Buy the Buyers

Twelve Banks Devouring the Competition

- Select regional banks driving superior results through strategic M&A transactions

- Most active acquirers operating far from large, concentrated banking centers

- Serial acquirers delivering higher net interest margins and earnings growth

- Strong outperformance in spite of powerful head winds for the sector

George Gleason bought his first bank in 1979 at age 25, becoming both employee #13 and Chairman of a $28 million lender with five branches across rural Arkansas. Dozens of acquisitions later, his Bank of the Ozarks, Inc. (OZRK) is still buying and consistently ranks as one of the most profitable regional banks focused on traditional Main Street lending. Since 2010 alone, he’s added $6.6B in assets. His current bid for C1 Financial (BNK) will expand the franchise into southern Florida, adding an additional $1.5 billion in assets.

American Banker named Gleason Community Banker of the Year in 2010, citing consistent shareholder return and superior profitability. Operationally he focuses on three key drivers: net interest margin; asset quality; efficiency. Recently reported results for 4Q 2015 tell the story. Bank of the Ozarks’ NIMs of 526 bps rank well above the industry average of 337 bps, and annualized charge-offs total just 0.17%, meaning the bank writes down just 17 of 1,000 loans.

The stock has recently suffered from the market sell-off, as well as a lawsuit brought by shareholders of current target C1 Financial, who argue OZRK’s purchase price is too low. Even so, shares have trended higher with the announcement of each transaction. Since the beginning of 2011, shares have appreciated 246%, seven and a half times the Keefe, Bruyette & Woods Index of regional banks.

Growth & Gains

M&A Driving Outperformance

While a master of merger integration, Gleason’s roll-up strategy is hardly novel. BofA, Citigroup, JPMorgan and Wells Fargo can all trace the size of their current footprints to multiple acquisitions made since 1990. In the past three years alone, twelve regional banks have kept M&A advisors particularly busy, each buying an average of $265 million in assets every 9 months.

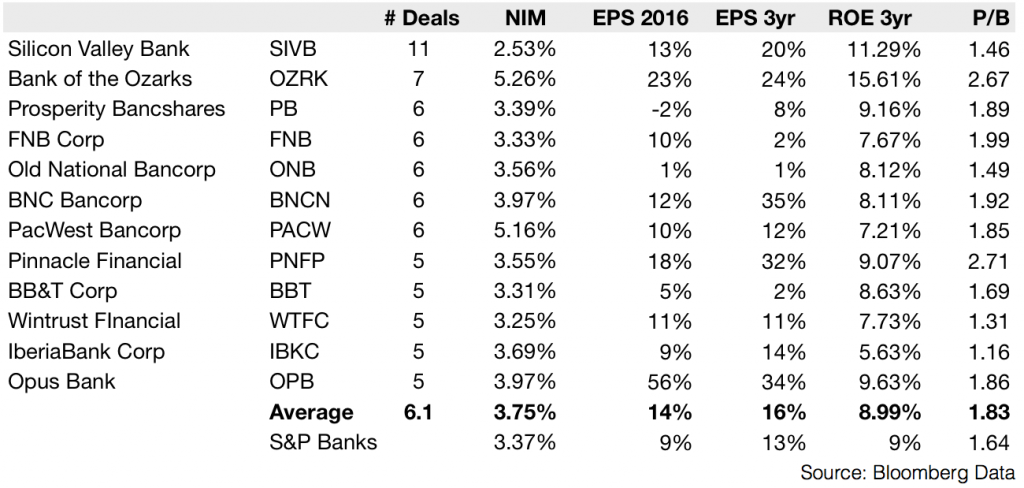

Busy Bankers

Top Consumer Bank Acquirers (2013-Present)

What’s particularly interesting about this group is its ability to post consistent growth and profitability while integrating multiple banks into their own established businesses.

• Net interest margins, the difference between a bank’s return on capital and its cost of capital, are significantly wider than the 94 banks of the S&P 1500 Bank Index (3.75% vs 3.37%).

• Earnings growth has exceeded the averages, both for the past 3 years and based on 2016 estimates (16% vs 13% and 14% vs 9% respectively). We also note this year’s estimates exceed the broader S&P 500 Index earnings forecasts by 2-3 times.

• Return on Equity figures are comparable to those of non-acquisitive banks, indicating transactions were generally accretive to earnings and therefore positive for shareholders of the buying banks. As Gleason commented at the C1 Bank acquisition announcement, “We strive to be an industry leader in providing best-in-class customer experience and operational efficiencies.”

Operational efficiencies are the operative words here. Streamlining procedures and integrating software gets very expensive, so does added regulatory compliance since 2008. Former American Banker Association President and two-term Oklahoma Governor Frank Keating told me Dodd-Frank costs the average Main Street bank 17 percent of operating profits. So the fact these twelve banks have been able to deliver superior earnings growth and maintain ROE while integrating multiple acquisitions speaks volumes. It also explains why they trade at a slight premium, in terms of price to tangible book value (1.83x vs 1.64x).

These regional banks have found a formula for earnings growth which eludes their larger money-center brethren. It’s a combination of strategic acquisition at the right price, organic expansion in niche markets, and rigorous attention to costs/efficiencies. Their proven ability to generate superior growth without sacrificing return on capital is all the more impressive considering two key facts:

1. Net interest margins for the industry as a whole sit near the lowest level since 1985, reflecting both a challenging environment near-term and a soft outlook into 2017

2. Bank stocks tend to lag NIMs by up to five years, as bond markets adjust faster to perceived future conditions than real world bankers can originate new loans (see below)

Powerful Headwinds

Profit Margins and Time Lags

Again, these banks have outperformed in spite of powerful headwinds. Their NIMs are rising and so are their stocks, which is why investors are paying a higher multiple of book value. As large money center banks continue parking excess reserves at the Federal Reserve to earn 25 bps, these strategic buyers are aggressively deploying capital to increase their footprints. They are building their businesses. They are the one slice of the banking sector to own now.