New Barons of Oil

How Icahn & Team Beat the Regulators

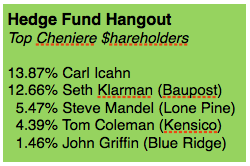

- Five hedge funds own 38% of the world’s largest LNG export operator

- The Sabine Pass, Louisiana terminal will be able to process 9% of global LNG demand by 2020

- Long-term supply contracts link prices of LNG at time of delivery to spot Brent prices

- LNG was upgraded recently by Standard & Poor’s and CFO Wortley seeks IG rating longer-term

Five powerful hedge funds have figured out how to bypass position limits in oil futures, and they’ll control billions of barrels for years to come. Led by Carl Icahn, several funds have amassed a 38% stake in publicly traded Cheniere Energy, Inc. (LNG). The company is building the country’s first-ever LNG export project, and it’s hands-down the single largest global project of its kind for the foreseeable future. On the surface it looks like gas, but dig deeper and it’s about oil –more oil than anyone could ever buy in the futures market, and for many more years than contracts exist. If you’re long-term bullish energy, this is the play.

What makes Cheniere so compelling is its combination of size, first-mover advantage and oil-indexed pricing of long-term sales to global customers. The Sabine Pass facility alone will be capable of processing 9% of the global demand for LNG by 2020. 85% of its capacity over the next 20 years has already been pre-sold at spreads to the Henry Hub U.S. natural gas price, and further indexed to Brent oil as the international energy benchmark. Additional capacity will price against oil spot prices for Brent, creating an implicit call option on the price of oil over the next 20+ years. This is the kicker, and it creates far more potential upside to the long-term price of oil than the oil futures market, which caps speculative positions at 20,0000 contracts, or about $900M worth oil at $45/bbl.

How It Came Together

For decades, Congress voted to treat U.S. domestic energy resources as strategic assets and prevented their export. That changed in 2011 when the Federal Energy Regulatory Commission concluded LNG export would ultimately prove a net benefit, based on increased drilling royalties, new tax revenue and job growth. The case was further strengthened by the unique position of the U.S. as global low cost producer. Cheniere’s petition to build the first-ever LPG export facility was granted and construction began.

The Sabine Pass, LA export terminal opened the first of 6 planned “trains” this summer. Each train is a self-contained facility spread over several acres which ingests natural gas via pipeline, super-cools it into liquid form, and then pipes it to holding tanks for export onto ships. Sabine Pass will be at full capacity by 2019, and 5 additional trains are currently planned for a second export terminal at Corpus Christie, TX.

The Sabine Pass, LA export terminal opened the first of 6 planned “trains” this summer. Each train is a self-contained facility spread over several acres which ingests natural gas via pipeline, super-cools it into liquid form, and then pipes it to holding tanks for export onto ships. Sabine Pass will be at full capacity by 2019, and 5 additional trains are currently planned for a second export terminal at Corpus Christie, TX.

Trains are financed by debt, collateralized by the physical assets, and debt repayment matches cash flow from long-term supply contacts with over a dozen global buyers. Cheniere calls them Foundation Customers, and without their commitment to buy LNG for the next 20 years at pre-determined spreads, Cheniere would not have been able to secure construction financing. Once the first seven trains are in place, which the CEO confirmed on the 3Q earnings call will be 2020, Cheniere will begin collecting $4.3B in annual fixed fees plus additional revenue on the incremental BOEs sold at spot rates.

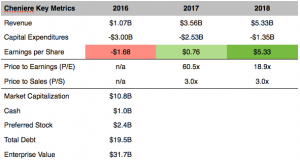

An important comment here about Cheniere’s $19B in debt. At nearly twice the equity market cap of $10.5B and 98% of assets, it’s a lot! Cheniere is significantly more levered than any of its peers, which Kynikos Associates Founder Jim Chanos has adamantly reiterated publicly in defense of his short position. However, what distinguishes Cheniere is its matching of current liabilities to forward contracts. This is what we call a back-to-back trade, cash flow arbitrage over time. It’s why Standard & Poor’s upgraded Cheniere in Q1 to BB- from B+ and CFO michael Wortley reiterated his ongoing conversation with both rating agencies during the 3Q call. He explicitly seeks an investment grade rating at LNG’s two operating subsidiaries and intends to simply/consolidate the corporate structure. These are positives.

Money Machine

Cheniere has exported 30 cargoes to date from the newly opened train 1, and trains 2-4 will likely come online next year. On the demand side, four new markets have openedto receiv e cargoes in the past 14 months (Jordan, Egypt, Pakistan and Poland). As a result, earnings accelerate from -$1.68 this year to a forecast of $0.76 next year and $2.43 in 2017 –which implies a forward P/E of 18.4x.

e cargoes in the past 14 months (Jordan, Egypt, Pakistan and Poland). As a result, earnings accelerate from -$1.68 this year to a forecast of $0.76 next year and $2.43 in 2017 –which implies a forward P/E of 18.4x.

The key here is visibility. Because Cheniere only begins the 4-year construction process to add incremental trains after securing 20-year forward supply contracts on 85% of capacity, the company is able to project multi-decade cash flow with much less expected variance than other energy related businesses. In addition, buyers include many state-owned enterprises like Electricite de France and Total, so default is not an issue.

While predictable cash flow is always appealing, the growth-minded hedge funds atop Cheinere’s list of shareholders are looking for far more than predictability, and they’ll get it. Cheniere sells 85% of capacity at a pricing formula which locks in a spread of 15% over the Henry Hub spot price for natural gas (plus additional charges for transportation, handling and storage) AND THEN INDEXES THE FINAL SALE PRICE TO SPOT MARKET PRICE OF BRENT OIL. It does so because Brent is the international energy benchmark, both for barrels of oil and gas-r elated barrels of oil equivalent (BOE). As Brent rises, Cheniere and its hedge fund shareholders make more money, especially on the 15% of capacity left unhedged and therefore able to rise with market prices.

elated barrels of oil equivalent (BOE). As Brent rises, Cheniere and its hedge fund shareholders make more money, especially on the 15% of capacity left unhedged and therefore able to rise with market prices.

Owning shares of Cheniere is like being long a call option on the future price of oil. The stock tracks closely with Brent, and cash flow from 20-year contracts provides sufficient cash flow to temper the downside. Additionally, long term investors recognize oil may be $45 now, but it won’t stay here indefinitely. The Baker Hughes Index of rigs actively drilling for new oil has fallen from 2,000 two years ago to 497 today. Stop drilling for new oil and your current supply runs out… prices rise. This is one of the reasons why forward Brent oil is well above today’s spot prices. The December 2019 contract costs $55.75 currently, 16% more than the current spot price.

Here’s the other key point: the ICE position limit for Brent is 20,000 contracts, which equate to less than $1B worth of oil at today’s prices –about one quarter the market value of the stock position held by the five hedge funds. True, so-called bona fide hedgers can get exemptions above position limits, but if you’re simply a large investor with a view, the futures market is too small. Icahn and his fellow investors in Cheniere have effectively gone around the position limits and created huge potential upside through Cheneiere’s exposure to oil-linked contracts. It’s the ultimate operating leverage play.

How WE Trade It

I believe Cheniere will develop into a core holding. It offers cash flow growth, earnings visibility, access to a global business with high barriers of entry and a 20-year call option on higher oil prices.

- Buy the stock now

- Sell covered call options to generate income, so we get “paid while we wait”

- Write out-of-the-money put options opportunistically (ie on declines) to capture additional premium and/or increase position size

For example, buy the stock at $45.00 to establish a position.

If I sell an October 50 call at $0.60 and an October 40 put at $0.70 I capture a total of $1.30 in premium for the next 42 days. This generates a 2.89% (25% annualized) if the stock stays between $40 and $50 through expiration and effectively lowers my cost basis on the original purchase to $43.70.

What if the sock trades through the strikes you ask? I will potentially own more shares under $40, or I will be called away at a profit above $50. I could also cover the options and simply hold the stock. Remember, selling options works in your favor over time, since every day they are worth less. Also, by creating a wide price bracket with out-of-the-money strikes, you’re building in a generous cushion. In this case, a 22% cushion over 42 days (50-40/45). ![]()