Friends in Low Places

Eleven Deep Value E&Ps

- Many energy drillers trade at significant discounts to the value of their proven reserves

- Two-thirds of E&P companies still have at least half their credit lines available

- A select few have lower ratios of debt to cash flow than the S&P 500 Index average

- Production volumes lag price changes by six months, implying late summer rebound

U.S. energy assets are changing hands at cents on the dollar. The mid-May acquisition by Range Resources Corp (RRC) of Memorial Resource Development Corp. (MRD) for $4.4B represents a discount of nearly 75% off the current market value of the MRD’s 441MMboe of proven reserves at $45/bbl. Even applying realized oil and gas prices reported by MRD during Q1 of $30.10/bbl and $1.97/mcf respectively, this transaction still values MRD at less than half the value of its known reserves. NO WONDER this is the single largest acquisition by Range Resources in its history. Long-term strategic investors would be well served to emulate Range Resources CEO Jeff Ventura, accumulating shares in Exploration & Production companies with high quality assets and low levels of debt.

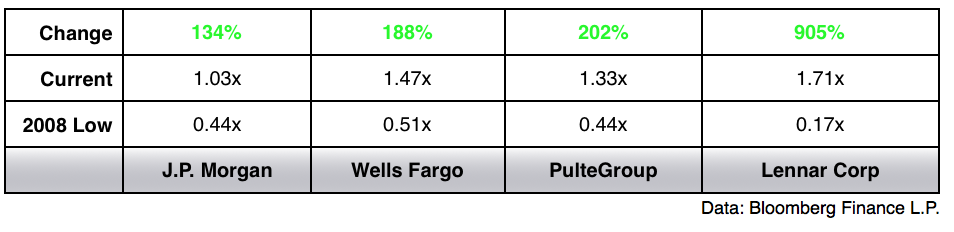

I knew energy assets were trading cheap, but I didn’t realize they were trading this cheap. Granted, relying solely on the value of hydrocarbons in the ground underestimates costs to both explore and extract, but I equate what’s happening in energy now to what happened to banks in 2008. Back then, JPMorgan traded down to 0.44x book… and you may recall CEO Jamie Dimon bought stock. So did then-CEO John Mack at Morgan Stanley, and Wells Fargo’s John Stumpf. Same story for the homebuilders. The environment was toxic and the outlook grim, but the assets got too cheap to ignore. Like Miami condos in 2010, Greek bonds in 2014, and energy companies today, low-priced assets with intrinsic value attract capital… and they rebound. Consider four examples.

Discounts Didn’t Last

Price to Book Ratios

Back to energy markets, the price paid by RRC for MRD speaks volumes, reflecting imploding metrics by nearly every measure:

• Active rigs searching for new oil and gas deposits have fallen 79% since 2014 (Baker Hughes)

• 3-yr average price declines of 50% have shut-in all but the lowest cost wells

• 63 U.S. energy companies have filed bankruptcy in 2016, a new Jan-May record

• Energy sector capital expenditures (CapEx) declined 36% in Q1 YoY (Strategas Research)

• $77B N. American energy corporates trade at less than 60 cents on the dollar (Morgan Stanley)

I had the distinct pleasure of joining legendary oilman Boone Pickens for dinner in early May with about three dozen investment managers and members of the media. Mr. Pickens is one of my all-time favorite television guests. I loved interviewing him because he’s funny, self-deprecating and razor smart. He commented at one point that “women run the oil business.” When asked to explain, he clarified that oil patch wives give their husbands about one week of “sitting on the couch with a six pack” after getting laid-off. Then the men are told in no uncertain terms to “Go get a job!” He says once they’re gone, they’re gone… wives won’t let ‘em go back to oil because it’s too unpredictable. Boone made the same point about drilling equipment, and he believes the current idling of land rigs and cold-stacking of offshore platforms will create a slingshot effect sending prices higher. Too much supply has come off market.

Put another way: The cure for low prices is low prices.

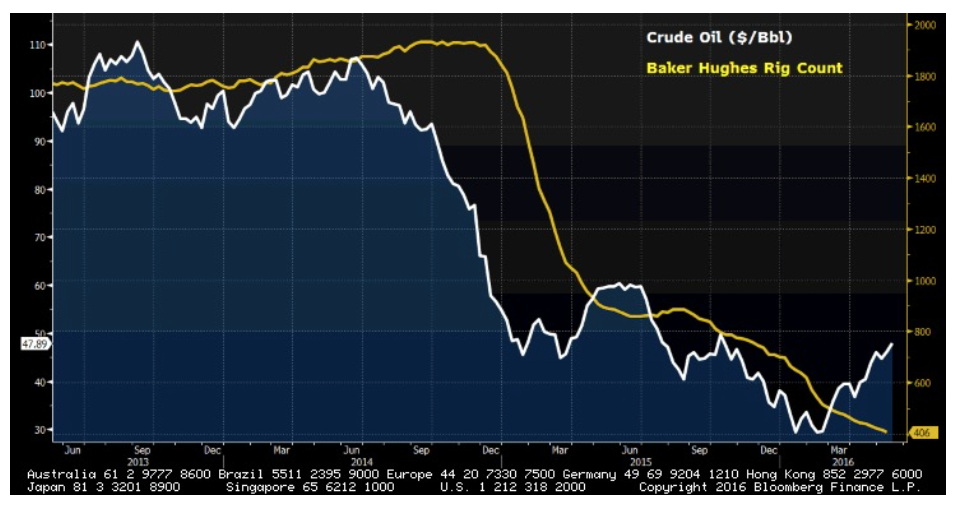

Over the past three years, oil prices have led rig activity by about 6 months, meaning price has moved first and then the equipment utilization has followed. Based on crude’s move from a low of $26 in February to the mid 40s now, we could expect to see drilling activity rebound by August if price gains are sustained. This is the corrective process Boone alluded to, and it’s bullish for energy E&P companies.

Cause & Effect

Production Follows Price

Curiously, not all E&P companies are as desperate as the headlines suggest. Bloomberg enables us to screen the universe of 106 drillers in the Russell 3000 Index to determine which companies have tapped into their credit lines based on figures reported as recently as Q1. The data is telling. Most of the companies which have tapped more than 90% of their credit lines have either filled Chapter 11 or are holding on for deal life, with stocks trading in the single digits. Some examples which come to mind include Triangle Petroleum Corp. (TPLM), W&T Offshore Inc (WTI), and Yuma Energy Inc (YUMA).

I implore you to resist the urge to contemplate stocks trading at $0.25. Many of these companies are tapped out and the stocks are just a marker for equity holders who hung on way too long. They are not cheap. They are worthless… their secured bonds may offer value but their equity does not. As evidence, recall former highflying SandRidge Energy (SDOCQ), which borrowed 98% of its credit line. The stock broke $1 a year ago and in mid-May went poof. Ditto for Breitburn Energy Partners (BBEP). In the past two weeks, Chesapeake Energy (CHK) has twice diluted equity investors by a total of 9.4% as it swaps old debt for new shares. I want no part of this action.

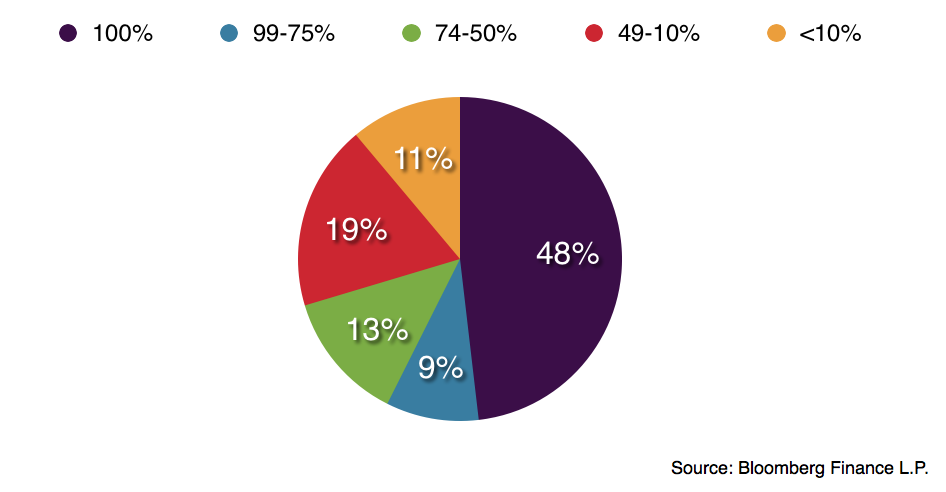

Instead, I’m focusing on well-capitalized companies which have barely tapped their credit lines, and there are more than you might suspect. Nearly two-thirds of the 106 companies we examined still had at least half of their credit lines available as of April 1, 2016. Almost half haven’t even touched them This is good. As we begin our process of narrowing down the few E&P companies we actually want to own, this is our starting point. We like tight-fisted drillers.

Tight Fisted

Credit Line Available

Having narrowed our universe of investable E&P candidates to the 76 which still have at least half their credit lines available, we focus on Low Debt, Low Valuation and High Survivability. Here’s our criteria more specifically:

• Total Debt is less than $7 per Barrel of Oil Equivalent (BOE)… manageable debt load

• Net Debt to cash flow (EBITDA) is less than 3.1x… ditto

• Enterprise Value (EV) to BOE Reserves is less than 0.9x… cheap, Cheap, CHEAP

• EBITDA for 2016 is at least half the amount during 2015… they’ve cut back but are still operating

• Strong analyst conviction… mostly buy ratings and only one, or no sells

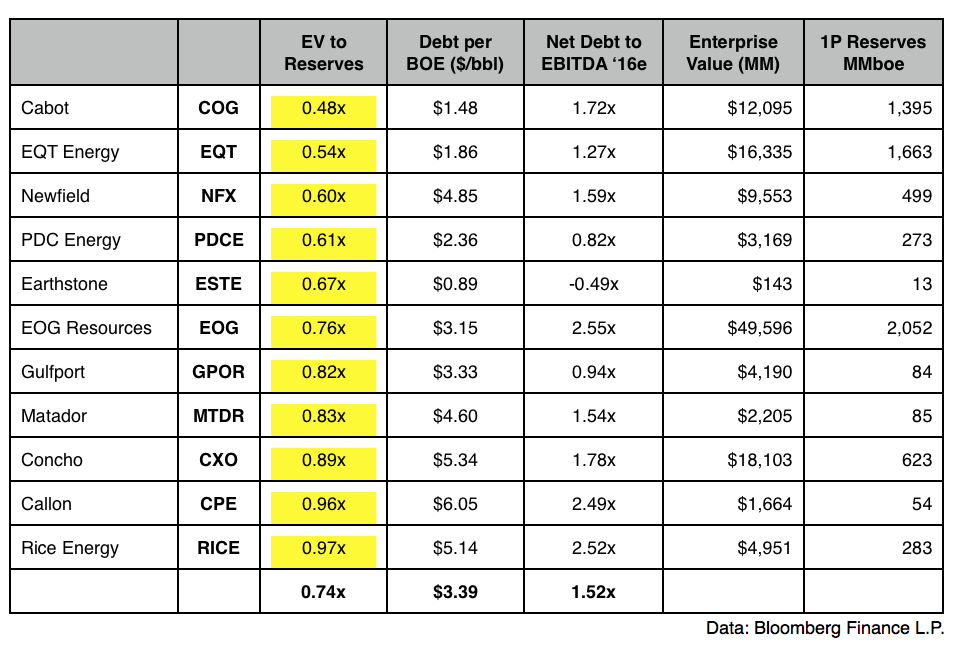

Eleven names from the original list of 106 made the list: Cabot Oil & Gas (CBT), Callon Petroluem (CPE), Concho Resources (CXO), Earthstone Energy (ESTE), EOG Resources (EOG), EQT Corp (EQT), Gulfport Energy (GPOR), Matador Resources (MTDR), Newfield Exploration (NFX), PDC Energy (PDC), Rice Energy (RICE).

In order to estimate the dollar value of proven reserves, I first multiplied barrels of oil equivalent (BOE) by $45 for producers with at least 50% production weighted to oil, and by $30 for “gassier” names. I then subtracted average lifting costs of $8.50/BOE and average transportation costs of $3/BOE. As a result, proven reserves reflect prices closer to actual realized prices, which is a more conservative way to estimate valuation. An even more rigorous analysis could itemize individual well-head costs and model depletion over time… but let’s not get too carried away.

A few important observations:

1. These companies are extremely cheap, trading at an average of 0.74 times the value of proven reserves. Banks and homebuilders traded at comparable valuations relative to book value in 2008, and have since risen by multiples.

2. Net debt to cashflow for the group equals 1.5x, which is LESS than the average of 2.2x for the S&P 500 Index. These companies are well-capitalized and in little danger of imploding. They are survivors, which is why many have not even tapped their credit lines. They don’t need to.

3. Both EOG and Concho made the cut, which is key. Nearly every energy analyst I interviewed at BloombergTV over several years told me these are the only two E&Ps which consistently fund new drilling projects from cash flow on existing wells. They are conservative, well-run and in-business for the long haul. Their inclusion on my list confirms the screening criteria is on point.

4. Barrels per Oil Equivalent (BOE) indicates the company’s audited and best estimate of proven reserves in the ground as of December 31, 2015. It includes both developed and undeveloped reserves. It does not include probable reserves, so actual reserves may be higher, and valuation cheaper.

Cheap, Low Debt & Lots of Oil

10 E&P Companies to Own