Hammer the Competition

One Semiconductor’s Quest to Dominate

- NXP Semiconductors ranks #1 by sales in its two largest markets

- Top 10 largest shareholders add to positions in Q4

- Key executive reiterates Freescale merger synergies

- CFO to update profitability and growth metrics April 28

“We don’t want to be just number one in the market, we want to be number one and at least 50% bigger than the next guy in the business.”

Strong words indeed, and we admit they catch our attention. We don’t often hear executives raise the bar quite so high, especially in the beleaguered semiconductor industry. Intense competition has compressed operating margins, and research firm IDC estimates growth in 2016 will barley touch 3 percent.

But don’t bother telling Peter Kelly, Exec Vice-President of M&A at NXP Semiconductors NV (NXPI). He’s the man who made the comment at Morgan Stanley’s Tech Media & Telecom Conference in early March. He is also the executive charged with integrating NXP’s recent acquisition of Freescale Semiconductor. The companies merged in December and now control over half the market for secure smart chips used in the auto industry. In that rapidly growing niche, where NXP’s chips work with sensors to enable park assist, automatic braking and lane change alerts, no one else even comes close. NXP also ranks #1 globally in programmable smart chips used on credit cards and inside smartphones to power secure money transfer apps like ApplePay (9.5% of sales). Samsung is also a customer, accounting for 5.5% of sales.

Together, NXP’s dominant auto and consumer franchises account over half annual revenue, estimated at $9.5B for 2016 as the company integrates its Freescale acquisition. This transaction catapults NXP squarely into the middle of the S&P 500 Index, comparable to Mastercard (MA), Lennar (LEN) and Tyco International (TYC).

Still haven’t heard of NXP? You will, and the company is making sure. Nearly the same day Mr. Kelly made his case to attendees the Morgan Stanley TMT conference, several positive developments hit the tape:

• NEC Corp. (6701 JT) names NXP Semiconductors Partner of the Year

• Harman (HAR) teams with NXP to enable vehicle-to-vehicle communication (V2X)

• NXP introduces remotely programmable smart cards which can serve multiple apps

• Drexel Hamilton initiates NXP as a Buy with $102 target (+30% upside)

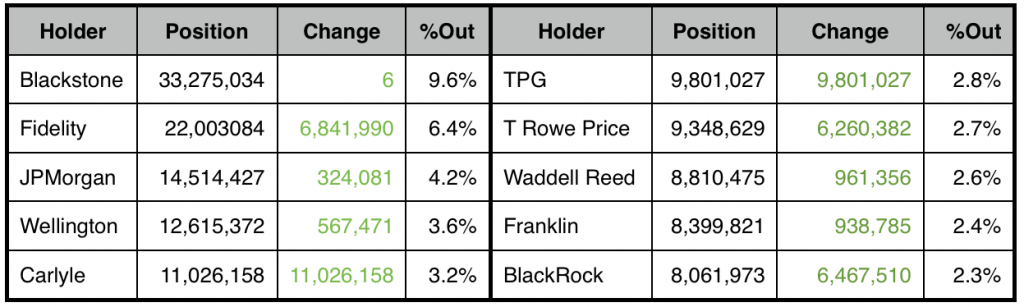

Wall Street got the whisper ahead of the news, of course. Top ten shareholders all bought shares during Q4 –lots of shares– and critically they are strong-handed buyers with very deep pockets… a CFO’s dream.

Big Names…Big Buyers

Position Change 4Q15

Institutional investors of this caliber buy large blocks because they have vetted the story ad nauseam. Their analysts have inserted themselves into the supply chain and modeled future cash flows. Their portfolio managers have argued multiple opportunities around the table and settled on a select few. Ten thorough investors reaching the same conclusion at the same time speaks volumes.

CATALYST #1: the NXP/Freescale combination creates runway.

First, the combined company will control over 15% of the $26B market for secure, specialized chips used by the auto industry. Second, this market is growing three times faster than the overall semiconductor market according to IDC, 9% versus 3%. Third, the sensor/secure chip architecture in hybrids and driver-assist technologies has significantly higher margins than traditional logic chips, in some cases by a factor of four. Fourth, these smart vehicles require double the number of chips, a total of $200 per vehicle. Fifth, added scale fosters long-term partnerships with key suppliers, providing added earnings visibility for NXP investors.

In addition to reiterating $500M in merger synergies (20% gross margin expansion and 80% cost savings) Mr. Kelly shared the following with attendees at the Morgan Stanley event:

“As soon as we announced the deal, the big OEMs were all over us straight away. They just see this as hugely positive. For them, they’re making a big investment in you as a partner. They know they have to work with you as a partner for 10-15 years. They are delighted to have a big company to work with.”

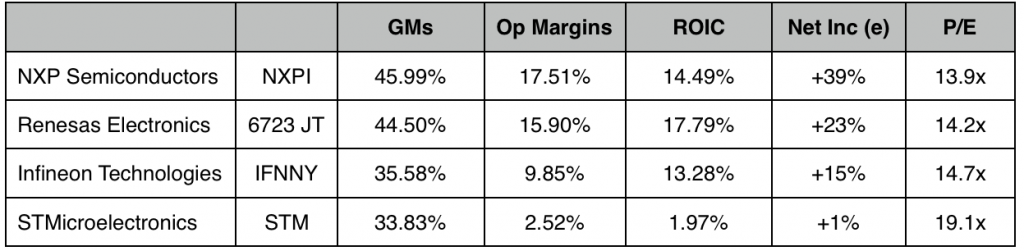

We will likely hear more from Mr. Kelly on April 28 at the company’s first analyst day since the merger. He told us to expect detail from CFO Dan Durn as to “what our growth targets are, what our gross margin targets are, what our operating margins are… and more importantly how we get there.” We will eagerly await those details. Meanwhile here are some of the figures currently forecast by the Street, including NXP’s closest competitors for both auto and mobile segments (60% of pro-forma sales for 2016):

Key Metrics Beat Key Competitors

Trailing Twelve Months

CATALYST #2: Rising demand for NXP’s secure smart chips which drive e-commerce on mobile devices.

While mergers grab headlines, STX has an equally compelling opportunity to expand its near-field communication chip business (NFC) on mobile devices through major agreements with Apple, Samsung and Xiaomi.

NXP creates secure chips in smartphones which enable tap-to-pay transactions, think Starbucks lattes with a tap of your phone at the checkout counter. This mobile division was equal in size to Auto prior to the Freescale merger ($1.3B annual revs), and is growing even faster at 13%. The deal with ApplePay accounts for nearly a tenth of NXP revenues, and a recently announced expansion with Xiaomi further enables public transit payments throughout China.

Essentially, these are the next gen chips which first appeared on credit cards in the 1990s as a secure alternative to magnetic strips. That transition solved fraud issues, and now internalizing payment within the phone increases flexibility. Since the phone is connected, chips can be updated remotely, unlike chip enabled cards which have to be replaced. Related applications like electronic passports present additional upside.

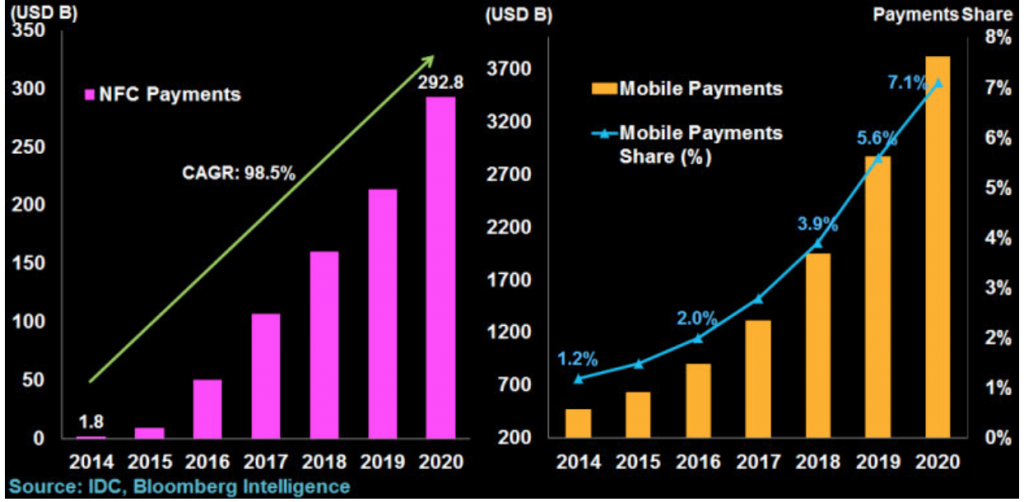

In the case of Xiaomi’s new transit app, the goal is to transition 400M users of disposable transit cards to tap-to-pay technology. It’s just one of 108 NXP customers identified by Bloomberg. Based on company filings, Bloomberg Intelligence quantifies such near-field communication (NFC) opportunities as a potential 98.5% CAGR market through 2020, which would still put mobile payments at just 7.1% of total.

Positioning for Growth

Tap-to-Pay Upside

25 analysts cover NXP, 23 of whom rate it a Buy. Collectively, they forecast 35% upside over the next 12 months (average target $104). We agree with their estimation, and we believe 13.6 times earnings is far too cheap given the glide path.