Is Anything Cheap?

10% Growth for 10x Earnings

- Only 8 companies in the S&P 1500 are growing at least 10% and trade less than 10x earnings

- All 8 have strong current franchises but face longer-term strategic uncertainty

- These are “story stocks” with unique fundamentals and adamant investors on both sides

- Half present attractive entry points from a technical perspective

On last week’s podcast I asked whether anything is still cheap. It’s certainly a worthwhile question as defensive sectors like Utilities and Telecom drive the S&P 500 Index to new highs, and global pension funds plough record billions into negative yielding sovereigns. Push me a little and I’ll say “No, nothing is cheap. Global central banks have penalized cash balances to ensure we deploy every cent of capital. We’ve bid up asset prices to the point of absurdity. NY condos go for $90M!” Okay, quantitative easing has made me cynical, but not oblivious to data, nor the power of the Bloomberg Terminal. Screening the S&P 1500 for growth and price, I did indeed uncover a handful of companies which are truly cheap –one even got acquired the day before publishing. Value does exist.

Bloomberg offers users a powerful screening function which narrows large groups of securities into specific baskets based on quantitative search criteria. While my goal was to identify stocks I thought were cheap, I also wanted to consider growth forecasts and gauge sell-side support. In other words, I wanted stocks which are cheap but probably deserve to trade higher, both because they are growing and the analysts love them. Starting with the S&P 1500, I applied the following metrics:

- Forward 12-month price to earnings ratio less than 10x

- 2016 earnings growth of at least +10% (Q1 and Q2 actuals plus Q3 and Q4 estimates)

- 2017 earnings growth forecast of at least +10%

- Analyst buys outnumber sells plus neutrals

- No more than one sell allowed

- Minimum 20% upside to target based on consensus estimates

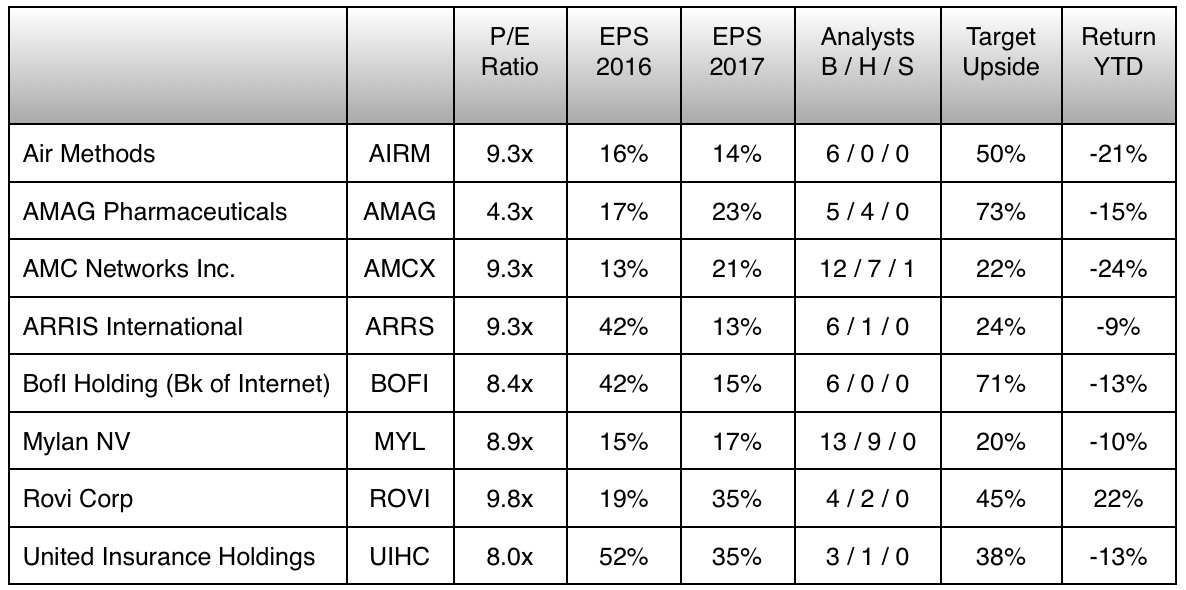

Cheap & Growing

Only 8 of 1500 Meet Criteria

Stocks are generally cheap for a reason, and a forward P/E of less than ten in an environment when the S&P 500 Index trades at 18.5x implies something is awry. Yet each of these companies is growing and is well-admired by the analysts covering them. Hence the potential opportunity for us. While my discussion is primarily fundamental, note some of these charts. They look ready to bounce. Happy hunting.

Air Methods Corporation (AIRM)

Air Methods provides emergency airlift services across North America. If you’re a stranded hiker in Death Valley and need a emergency helicopter, or a transplant patient in Atlanta awaiting a donated organ from LA, these guys are probably involved. They serve hospitals on a contract basis with 500 aircraft (mostly helicopters) from 229 bases across the U.S. They also operate emergency call centers, and about 11% of revenues come from using idle helicopters for tourism in certain locales. At an average of $12k per flight, medical cost scrutiny under the Affordable Health Care Act has weighed on shares. In addition, the tourism business slipped 1.6% YoY in the recent quarter and may obscure the core business. That said, margins have risen each of the past 3 years and the company is buying back stock.

AMAG Pharmaceuticals Inc (AMAG)

AMAG looks down and out, but it’s not. The concern stems from upcoming patent expirations for its two lead drugs: Makena which delays prenatal births and Feraheme which treats iron deficiency for patients with kidney disease. Each drug is involved in studies which could potentially broaden approved applications and extend patent protection. Makena requires injections that can create adverse side effect, so AMAG is pioneering alternative administrations which could earn seven years of protection under orphan drug status. In the case of Feraheme, the company is engaged in a trial of 20,000 people with iron deficiency unrelated the current kidney disease application. Results will become available next year and could potentially provide new applications for the drug by 2018. As with most biotechs, the outcomes are binary and analysts are split between targets ranging from $27 to $80. The stock currently trades at $24, which suggests risk-reward favors the longs.

AMC Networks Inc (AMCX)

What makes AMC interesting is its ability to consistently produce exceptional hits like Mad Men, Breaking Bad and The Walking Dead. That is also the challenge however… Can they do it again? So far, the Walking Dead spin-offs have done quite well. Better Call Saul attracted 3.2 million viewers per episode in the first season and Fear the Walking Dead 7.2M. By comparison, Mad Men attracted just 2.1M per episode in its first season. Distribution accounts for 56% of revenue, and advertising constitutes the balance of 44%. Strong penetration across digital platforms is a positive, as is the international exposure provided by the 2014 acquisition of Chellomedia, but again you’re betting on hits here.

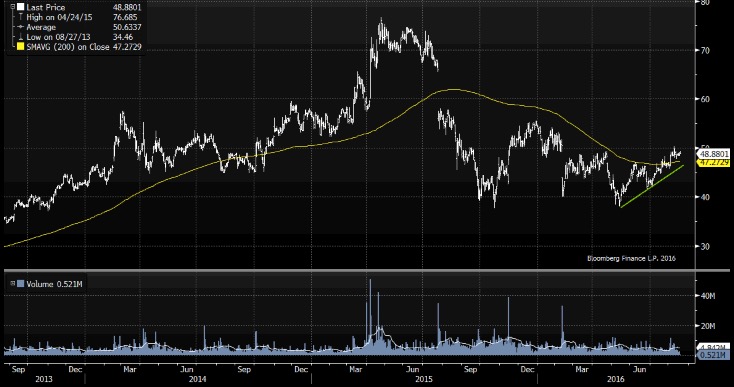

ARRIS International plc (ARRS)

Okay, this is a crazy chart and I’m not crazy about it. A lot of gaps, and right now it looks like it’s levitating, which suggests it’s vulnerable short-term. That said, this company is the global leader in set-top box and video infrastructure equipment. Do you watch TV or stream content online? ARRIS makes it possible. The company currently controls 45% of the home broadband market in the U.S. according to IHS. There are two issues for potential buyers: 1. Whether this dominant share is as good as it gets 2. Whether mobile supplants fixed box distribution over time, and if so how ARRIS will adapt. These hypotheticals are hard to answer. Right now the company is sitting on nearly a billion in cash and posting strong growth. It’s also quite cheap at 9.3x earnings and 0.7x sales.

Bofl Holding, Inc (BOFI)

This is a hairy dog. A staggering 44% of BofI’s stock is sold short based on a lawsuit filed last October by former a employee which alleges multiple improprieties (inflated appraisals, loan doc forgery, insufficient due diligence, etc). That said, all six analysts covering the company maintain their buy ratings as the bank continues to post double digit asset growth and strong earnings. In the most recent quarter, assets rose 30.5% YoY to $7.6B, net interest margins held at 3.7% and ROE for the 12 months ended June 30 was 19.43%. The partnership with H&R Block to cross sell IRAs is moving forward. CEO Greg Garrabrants addressed the current litigation on the most recent earnings call, “The bank is in strong regulatory standing with no enforcement actions, has not been fined a single dollar by any regulatory agency, has not been required to modify its products or business practices. Additionally, we do not foresee any further impact to the underlying business as a result of the frivolous lawsuit and the short-seller thesis. Our management team and employees remain focused on running the business.”

Mylan NV (MYL)

David Einhorn’s Greenlight Capital doubled its position in Mylan during 2Q to 4.9M shares (14 of the top 25 shareholders increased positions during the quarter, 9 sold and 2 held steady). I like seeing a value minded activist investor increase his stake in a company, especially in Mylan’s case as it has never recovered from the gap created last year when Teva abandoned its hostile takeover bid. 86% of Mylan’s business is generic, which means margins are lower and upside is less than non-generic drug makers. In addition, there’s no dividend. Of the 8 companies in my screen results, this is probably the least compelling –though 8.9x earnings for mid-teens growth seems awfully cheap.

Rovi Corporation (ROVI)

Rovi is like TV Guide for the 21st century. It creates interactive programming guides for cable companies and video ad campaigns appearing on digital devices. The company is currently in the process of acquiring TiVo and the deal is on track to close by Oct. 1. In addition, George Soros bought 3.6M shares during 2Q to become the seventh largest shareholder. As for why it trades so cheap, the 2017 earnings estimate of $2.30 is LESS than the 2011 earnings of $2.40. Also of note, the company has missed estimates seven times since… that’s nearly two years worth of disappointments. As noted earlier, stocks are generally cheap for a reason, or in this case seven reasons.

United Insurance Holdings (UIHC)

Take a bow United Insurance! I ran the screen on Wednesday night and Thursday morning it announced a merger of equals with RDX Holdings. The stock popped 9%. If only every trade were this easy! This underscores the value of running regular stock screens for growing companies trading at a discount. If we don’t buy them, someone else will.