The Last Shall Be First

21 Shorts to Avoid

- Hard-to-borrow shorts outperform broad market nearly three to one in February

- Nearly 10% of large and mid-cap stocks nearing hard-to-borrow threshold

- Short Interest as a percentage of float hits a post-crisis high

- Heavily shorted stocks up significantly YTD

The Head of Block Trading had lost seven figures in several minutes. He was desperate, in disbelief and almost inhuman as he hovered in place, staring into his screen. We were new to the desk, new to Wall Street and totally petrified. All we wanted to do was get out of his way. Hundreds of traders and the room had gone silent. “I’m am getting my face RIPPED OFF.” And then it got worse.

Short squeezes are highly unpleasant. You watch prices accelerate and realize the only way to make the pain go away is to buy. Every purchase is higher, and then you begin to think everyone knows. You’re not paranoid of course, just convinced you’ve been ratted out and now everyone’s ganging up on you… squeeeeezing.

To the uninitiated, selling borrowed shares on the assumption you’ll buy them back later at a lower price probably sounds slightly twisted. In fact, it’s quite common. Like our Head of Trading who was simply taking the other side of a customer’s purchase and rounding out a large order, going short is a part of every day market making. For a portfolio manager with net long exposure, shorting rebalances the overall risk profile towards neutral. In theory it reduces risk.

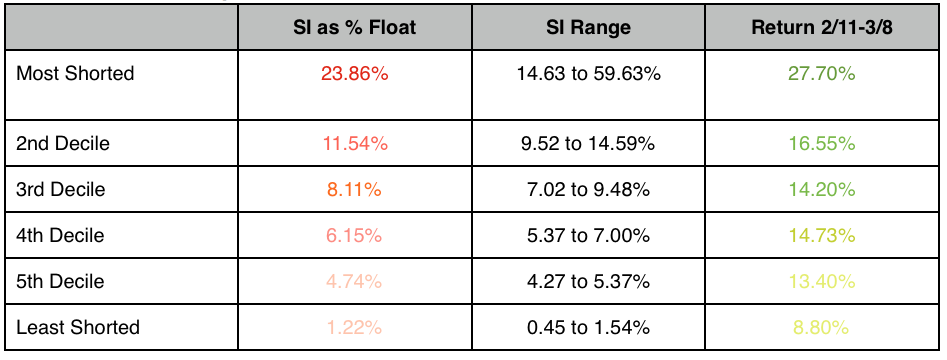

We say “in theory” because shorts have taken investors for quite a ride recently. The top 10 percent MOST shorted stocks in the S&P 1500 Index rallied 27.70% from the February low through early March, nearly three times the rise of the broader market. Meanwhile, the least shorted stocks –which by default we could call the least hated stocks–lagged the market and rallied just 8.80%. Strange times indeed.

Most Pain…Most Gain

S&P 1500 sorted by Short Interest

This action is incredibly significant. So-called “rip your face off rallies” are common in heavily shorted stocks which have been placed on the Hard to Borrow List, but rare for such a large group of stocks simultaneously. The extreme price move perfectly illustrates the concept of why crowded trades are best avoided, unless of course you’ve identified the imbalance in advance and taken the other side. Again, look at the data above and focus on the top row. The most heavily shorted, most hated stocks in America rose 27.70% in one month.

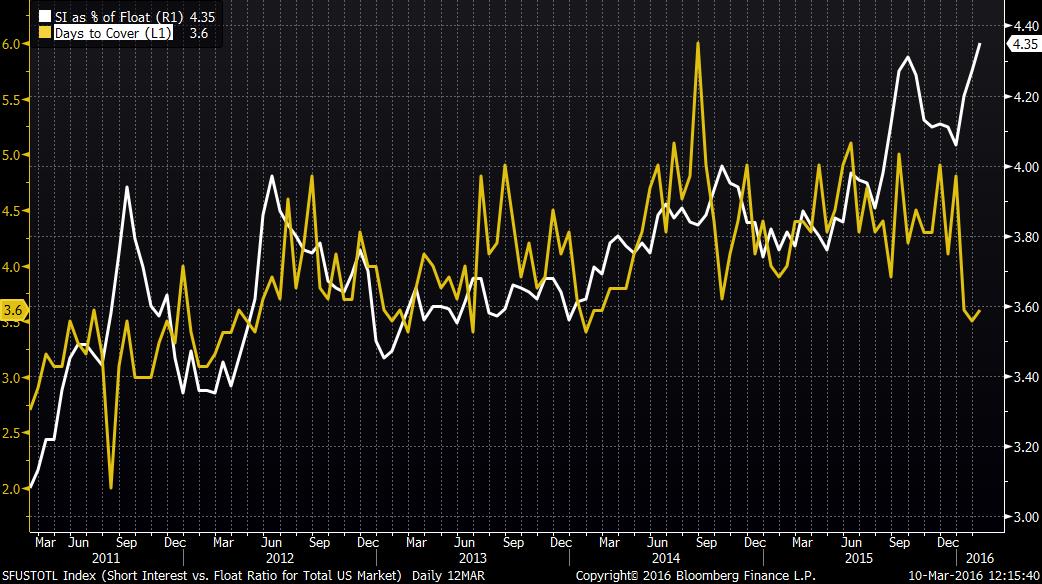

What’s happening here? First of all, recognize shorts as an asset class are on the rise. The bull market has entered its 84th month, well above the average run of 59 months for post WWII bull markets, and The Fed has begun turning off the spigot of excess liquidity, in spite of GDP growth which still lags the +3% target. Additionally, the S&P 500 Index trades at approximately 16.5 times forward earnings, towards the higher end of the historic 14-17x sweet spot. So you can understand why portfolio managers are eager for ballast against their longs. Two primary measures of short activity have increased steadily since the financials crisis:

1. Short Interest as a Percentage of Float Divide number of shares shorted by total shares freely trading in the market to express the level of short activity in relative terms. Currently 4.35%, this ratio is the highest since 2008, having bottomed in 2011 at 3.11%. That’s an increase of 40% in five years (white line below).

2. Short Interest Ratio, or Days to Cover Divide short interest by average daily trading volume to determine how many days of typical activity are required to eliminate the overall short position. Note: recent declines reflects 15-20% higher daily trading volume, not lower gross short activity.

Shorts on the Rise

SI as % Float hits 5yr High

So we have a general backdrop where shorting is on the rise, opening the door to sudden updrafts which create artificial rallies and obscure fundamentals. 88 of the 900 largest public companies traded in the U.S. have SI to Float ratios at or above the hard-to-borrow threshold. Investors MUST consider the short landscape for a given stock before initiating a position, even if they are going long.

From my days as an options trader calling Bear Stearns’ Stock Loan Desk in search of stock to short against customer buy writes, the general Rule of Thumb is any SI/Float Ratio above 11% equals Danger Zone. If 11% or more of the float is shorted, then the stock by definition is Hard to Borrow and subject to buy-ins by margin clerks who must balance accounts by end of business. If back office clerks are in there buying and you are short, you have a GIANT problem. They will keep buying until the position is covered. They will not ask questions and they do not care. They are they gorilla baggage handlers from the old Samsonite commercials.

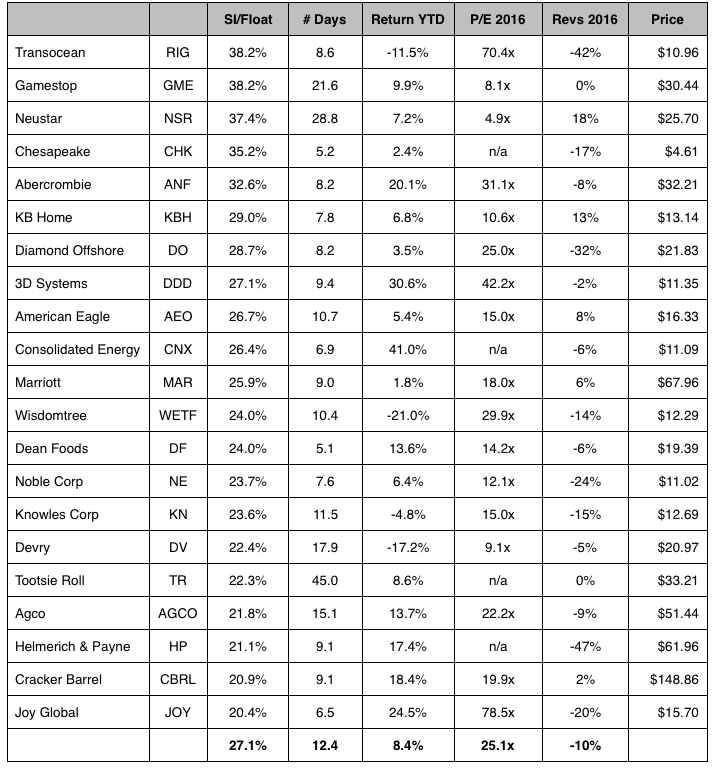

In the interest of avoiding said beasts, we’ve established some basic ground rules and complied a list of stocks which we will absolutely not short. First, resist shorting a stock priced under $10 and NEVER under $5. At that point you’ve already missed it and they’ll rip it in your face. Chesapeake Energy (CHK) comes to mind as a recent example. Second, avoid small caps in general. They are less liquid and harder to borrow. More fertile ground exists elsewhere. Third, steer clear of stocks which trade fewer than 100k shares per day. They are too unpredictable.

Now let’s screen for large and mid-sized companies which look squeezable. We choose our words carefully here because 1. We will definitely not short them 2. We might even buy them opportunistically if we smell smoke (see paragraph one). Our list includes stocks in the S&P 500 and 400 Indicies whose short interest as a percentage of float exceeds 20%, and where five or more days would be required to cover all outstanding short positions. We also present sales data to help explain why shorting is elevated (sales are generally falling while P/E is high) and returns YTD to show why crowded shorts are dangerous (stocks are generally up).

What to NOT to Short

Values as of March 10, 2016