Actionable Trades

BUY

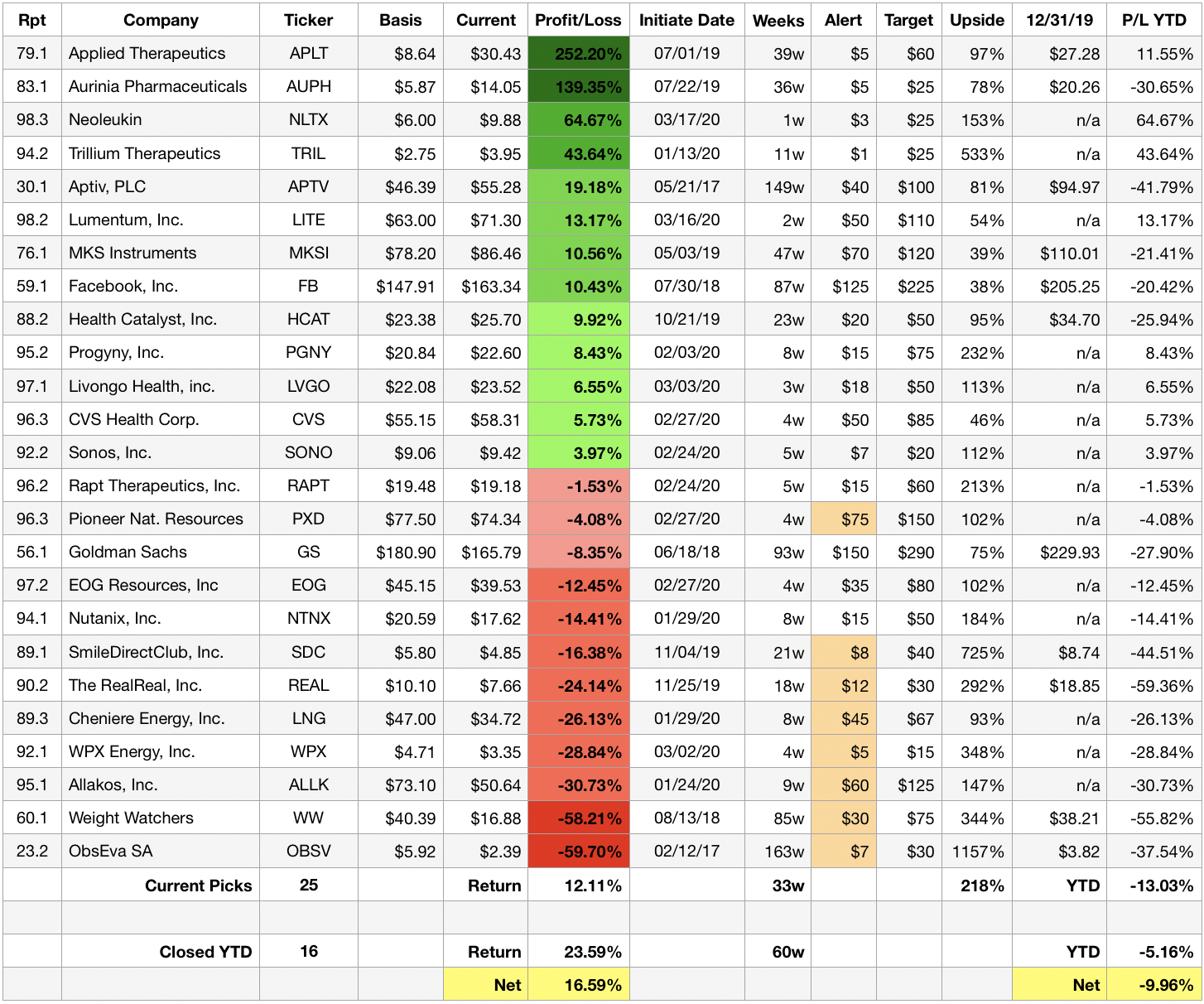

CVS Health, Inc. (CVS) – I am buying back this winning position from 2019 below $55.

Health Catalyst, Inc. (HCAT) – I am adding shares under $20.

Livongo Health, Inc. (LVGO) – I am building my position below $25.

Lumentum, Inc. (LITE) – I am buying back this winning position from 2019 below $65.

Neoleukin Therapeutics, Inc. (NLTX) – I am buying back this winning position from 2019 below $8.

Progeny, Inc. (PGNY) – I am building my position in the low $20s.

Rapt Therapeutics, Inc. (RAPT) – I am building my position in the mid-teens.

SmileDirectClub, Inc. (SDC) – Appears to have bottomed and I’m adding around $5.

HOLD

EOG Resources, Inc. (EOG) – I am underwater and adding below $35 in small increments.

Pioneer Natural Resources (PXD) -I am underwater and adding below $65 in small increments.

The RealReal, Inc. (REAL) – I am underwater and adding below $10 in small increments.

WPX Energy, Inc. (WPX) – I am underwater and adding at $4… the stock was $14 in January.

SELL

None, as I have already trimmed losers.

Bullseye Performance

Current Picks

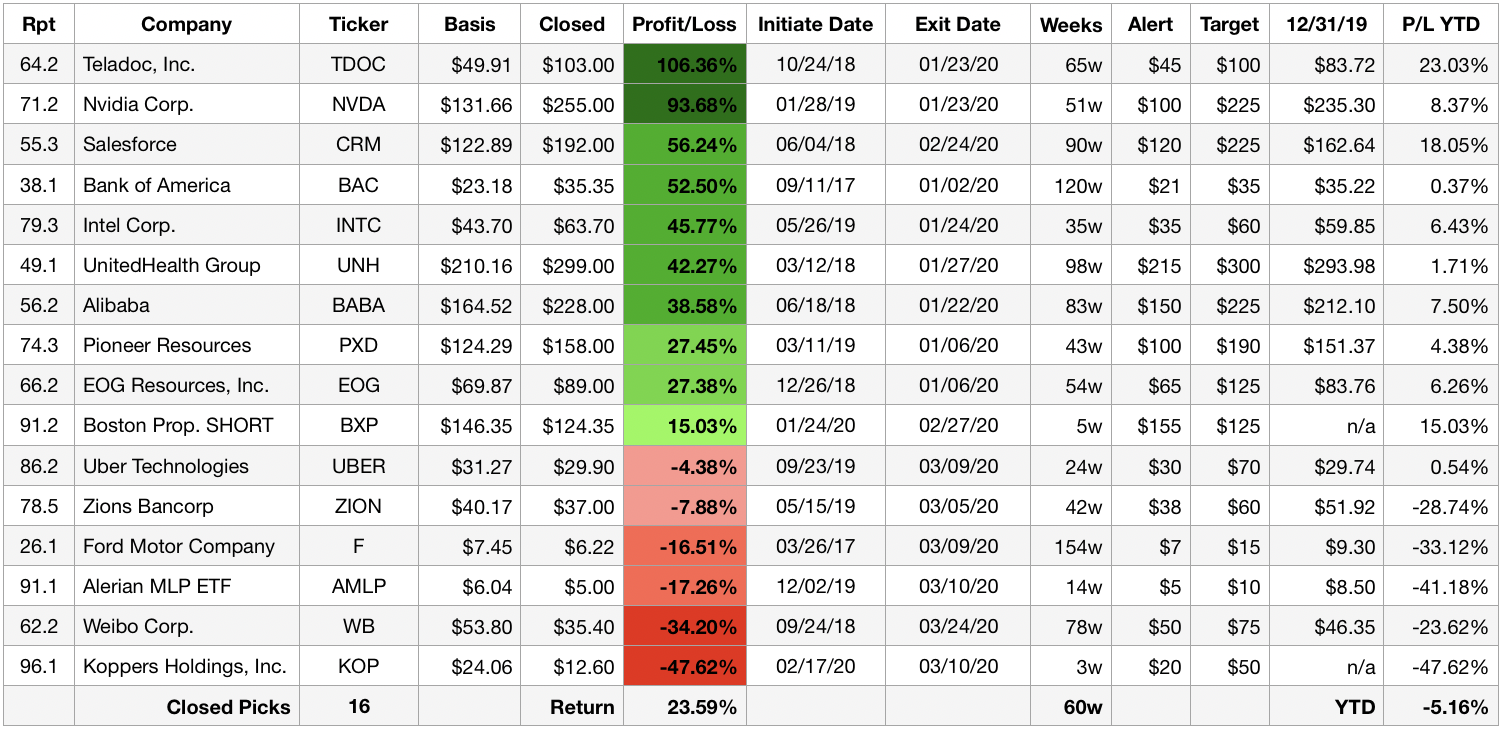

Closed Picks YTD