Home From Siberia

13 Banks to Buy Now

- The KBW Bank Index has rallied 20% since June

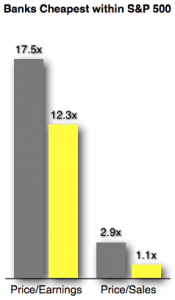

- Banks are still the cheapest group in the S&P 500 based on Price to Earnings and Price to Book

- Brokerage firms beginning to turn positive on banking sector for first time in several years

- Bloomberg Intelligence estimates 8% rise in net interest income if Fed Funds increase 100 bps

I love the geeky stuff Bloomberg’s analysts come up with, especially when it reveals something I hadn’t considered myself. Buried deep inside the new Bloomberg Intelligence application I stumbled upon a data-driven analysis of what happens to bank earnings as interest rates rise. BRILLIANT. That’s the whole thing right now. Admittedly, only money center banks and larger regionals provided the guidance necessary to drive the study, but suffice to say their sample suggests net interest income will increase 8% on average if the Fed raises interest rates 100 basis points. No wonder banks have popped 20% since June, investors finally have a reason to own them –especially with rock bottom valuations relative to the market. The question is, which ones should we buy?

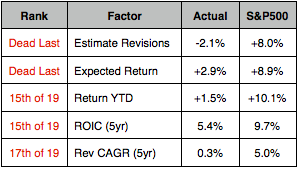

Banks have been dead money for so long. With home ownership still at a 40-year low of 63%, their largest engine of growth has been sputtering. Bloomberg divides the S&P 500 into 19 super-sectors and banks have ranked dead last this year both for earnings revisions and upside potential relative to current target prices. This is because there has been little reason to get excited over the past five years. Bank revenue growth and return on invested capital since 2011 have ranked 17 and 15 respectively. Not surprisingly stock returns too, have been down –though that has begun to change. Banks appear to have finally come home from their exile in Siberia.

Banks have been dead money for so long. With home ownership still at a 40-year low of 63%, their largest engine of growth has been sputtering. Bloomberg divides the S&P 500 into 19 super-sectors and banks have ranked dead last this year both for earnings revisions and upside potential relative to current target prices. This is because there has been little reason to get excited over the past five years. Bank revenue growth and return on invested capital since 2011 have ranked 17 and 15 respectively. Not surprisingly stock returns too, have been down –though that has begun to change. Banks appear to have finally come home from their exile in Siberia.

Pre-Approved?

Banks Anticipating Rate Hikes AND Outperforming

I admit, buying banks solely because the Fed will begin raising rates seems one-dimensional, and yet my inbox has been inundated with notes/questions/commentaries about the banks being cheap and how the macro environment has begun to shift. Here’s a sample from the past week alone:

Morgan Stanley

While the group has been a “bellyflop” to own for the first half of year, Financials may pose the best opportunity in the second half of 2016. The bull case is predicated on low ownership, a fundamental expectation of improving revenue comps and still aggressive focus on expenses. Also, banks and asset managers which missed revenue estimates during the quarter actually had positive returns one week later, outperforming stocks in other sectors that missed revenue expectations. That itself is a hallmark sign of bottoming. Morgan Stanly overweight names include JP Morgan (JPM) and Bank of America (BAC).

While the group has been a “bellyflop” to own for the first half of year, Financials may pose the best opportunity in the second half of 2016. The bull case is predicated on low ownership, a fundamental expectation of improving revenue comps and still aggressive focus on expenses. Also, banks and asset managers which missed revenue estimates during the quarter actually had positive returns one week later, outperforming stocks in other sectors that missed revenue expectations. That itself is a hallmark sign of bottoming. Morgan Stanly overweight names include JP Morgan (JPM) and Bank of America (BAC).

Strategas Research

The recent leadership from the Bank stocks is noteworthy, particularly given the persistent shape (flattening) of the curve. Bellwethers like JPMorgan (JPM) are acting well, and even the European Banks have bounced from small bases. Our hunch is the improved performance of the Banks and the relative weakness from Utilities may be foreshadowing at least a modest move higher in yields.

Bloomberg Intelligence

Loan growth has remained strong at regional banks, rising to 8% in 2Q… the past 12 months have been aided by residential mortgages, credit cards and other consumer lending. Median commercial and industrial loan growth has been stable sequentially at 7%.

The call from strategists is two-fold: Lending is improving so volumes are rising, and rates are going up so margins will expand. Coupled with the cheapest valuations of all 19 S&P 500 super sectors, you can understand why animal spirits are beginning to stir. Like E&P companies earlier in the year after oil started to re-inflate, investors smell opportunity and they have already begun to buy.

I see three ways to get exposure:

- Go total macro and buy the exchange traded fund for money center banks, the Financial Select Sector SPDR Fund (XLF)

- Focus more on the large regionals with lower exposure to capital markets via the SPDR S&P Regional Banking ETF (KRE)

- Drill down and find the highest quality banks within the S&P 1500 Index and create your own portfolio, recognizing premium assets are generally not be the cheapest.

The two ETFs are perfectly acceptable ways to express a macro view, and they will certainly provide exposure to some of the less expensive companies. If I’m bottom fishing, this is he way to go. As for the quality option, I’ll look past high multiples of earnings and book value, focusing instead on superior operating metrics.

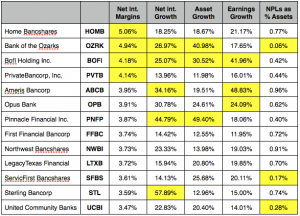

Here’s how I constructed my screen of the 97 banks in the S&P 1500 Index:

- Net Interest Margins are greater than 3.44% (the current average). Note JPM and BAC are below 2.3%. Ugh. Both banks are also in the XLF, which is why I’d rather sniff out my own handful of names.

- Net Interest Income and Total Assets are both rising at least 10%, implying a bank is adding healthy loans to its portfolio. (If assets were rising but NII weren’t, I’d be concerned.)

- Earnings are rising at least 10%

- Non-performing loans equate to less than 1% of total assets. The national average is 1.9%.

This criteria yields a total of 13 banks. While not cheap at an average price to book multiple of 1.9x and a forward earnings multiple of 14.4x, these are the superior names I want to own. They are up an average of 9.7% YTD, roughly in line with the S&P 500 Index. I’ve highlighted standout metrics in yellow.

Note: I’m happy to see Bank of the Ozarks made the cut. CEO George Gleason just closed his most recent acquisition and I wrote this up may in April before Bullseye’s official launch https://bullseyebrief.com/buy-the-buyers-issue-2-1/ Also of note, BofI Holdings appeared on my recent 10/10 Screen (10% growth under 10x earnings) and has since been moving up!

Quality Metrics = Quality Banks

Subscribe at https://bullseyebrief.com