Bitcoin Grows Up

Five Blockchain Blockbusters

- Blockchain protocol pioneered to settle bitcoin transactions could transform money transfer

- Goldman Sachs, J.P. Morgan, IBM and Microsoft are investing in blockchain partnerships

- Citi Research identifies 20 businesses ripe for blockchain disruption

- Several consortiums threaten PayPal’s P2P franchise

CEO Bob Griefeld is a pretty cool cat. He’s the one who showed up next to Mark Zuckerberg for Facebook’s IPO wearing the spayed-on mock-T straight out of Star Trek, launched a first-ever public marketplace for private companies the following year, and is now bringing bitcoin back to life… sort of. This latest venture revolves around a revolutionary technology called blockchain, originally pioneered to settle bitcoin transactions. If you’ve never heard of it, suffice to say blockchain is capable of clearing trades in seconds versus days thanks to simultaneous reconciliation by all clearing parties which makes fraud virtually impossible. Mr Griefeld’s team is so excited by blockchain they mentioned it 45 times during a conference call with investors on March 31.

Star Trek and other moonshots aside, the promise of blockchain as a viable alternative to outdated clearing systems has convinced some of Wall Street’s largest banks to invest millions. In February, Goldman Sachs and IBM joined 13 other institutional investors to fund a privately held Digital Asset Holdings, a pioneer of blockchain technology. Per the joint press release:

“The addition of Goldman and IBM in Digital asset will continue to help drive the global adoption of this transformative technology… Blockchain holds real potential to transform a wide range of industries… improving efficiency while reducing cost, latency, errors, risk and capital requirements.”

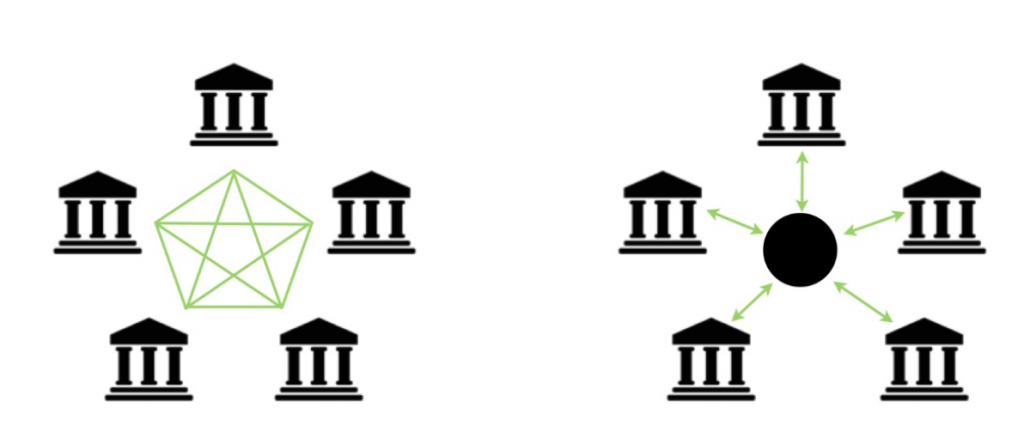

The key to blockchain is an innovation called distributed ledger, where all parties involved in a payment stream are aware of the transaction in realtime, and they attach their own unique security codes to effectively “solve” the clearing process. Rather than wait on each step in the daisy chain linearly, which can become problematic across time zones and with multiple currencies, each partner matches it’s own action with the anticipated entry on a shared ledger. Any discrepancies become immediately apparent, and settlement can occur much faster. Once a transaction has been verified across the network, the corresponding “block” of data is appended to the “chain” of previous transactions, hence the name.

More Points of Contact

Blockchain vs Central Clearing

One of the defining characteristics of blockchain is decentralization, another is trust. The notion of a distributed ledger, where all parties see all transactions, appears like an intentional abandonment of privacy. In fact, it’s more a reflection of transacting parties opting to communicate directly rather than through an empowered central clearing entity. Think open software like Linux or Android. That said, Morgan Stanley bank analyst Betsey Graseck, noted in recent research on blockchain that no policymakers she interviewed would endorse an “unpermissioned” distributed ledger.

So at this point, the consortiums pursuing the concept are doing so largely away from governmental eyes. Like Uber, they are disrupting a decades-old framework, largely absent regulatory input. The three most notable partnerships include the aforementioned Digital Asset Holdings, a second IBM-backed venture in conjunction with The Linux Foundation called The Hyperledger Project and R3, which is jointly funded by J.P.Morgan and Microsoft among 30 others (eg Barclays, Goldman Sachs, ING, Nomura, State Street).

While they sound like distinct entities and potential competitors, they are not. Like the open source software model on which development is based, collaboration is the name of the game. A recent article in Bitcoin Magazine notes, “The Linux foundation announced its Hyperledger project on December 17, 2015, and just one day later, 2,300 companies had requested to join. The second-largest open source foundation in the history of open source had only 450 inquiries.”

I recently attended a J.P. Morgan event for senior treasury executives of its largest corporate banking clients. The goal was to address the evolving landscape for wholesale payment processing and blockchain dominated the discussion. Lori Beer heads Technology for the Corporate and Investment Bank. She offered this perspective, which I paraphrase:

Through the use of a distributed ledger, blockchain technology allows a shared record of irrefutable events to be updated near-simultaneously across all parties to a transaction. It’s faster and more secure than previous protocols. The key is reducing friction wherever possible, increasing speed, visibility and security for our clients. Near-instantaneous transfer and settlement of funds across the bank’s global network expedites cross-border payments while minimizing traditional lifting fees and settlement inefficiencies.

Kristen Michaud, General Electric’s Managing Director of Treasury Operations also spoke at the event. She oversees 13,000 separate accounts and outlined two specific goals where blockchain could potentially play a role: 1. Raise the current threshold of payment automation from 30% to 90%; 2. Increase same-day settlement from 90% to 95%. Blockchain could transform multiple banking functions.

Blockchain as a Platform

Broader than Payments

There is even an experimental peer-to-peer energy exchange in Brooklyn which uses blockchain protocol to manage energy sharing.¹ A blockchain network links about a dozen homes, all of whom generate electricity on their roofs using solar panels. When one home needs to consume more than it produces, surplus is drawn from a neighbor and a shared ledger records the transaction. Because the network is highly localized, fewer “electrons” are lost during transmission and shared data in real-time optimizes excess supply. It’s efficient on two fronts.

Here’s the point: Blockchain could revolutionize transactional record keeping across multiple industries. The harder part is figuring out how to invest in blockchain and benefit from its potential adoption. While big banks have joined with Big Tech to sponsor VC-like blockchain startups, there are few publicly traded blockchain pure plays. There are however some derivative blockchain companies we are watching very closely, specifically with an eye towards accelerated blockchain activity which could prove the catalyst for dramatic future revenue growth.

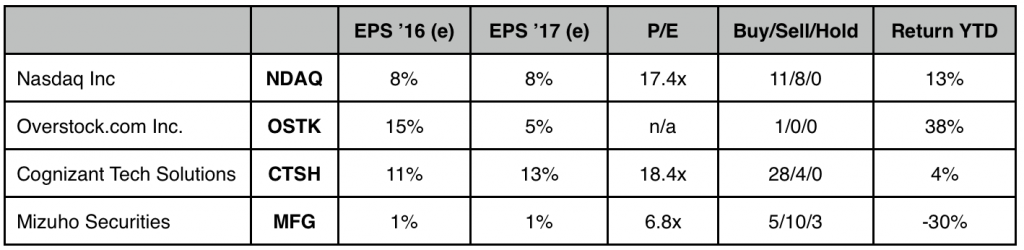

1. Nasdaq, Inc. (NDAQ) pioneered electronic trading in 1971. The company launched the first public marketplace for private companies in 2013, and now it’s actively piloting a blockchain program to settle some of its private company transactions. If a central exchange and clearing house built around innovation sees opportunity, pay attention. The integration of blockchain protocol onto its Marketplace platform is the most viable mainstream application to date.

2. Overstock.com Inc, (OSTK) has recently gained approval from the SEC to issue crypto securities which will settle according to the blockchain shared ledger protocol. While no issue date has yet been determined, the e-commerce company is effectively making itself a litmus test for blockchain as a real world settlement mechanism. If successful, the company may apply apply the method to peer-to-peer transactions (P2P). Overstock.com has launched a wholly-owned subsidiary called t0.com in order to “revolutionize the capital markets.”

3. Cognizant (CTSH) and Mizuho Securities (MFG) announced in February a strategic partnership to develop a blockchain solution for secure record-keeping of documents for all Mizuho Financial Group companies worldwide. This is really about expediting multi-party verification rather than trade processing. Per Cognizant Financial Services President Prasad Chintamaneni, “This paves the way for increased adoption of blockchain technology… into newer areas such as smart contracts and P2P transactions.”

4. The joint venture clearXchange as a future IPO? Similar to the 30-firm consortium R3, clearXchange includes several large banks and was founded in 2011 to present a viable P2P alternative to PayPal. Original backers include Bank of America, J.P. Morgan Chase and Wells Fargo. Capital One bought a 25% stake in 2014. The venture currently serves half the mobile banking customers in the U.S. according to Samsung Securities. While neither public nor purely blockchain-focused, it’s implicitly a shared ledger protocol given the scope of its user base. Most notably, transactions settle in two days virtually cost-free, compared to 6-8 days and 2.9% at PayPal.

¹http://bit.ly/1WQr2rB Bitcoin Magazine (4/25/16)