Thank You Uncle Sam

How to Maximize your 401(k)

- Compounding and dividend reinvestment significantly enhance 401(k) returns

- Outperform after-tax accounts nearly two-fold over long-term holding periods

- Second quintile dividend stocks offer the best risk-adjusted returns

- Six stocks to buy now

American illustrator J.M. Flagg created his iconic image of Uncle Sam for Army recruiting posters in 1917. He effectively painted himself wearing a top hat and borrowed the nickname from a legendary U.S. Army meat supplier from the Battle of 1812, whom troops affectionately called “Uncle Sam” for stamping US on bags of rations. Today pork has replaced steak as Washington’s meal of choice, but there’s still one particular feast every American deserves: tax-deferred compounding and 100% dividend reinvestment in a 401(k) account.

Congress first introduced language on tax deferred savings plans into the Internal Revenue Service Code in 1978, though in true governmental fashion the IRS took another three years to codify treatment and structure for what would become commonly known as 401(k) accounts. By 1983, seven million Americans were on board. Today the number has risen to 55 million and assets top $4.5 trillion, according to the Investment Company Institute.

Now, let’s be clear: 55 million people may sound like a lot, but it’s less than one-third of the working population. Far too many people are ignoring Uncle Sam’s generosity… note the pointed finger. This is red meat for the masses, and everyone has a seat at the table.

401(k) accounts represent the single most advantageous retirement plan available and we should all be participating. Here’s why and how to maximize returns.

For the 2015 tax year, individuals can contribute up to $17,500 of pre-tax income. In addition, companies can make matching contributions, provided the combined total does not exceed $53,000. All earnings which accrue in a 401(k) are tax deferred, meaning no tax is paid until withdrawal, presumably after retirement and therefore at lower rates. Since earnings include interest, dividends, and capital gains, 401(k) returns significantly outperform identical allocations in after-tax accounts. In effect, the government is giving you a loan on all your gains, allowing you to compound the government’s money in the process. Again, this is a very good deal.

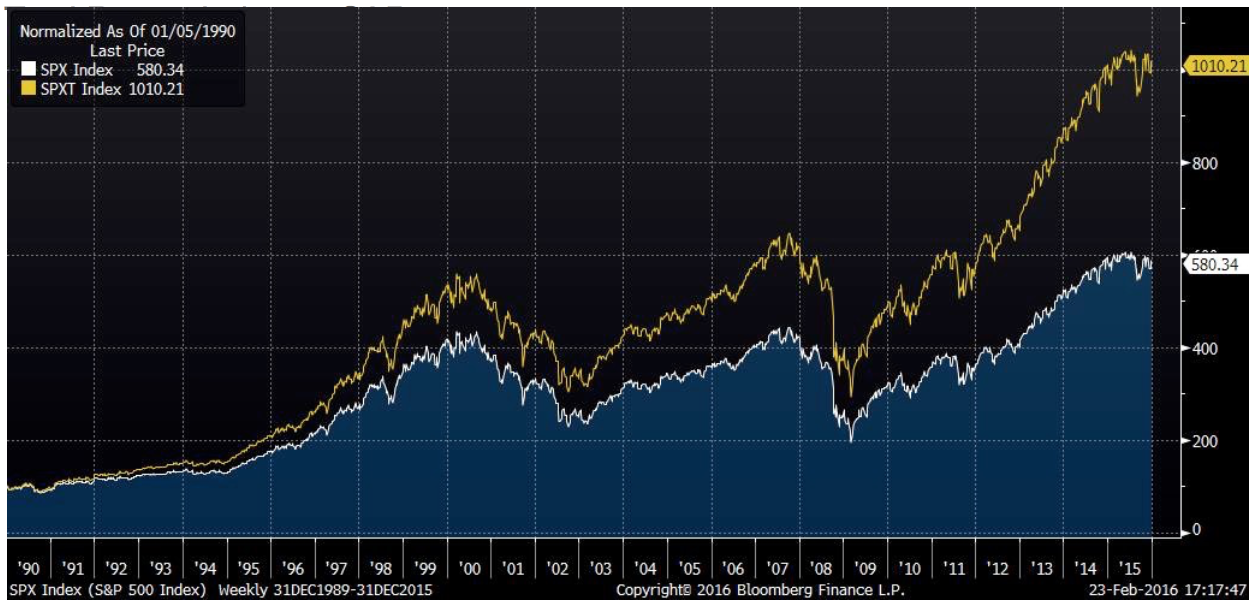

To better illustrate the point, consider returns on the S&P 500 Index relative to its Total Return Index, where dividends are reinvested without regards to tax withholding. This is analogous to a 401(k) account. Every time a company in the index pays a dividend, the amount automatically goes towards purchasing additional shares. The Total Return Index assumes taxes and commissions are zero.

Reinvesting Dividends Adds Up

Total Return Index vs S&P 500

The difference is staggering when seen on the chart above. While an initial investment of $100 in the S&P 500 Index at the beginning of 1990 rose to $580 by 2015, the Total Return Index (TRI) rose an additional 430 percent to $1,010. The reason for the near doubling of performance is twofold: additional shares accumulated over time generate additional return; no taxes are paid on dividend distributions, so more money buys more shares.

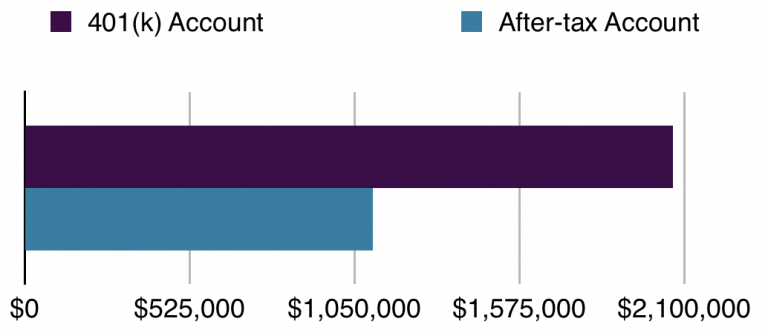

Let’s put some real world numbers on this to further prove the point, focusing on the actual 25 year period from 1990 to 2015. We will be very conservative in our assumptions: a.) an individual’s company does not match employee contributions; b.) the IRS maintains its current maximum of $17,500 rather than adjusting upwards for cost of living.

Our base case reflects the actual return of the S&P 500 Index over the 25 year period, including dividend income, but not allowing for any dividend reinvestment. In our 401(k) account by contrast, those same dividends accrue tax-free and are fully reinvested. Plugging actual returns of 8.5 percent and 11.4 percent respectively using Bloomberg data, 401(k) outperformance is self-evident.

Power of Pre-Tax Compounding

S&P 500 Returns (1990-2015)

The key here is compounding over time. The same S&P 500 stocks in a 401(k) account produced nearly double the return of 25 years. For all the talk (and effort) to find the next Uber or Apple, buying boring dividend-paying names and reinvesting the proceeds on a tax-deferred basis is a highly profitable strategy.

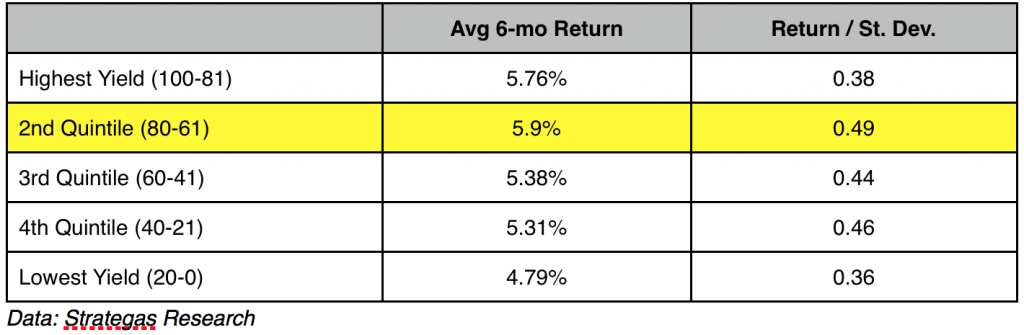

Now that we’ve got the basics, the question is whether we can further optimize returns through stock selection, and the answer may be yes. The team at Strategas Research looked at the risk-adjusted returns of S&P 500 component stocks sorted by dividend yield. They found risk and reward were maximized when investors bought the second decile of highest yielding stocks (i.e. stocks ranked 61-80% in terms of yield) and rebalanced every 6 months. As their data illustrates, the second quintile produced the highest returns on both an absolute and risk-adjusted basis.

Second Quintile Steals First Place

S&P 500 Index by Dividend Yield (1990-2015)

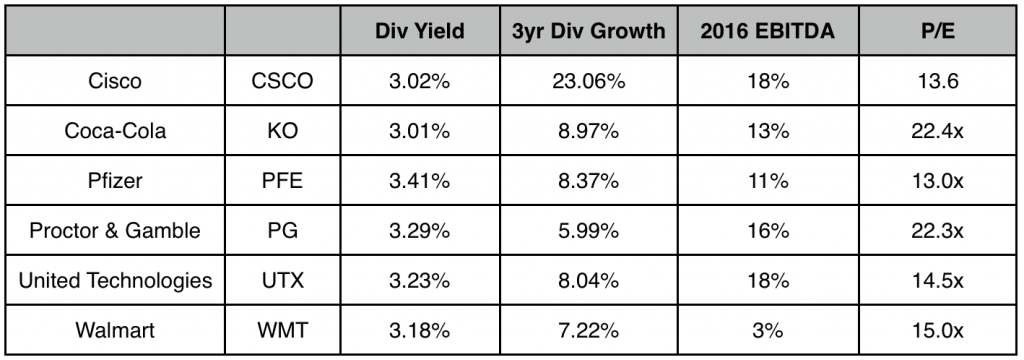

We are all about maximizing returns, but not at the expense of our sanity. Even in a world of zero commissions, the prospect of buying/rebalancing/reinvesting dividends on over 100 stocks is totally impractical. So as an alternative, we applied the Strategas second quintile approach to the more manageable Dow Jones Industrial Average. The index has just 30 components, all of which pay dividends, so the second quintile totals just six companies.

Backtesting the strategy with Bloomberg Analytics over the maximum period allowable (2000-2015) shows the DJIA second quintile group outperformed the overall DJIA Index by a margin of three to one, returning a cumulative 151% compared to 52%. Additionally, since Bloomberg Analytics can only model dividends paid plus stock appreciation on backward-looking time series, not dividend reinvestment, we would expect actual returns to be higher.

DJIA Second Quintile Dividend Portfolio

As of 12/30/15

For investors looking to replicate our study, or begin putting it to work in their own 401(k) accounts, here’s our methodology:

• Buy the second quintile dividend components of the DJIA as of 12/31.

• Rebalance as of 6/30, and every 6 months thereafter.

• Immediately buy new shares with proceeds from dividend distributions.

• Our study revealed 51% turnover annually, meaning three stocks were typically bought/sold every 6 months.