Smokey the Banker

Nine Stocks with 10% Growth at 10x Cash Flow

- Central bank balance sheets still 3-6 times pre-2008 levels… and rising

- Recent actions by BoJ and ECB exacerbate deflation

- Financial debris piling up creates incendiary conditions

- Protect capital in proven Growth at Reasonable Price (GARP) strategy

Quail plantations cover south Georgia’s pine barrens for miles. Hours pass as you make your way through sage brush and red clay, steering your horse around pines taller than the sky. It’s an lyrical place and I found myself transported. Strangely though, something our huntsman said about annual shrub burns in March led my mind back to the canyons of Wall Street and rip tides of Washington. Allow me to explain.

Longleaf pine forests overhead and grasslands afoot sustain native quail populations which once stretched from Virginia to Florida, as far east as Texas. They survived for centuries through diversity and resilience. In addition to providing habitat for up to 300 separate plant species and 60 percent of the region’s amphibians and reptiles, their seeds could withstand the heat of regularly occurring forest fires, sometimes only sprouting because of heat. These boom/bust cycles occurred regularly, clearing the forest floor from debris and providing ample opportunity for plants to regenerate… ultimately creating more suitable habitat for quail and other wildlife.

Today this ecosystem covers just three million acres across the southeast, down from an estimated 90 million acres before settlers began arriving 300 years ago (The Smithsonian). In addition, a stated “zero tolerance” policy against forest fires by U.S. Forestry Service mascot Smokey the Bear means forests don’t purge themselves naturally, creating an unnatural build up of dead wood which has contributed to a 19 percent increase in fire season length over the past 35 years (Nature Communications study, July 2015).

As we rode across fields where nature still rules, I was stunned by the now fire-free example presented by global asset markets. Central bankers want no part of cyclical downturns. Fire is something they now seek to avoid at all costs. Their artificial buying has contorted rates into negative territory past the point of recognition. Smokey the Bear meets Janet Yellen. Zero tolerance meet Zero Rates. Again, I digress.

Georgia’s plantation owners are working overtime to rebalance and replace these vast forests, often partnering with local institutions like Auburn’s School of Forestry & Wildlife Sciences and the Tall Pines Conservancy. As my guides explained, the process begins in March and April, when forestry wardens grant permits to conduct controlled burns on private land. Fire eliminates dead wood, consumes oak saplings which starve ground plants of light and produces heat which open spores and seeds. Within weeks, green shoots emerge.

By the second season, a canopy of broom sage hovers four feet above soil no longer scorched by fire, teeming instead with insects. It’s the perfect environment for quail to move in and begin brooding. They are shielded from hawks circling above, while surrounded with ample food for their chicks on the ground. As July arrives the birds will begin exploring corn and sorghum patches farther afield, feeding on an abundance of seed from newly sprouted crops. Come November, they’ll circle fields in coveys of up to 30, relying on one another to fend off predators. Many will survive for several years, though a few will get paired with bacon, as was the case on our particular weekend.

My time in Georgia revealed the modern quail plantation is about restoring as faithfully as possible the natural lifecycle. Full-time staff with forestry degrees serve as caretakers of the land, facilitating blossoms and burns… booms and busts. Their six to ten thousand acre parcels attempt to duplicate what happened for centuries before the advent of roads, homes and businesses. If only the Fed could shift its annual policy conference from the rivers of Jackson Hole to the pine groves of south Georgia…

To the Fed’s credit, it stepped into the abyss of 2009 when banks and private institutions ceased to function. The Fed provided a bid as the lender of last resort and prevented a full-scale meltdown. But as former Dallas Fed President Richard Fisher offered on CNBC mid-January, “We at the Fed brought demand forward by several years by keeping rates so low for so long.” Put another way: We prevented the burn, and now it’s a tinder box.

Like Smokey the Bear, they’ve made clear no fires are allowed… controlled or otherwise. In the words of ECB President Mario Draghi, “Whatever it takes.” He’s not alone. In January, Bank of Japan governor Haruhiko Kuroda lowered the rate paid on excess reserves posted by banks at the BoJ to negative -0.1 percent. Not only is Mr. Kuroda disallowing the removal of debris from the forest floor, he’s imposing a penalty if anyone picks it up.

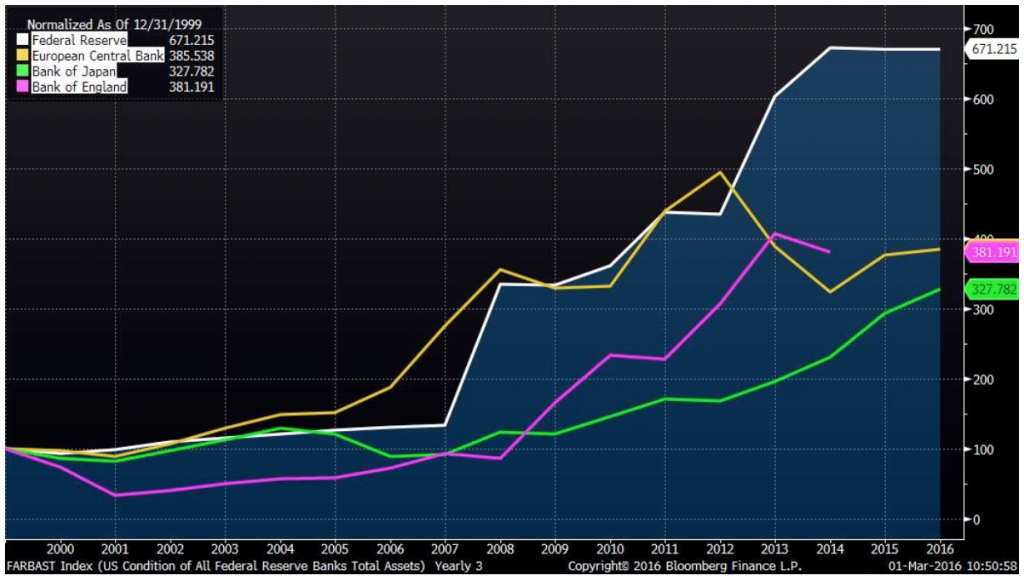

The logical consequence of increased debris is a much hotter fire, and we may well be stacking the wood past the danger point. Assets held by the four largest central banks outside China (BoE, BoJ, ECB, Fed) have risen fourfold on average since 2000.

Debt Pile

Central Bank Asset Growth

Another recent policy adjustment proves troubling. On January 27, The Federal Reserve released its latest outlook and chose to include some new wording about “monitoring markets.” Smokey, put down the binoculars. The Fed already has a dual mandate, assigned by Congress in the Reform Act of 1977, which states explicitly “the goals of maximum employment, stable prices, and moderate long-term interest rates.” Adding this market-facing mission only increases the Fed’s already interventionist bias. Again, no chance of a natural burn on Chair Yellen’s watch.

One final thought about fires and barking dogs: they wake us up. When a fire erupted inside the walls of my Georgia host’s home months earlier, he was alerted by an otherwise calm labrador retriever. The dog growled at the walls, barked until he was heard and wouldn’t leave until the children were out.

China’s 48 percent implosion since May is our barking dog. For six years we have laid comfortably in our beds as Zero Interest Rate Policy (ZIRP) by the world’s central banks have pushed otherwise responsible investors into inappropriate assets father afield. No longer. The current correction reflects a reassessment of risk by global asset managers. Where the bankers failed to clear the floor of debris, asset managers are now pruning proactively, and they’re not done cutting. The limbs have gotten long, and S&P 500 Index offers little value at 17 times earnings, specially given four consecutive quarterly earnings declines.

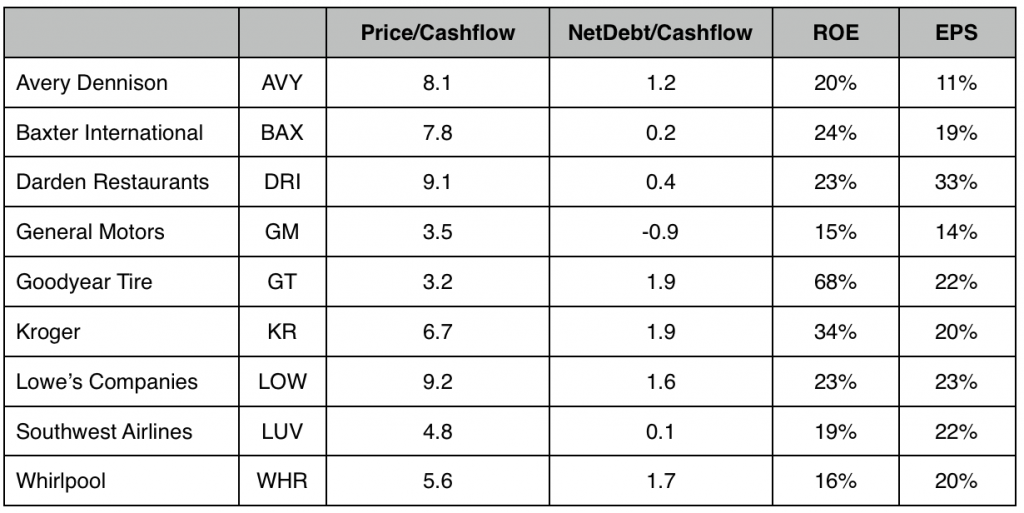

As a result we need to find a brush-free clearing for our assets, as well as some blue sky overhead. We turn to our friend David Herro of Harris Associates, named Fund Manager of the Decade by Morningstar in 2010. David is soft-spoken, thoughtful and precise. His stock selection process begins with a timetested screen he runs periodically to identify growing companies with little debt, trading on the cheap:

• Price to cash flow less than 10 times

• Net Debt to cash flow less than 2 times

• Return on Equity (3-yr avg) at least 13.5 percent

89 companies in the S&P 500 Index meet David’s criteria, and as he notes, stock screens are a place to begin, not an end unto themselves.

To narrow the list, we added two more conditions: Projected earnings growth in 2016 of at least 10 percent and positive earnings revisions during the past 60 days. Eight names fall off the list, proving the combination of 10 percent growth at less than 10 times cash flow is difficult to find. As fire risk rises around us, these are the types of places where we intend to seek refuge for a portion of our assets.