberg lists 33 high yield ETFs, including the two largest and most liquid: iShares HY Corporate Bond ETF (HYG) and SPDR Barclays NY Bond ETF (JNK). We will not consider these two however, as their energy exposure 9.5 and 10.9 percent respectively. Instead we focus on several others with lower exposure. They are all diversified, provide reasonable yield and meet minimum liquidity requirements. In addition they are down on average only 1-2 percent this year, implying reasonable safety compared to stocks.