Anchors Aweigh

One Fleet to Own Now

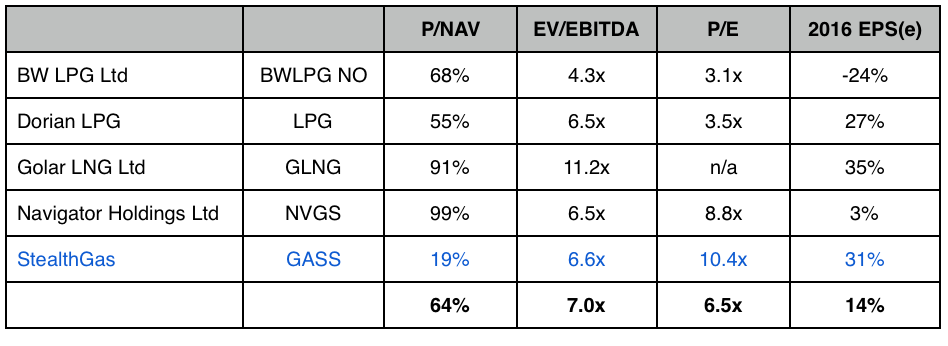

- High quality shipping assets are trading at significant discounts to net asset value (NAV)

- China LPG imports up sixfold since 2008 are forecast to rise again in 2016/7

- Niche operators earning profits now are highly levered to potential rate increases

- Maritime stock valuations tracking commodity prices will recalibrate to shipping volumes

We’ve just identified the Perfect Storm, and we like what we see. StealthGas is a Greekbased operator small-sized tankers transporting Liquified Petroleum Gas (LPG). It embodies everything investors have been desperately trying to avoid for the past 12-18 months: Uncertainty in Greece; Price Implosion in Energy; Oversupply in Shipping. So why are we intrigued? Price. The stock trades at a fraction of net asset value. In addition, it has lots of cash, very little debt, a new fleet with dominant market share. One more point: It’s making money even now, at the lowest shipping rates in decades.

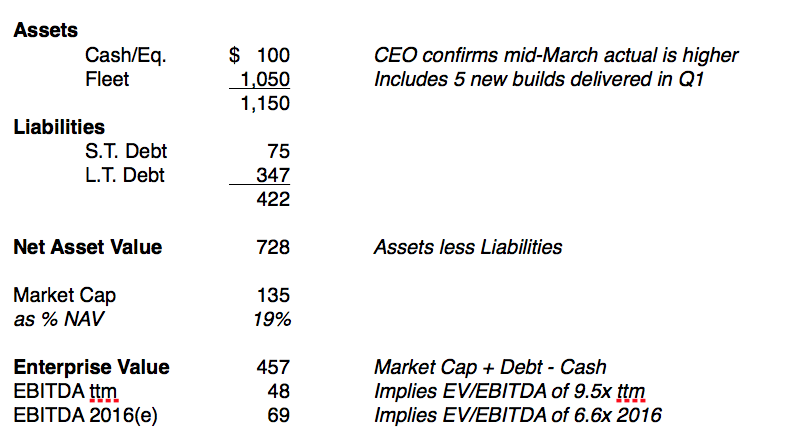

StealthGas is a balance sheet story with a cash flow cushion. Assets comprise cash of $100M and a fleet valued at $1.05B. Its 53 ultra-high quality, Japanese-made LPG carriers have an average age of 8.8 years. The fleet is almost fully booked, operating at 93% of capacity, and last year the company generated nearly $50M in EBITDA. Liabilities as of 12/31 totaled $455M, including $75M short-term debt and $347M long-term debt. Debt is privately held by international lenders in the form of loans at an average of +200bp over LIBOR for terms of 7-15 years. Leverage (net debt to assets) is 35%, half the industry average and likely to decline through 2018 as the company retires a portion of its current loans. Bottom line, StealthGas owns high quality assets funded with low comparative levels of debt.

Compelling Value

Key Metrics as of 12/31 (millions)

We interviewed CEO Harry Vafias mid-March at the NASDAQ market site. To say he is exasperated by the current price is an understatement. While he concedes all shipping stocks have suffered with oil prices, especially StealthGas as a Greek domiciled enterprise, he thinks the discount is extreme. “Let me stress how cheap our stock is, how strong our balance sheet is. We have very little debt and lots of cash. We are trading at less than a quarter of NAV. Someone should buy us.”

Let’s indulge that last comment for a moment and imagine that someone should be us. Current enterprise value is $457M, which includes equity and debt less cash. Assuming we paid a 20% premium to equity holders as a sort kiss to the Gods (this is a Greek company, after all) our total purchase price would rise to $484M. In return, we’d be getting 53 virtually new ships worth $1.05B and generating an estimated $69M in cashflow this year. At this point we could either:

a. Net $251M by liquidating the company, which entails selling the fleet at say a 30% discount to market value and then netting proceeds against the purchase price (1.05*0.70 – 484 = $251M) to generate a Return on Equity of 52% (251 / 484)

b. Earn $25M annually by privatizing StealthGas in an LBO, financed by putting up a portion of the fleet as collateral and using cash flow to support debt payments. If we apply the same 30% haircut to the fleet’s market value, we’d need to post roughly 2/3 of the fleet as collateral against the purchase price (484 * 1.3 = $629M). If this were financed with debt at 7%, debt service would total $44M (629 * 0.07), which is easily covered by 2016 estimated cashflow of $69M. Pretax operating profit would be $25M (69 – 44).

To check our math and get a second opinion, we spoke with Jefferies’ I.I. ranked shipping analyst Doug Mavrinac. For starters, he rates the stock a buy with a $7 price target, suggesting it’s 50% undervalued at current prices. He shared several other key perspectives. First, he notes StealthGas is making money at the bottom of the rates cycle, which should provide considerable operating leverage if rates begin to rise. In fact, Mr. Vafias told us a sustained increase of $1,000 in the current day rate of $7,000 would add $20M to cashflow this year. Second, Doug argues maritime shipping stocks should trade on the volumes of the materials they transport, NOT the prices of those materials… and volumes are up.

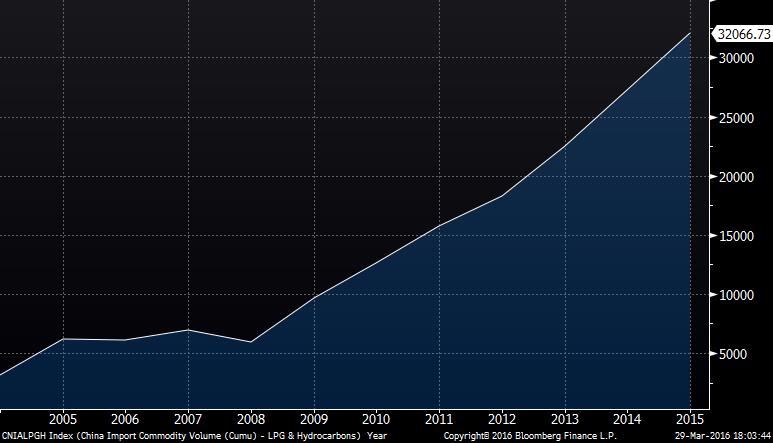

Liquified petroleum gas (LPG) shipments from the Mideast to China have been rising steadily. This is where two-thirds of StealthGas vessels are booked on term charter, and why the company enjoys a 93% operating rate. Since 2008, China’s imports have increased sixfold, as rising household wealth has enabled more Chinese to purchase cooktops and stoves. Globally, Doug forecasts global LPG trade will grow 15-16% in 2016 and 10-11% in 2017. This is very good for StealthGas.

China Driving Demand for Tonnage

Imports of LPG + Hydrocarbons (000 tons)

Critically, StealthGas operates vessels in the smallest class of LPG carriers (3,000-8,000 cubic meters). This is a distinguishing advantage over competitors, whose larger vessels cannot access the many smaller ports which supply secondary and tertiary Asian markets. Additionally, with fewer smaller vessels on the water currently and fewer new build deliveries expected in 2016 (11% vs 39% overall) smaller vessel day rates are significantly less volatile than those for larger vessels. Doug believes this combination of fundamentals creates divergences within shipping asset classes and positions StealthGas as the one to own.

Ultimately, the maritime shipping industry is fairly easy to understand. Operators fund vessel purchases with debt, servicing coupon payments with cash flow earned from transporting material with predictable regularity. Eventually, bonds come due and vessels are either recapitalized or sold. Proceeds fund purchases of new vessels and the cycle recommences. The opportunity in StealthGas currently is equally straightforward: A stock valuation at 19% of net asset value is simply too cheap for a market share leader whose vessels are nearly fully booked, generating ample cash flow to service low levels of debt and produce profits for shareholders.

StealthGas: Too Cheap to Ignore

March 2016 (Bloomberg data)